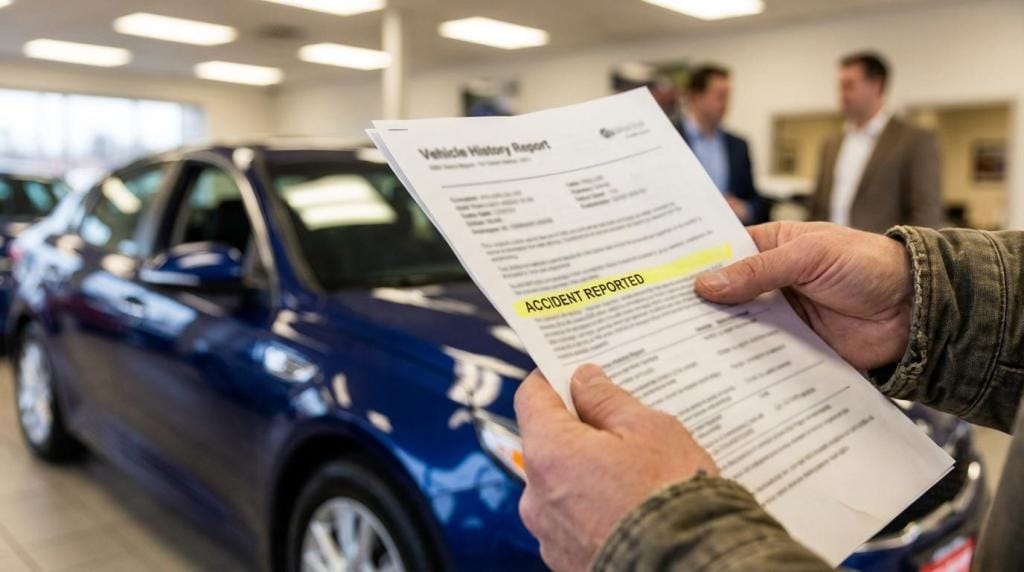

A car can look perfect after repairs and still be worth less the moment it shows an accident on its history report. Buyers worry about hidden structural issues, paintwork quality, and whether the next repair will be harder or more expensive. Dealers often price that risk in immediately.

A diminished value (DV) claim is the way you ask to be paid for that loss in resale value, separate from the repair bill. It can be one of the most overlooked parts of an auto claim, mostly because it sits in the gray space between “the car is fixed” and “the market still penalizes it.”

What “diminished value” really means

Diminished value is the gap between what your vehicle was worth right before the crash and what it’s worth after it has been repaired, with the accident now part of its record. Industry sources commonly define it as the reduction in resale value caused by the accident history, even when the vehicle is restored.

That difference can be small on an older, high-mileage car with cosmetic damage. It can be meaningful on a newer vehicle, a higher-end trim, or anything with structural repairs, airbag deployment, or multiple panels replaced.

A DV claim is not the same thing as “bad repairs.” If the repair is improper, that is usually handled through a supplemental repair dispute or a warranty issue with the shop. DV is about stigma and market behavior.

When DV is on the table: fault and claim type

Whether you can realistically collect diminished value often comes down to one question: whose insurance is paying?

In many states, DV is most commonly pursued as a third-party claim against the at-fault driver’s liability coverage. The logic is simple: liability aims to make the harmed party whole, and “whole” can include market value loss.

A first-party DV claim under your own collision coverage is harder. Standard policy language often caps payment at the lesser of repair cost or actual cash value (ACV), and insurers argue that once repairs are complete, the contract has been satisfied. Courts in some states have agreed with that reading in many contexts.

Michigan is a frequent outlier because of its no-fault framework, which often blocks or limits certain third-party property damage recoveries.

The three flavors of diminished value

Most conversations about DV are referring to “inherent” diminished value, but it helps to know the categories because insurers may try to steer the discussion toward the least favorable one.

- Inherent diminished value is the market penalty that remains even after high-quality repairs.

- Repair-related diminished value ties to substandard repairs or lingering defects.

- Immediate diminished value is the drop right after the crash, before repairs.

In practice, most consumers pursue inherent DV because it is the most widely recognized concept for a repaired vehicle with an accident history.

What affects the dollar amount

There is no universal DV calculator that every insurer must follow nationwide. The value impact usually depends on vehicle specifics and what the local used-car market does with accident history.

Here are the factors that typically move DV the most:

- Severity and location of damage (structural and safety-related repairs often matter more)

- Make, model, trim, year, and mileage

- Prior accident history (a second accident can compound the stigma)

- Pre-loss condition and maintenance records

- Quality and documentation of repairs

- Local demand for the vehicle and how comparable listings are priced

Some insurers reference formula approaches in certain settings (you may hear about “17c” in Georgia-related discussions), while independent appraisers often rely more heavily on market comps, dealership offers, and documented valuation methods.

A quick table: common DV scenarios and what to expect

The fastest way to set expectations is to match your situation to the most common claim routes.

| Scenario | Who pays | DV usually available? | Notes to watch |

|---|---|---|---|

| Other driver clearly at fault, you file against their liability | At-fault insurer | Often yes | Stronger when you can show market comps and an appraisal |

| You are at fault, you file under your collision | Your insurer | Often no | Policy language may limit payment to repair/ACV only |

| Other driver uninsured, you use UMPD (where available) | Your insurer | Depends on state and policy | Some states treat UMPD more like a third-party recovery substitute |

| Vehicle is totaled | Insurer paying ACV | DV usually not separate | DV is typically baked into the ACV settlement discussion |

This is a general guide, not a guarantee. State law, policy language, and claim posture can change the outcome.

Build your DV file before you argue the number

A DV claim is a documentation contest. Adjusters tend to take these claims more seriously when your packet is organized and your number is tied to evidence, not a guess.

After you have a paragraph of context in your demand, the rest should read like a file index. Keep it clean and easy to verify.

Gather the basics first:

- Crash report and claim numbers

- Repair estimates, final invoices, and supplements

- Photos before repairs, during repairs (if available), and after delivery

- Proof of pre-loss condition (maintenance, recent inspection, tire/brake receipts)

- Valuation support (pre-loss and post-repair)

- Vehicle history report (to show the accident is now recorded)

Many people add an independent diminished value appraisal. It costs money up front, yet it can anchor negotiations because it gives the adjuster something concrete to rebut.

A practical filing sequence that avoids common timing issues

You generally want to wait until repairs are complete, because the claim is about the value of the repaired vehicle with an accident history, not a partially repaired car. Also, your repair bill and final damage description are part of what supports the value impact.

A simple workflow looks like this:

- Confirm fault and coverage path (third-party liability, UMPD, or other).

- Complete repairs and collect final invoices, parts lists, and paint materials detail if available.

- Document the post-repair condition with clear photos in good lighting.

- Establish pre-loss value using recognized guides and real market listings for similar vehicles.

- Obtain an independent DV appraisal if the likely DV is more than the appraisal cost.

- Prepare a DV demand letter with your evidence packet attached.

- Negotiate the settlement amount and get the agreement in writing before accepting payment.

If the insurer asks for “proof someone offered you less,” that can be difficult to produce without actually trying to sell the car. Market comps and an appraisal report usually stand in for that.

What to say when the adjuster pushes back

Many DV disputes follow a predictable script: the insurer says the car was repaired properly, so there is no loss. Your response should be calm, evidence-based, and tied to market reality.

Here are approaches that tend to be more productive than repeating the same demand number.

- Position it as market math: pre-loss value minus post-repair value, supported by comps and the damage profile.

- Focus on what buyers do: accident history changes resale behavior even when repairs are excellent.

- Keep the scope narrow: you are not reopening the repair bill, you are addressing resale value.

When it is time to negotiate, it helps to separate “whether DV exists” from “how much DV is fair.” The first is a concept discussion. The second is a pricing discussion.

Useful negotiation moves include:

- Ask for their valuation method: request the insurer’s written basis and any formula inputs they used.

- Challenge unsupported reductions: if they discount for “minor damage” but your invoice shows significant parts replacement, call out the mismatch.

- Offer a clean counter: respond with a single number and a short explanation tied to your appraisal and comps.

- Escalate within the claim unit: request supervisor review when the adjuster will not explain the valuation.

- Use formal options when available: appraisal clauses, small claims court limits, or state complaint channels vary by location.

Keep every email and letter. A timeline matters if you later need to show delays or inconsistent explanations.

State law wrinkles that can change the outcome

Two consumers with identical vehicles and identical repairs can get different results based solely on where the crash occurred and what coverage applies.

A few patterns show up repeatedly:

- Third-party DV claims are commonly recognized in many jurisdictions because they follow general tort principles of making the claimant whole.

- First-party DV under collision is frequently denied based on policy limits of liability language, unless a state requires it or a specific endorsement applies.

- Michigan’s no-fault structure often limits the typical third-party DV path many people assume exists everywhere.

- Some states have clearer statutory language around value-before and value-after property damage measures, while many rely on case law and claim practice.

If you are unsure, start by confirming whether you are pursuing DV as a liability claim against the at-fault carrier or trying to add it onto your own collision payment. That one distinction often predicts the rest of the process.

Mistakes that shrink DV payouts

Most underpaid DV claims are not underpaid because the concept is wrong. They are underpaid because the file is thin, the timing is off, or the claimant accepts a quick denial without asking for the insurer’s basis.

One sentence can save you weeks: “Please provide your written valuation method and supporting data for your DV position.”

Other common missteps include overreaching with an inflated number, skipping the appraisal when the vehicle is high value, or mixing repair disputes into the DV demand. Keep the claim clean: repaired car, documented accident, measurable market penalty.

If you plan to trade the vehicle soon, consider starting your DV documentation early, while the repair details and damage photos are easy to obtain. That paper trail is hard to recreate later.