Are you using your car for work and wondering if your insurance will cost more? It’s a common question with an important answer.

When you drive your car for business purposes—not just commuting—your insurance company may see you as a higher risk. This could mean your premiums go up, but it depends on how you use your vehicle and what kind of coverage you have.

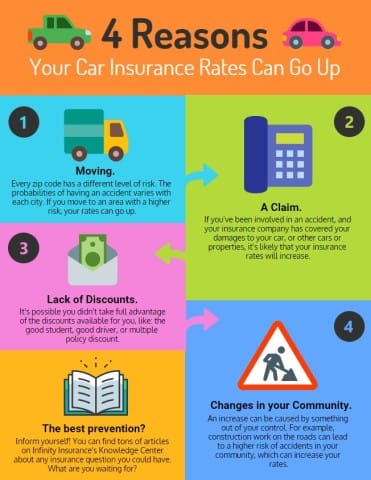

You’ll learn exactly when your car insurance might increase, how to avoid surprises, and what options you have to protect yourself without breaking the bank. Keep reading to make sure you’re fully covered and not paying more than you need to.

Work Use Vs Personal Use

Understanding the difference between work use and personal use of your car is key. Insurance companies treat these types of use differently. Your insurance costs may change depending on how you use your vehicle. Knowing the distinction helps you avoid surprises on your bill.

Work use usually means driving related to your job beyond just going to work. Personal use involves everyday activities like shopping or visiting friends. Each use carries different risks, which insurers consider when setting your premium.

Defining Business Use

Business use means driving your car for tasks tied to your job or business. This includes delivering goods, visiting clients, or making work-related trips. Your personal insurance may not cover these activities fully. Some insurers require a business use endorsement or a commercial policy for this type of driving.

Business use increases the chances of accidents because of more time spent on the road. Insurers see this as higher risk, which can lead to higher premiums. Always be clear with your insurer about how you use your vehicle to get proper coverage.

Commuting Vs Work-related Driving

Commuting means driving between your home and workplace. Most personal car insurance policies cover this by default. It is considered personal use even though it is work-related.

Work-related driving goes beyond commuting. It involves trips during work hours for business reasons. This could be visiting clients, running work errands, or transporting equipment. This type of use often requires additional insurance coverage.

Insurance companies may charge more if your driving includes work-related trips. The risk of accidents is higher with more miles and different driving conditions. Knowing the difference helps you choose the right insurance and avoid coverage gaps.

Credit: www.infinityauto.com

Insurance Policy Types

Choosing the right insurance policy depends on how you use your car for work. Different types cover different risks. Understanding these types helps protect you and your vehicle adequately. It also affects your insurance cost and coverage limits.

Personal Auto Insurance

Personal auto insurance covers everyday driving like commuting and errands. It usually excludes work-related use beyond normal commuting. If you use your car mainly for personal reasons, this policy works well. Using your car for business might not be fully covered under this policy. Accidents during business use could lead to denied claims or higher costs.

Commercial Auto Insurance

Commercial auto insurance is designed for vehicles used primarily for work tasks. It covers driving related to your job or business activities. This policy offers higher coverage limits and protection for business risks. It suits drivers who travel a lot for work or carry equipment. Commercial insurance usually costs more but provides better protection for work use.

Adding Business Use Endorsements

Business use endorsements add coverage to your personal auto policy. They cover some work-related driving not included in a standard personal policy. This option can be cheaper than a full commercial policy. It fits those who use their car for limited business trips. Adding endorsements helps avoid coverage gaps and potential claim denials.

Factors Influencing Premiums

Several factors influence car insurance premiums when using a vehicle for work. Insurers assess risks differently based on usage and driver profile. Understanding these factors helps predict possible premium changes. Below are key elements that affect insurance costs.

Mileage And Driving Frequency

Insurance companies consider how much you drive daily. Higher mileage means more chances of accidents. Frequent driving, especially in busy traffic, raises risk levels. Long work commutes usually increase premiums. Short, occasional trips tend to keep costs lower.

Job Title And Occupation Risks

Your job type impacts insurance rates too. Certain occupations involve higher risks on the road. Delivery drivers, salespeople, or field workers face more exposure. Jobs with frequent stops or heavy traffic use raise premiums. Safer, office-based roles might not change rates much.

Vehicle Type And Usage Patterns

The kind of vehicle you drive affects insurance costs. Commercial vehicles or trucks often cost more to insure. Using your car for transporting goods or tools adds risk. Personal cars used lightly for work may stay on personal policies. Insurers also check how you use your vehicle daily.

Impact Of Work Use On Rates

Using your car for work can affect your insurance rates. Insurers view work use differently than personal use. This change often impacts your premium costs. Understanding how work use influences rates helps you prepare for possible increases.

Insurance companies assess the type and amount of driving. Work-related trips usually mean more time on the road. More driving raises the chance of accidents. This higher risk leads to higher insurance premiums.

How Premiums May Increase

Work use can increase your car insurance premiums. Driving longer distances for work raises accident risks. Insurers charge more to cover this added risk. Using a vehicle for deliveries or client visits often costs more. Even small increases in daily mileage can affect your rates. Insurance companies want to cover possible claims from work trips.

Risk Assessment By Insurers

Insurers analyze how often and why you drive. Work use means more exposure to traffic and hazards. They consider the type of work you do with your car. Jobs involving heavy traffic or risky areas raise your risk profile. Insurers also check if you carry equipment or passengers. These factors influence how much your insurance will cost.

When To Switch To Commercial Insurance

Using your car for work can change your insurance needs. Personal car insurance often does not cover many business-related uses. Commercial insurance offers protection designed for work-related driving. Knowing when to switch helps avoid coverage gaps and higher costs later.

Criteria For Commercial Coverage

Commercial insurance is needed if your car use fits certain conditions. Regularly driving to multiple job sites counts. Carrying tools, equipment, or products for work applies too. If you transport clients or passengers for pay, personal insurance won’t cover you. Also, if your car use exceeds typical commuting, consider commercial coverage. Insurance companies check how you use your vehicle closely.

Common Business Activities Requiring It

Many jobs require commercial car insurance. Delivery drivers must have it. Tradespeople carrying tools and materials need coverage. Real estate agents driving clients fall under this too. Rideshare and taxi drivers must carry commercial insurance. Any job that uses your car for business errands or appointments usually needs this policy. This insurance protects your vehicle and your business risks.

Credit: www.candsins.com

Tips To Manage Insurance Costs

Managing car insurance costs can be tricky, especially when using your vehicle for work. Understanding ways to control expenses helps keep your premiums affordable. Simple steps can make a big difference.

Communicating With Your Insurer

Always inform your insurer if you use your car for work. Full disclosure ensures you get the right coverage. It prevents surprises if you need to file a claim. Ask questions about how work use affects your premium. Clear communication builds trust and helps find cost-saving options.

Choosing The Right Coverage

Select coverage that fits your work needs. Avoid paying for unnecessary add-ons. Consider liability limits and comprehensive protection. Some insurers offer business-use endorsements on personal policies. Compare quotes for both personal and commercial insurance. Right coverage protects you without overspending.

Maintaining A Clean Driving Record

Safe driving lowers your insurance costs. Avoid tickets and accidents at all costs. Insurers reward drivers with good records. Use defensive driving techniques daily. Regularly review your driving habits and improve them. A clean record keeps premiums steady or even reduces them.

Common Misconceptions

Many drivers worry about using their car for work and the impact on insurance. Myths and misunderstandings often cause confusion. Knowing facts helps you avoid unnecessary stress and expenses. Here are some common misconceptions about work use and insurance rates.

Using Car For Work Always Raises Rates

Not all work-related driving leads to higher insurance rates. Insurers check how often and how far you drive. Occasional work trips usually do not affect premiums. Frequent, long-distance driving may increase your risk. This could lead to higher costs. But simple errands or short commutes for work rarely change your rate.

Commuting Automatically Requires Commercial Insurance

Many think commuting means commercial insurance is mandatory. This is not true. Commuting to a regular workplace is considered personal use by most insurers. Commercial insurance is needed if you use your car for business tasks. Examples include deliveries or client visits during work hours. Just driving to and from the office does not require a commercial policy.

Credit: www.thehadilawfirm.com

Frequently Asked Questions

Does Car Insurance Cost More If You Use It For Work?

Car insurance often costs more if you use your vehicle for work. Increased mileage and higher risk raise premiums. Commercial insurance may be required for business use, offering better coverage than personal policies. Always inform your insurer about work-related use to ensure proper protection and accurate rates.

Do I Need Different Insurance If I Use My Car For Work?

You need different insurance if you use your car for work tasks beyond commuting. Commercial auto insurance covers business-related driving. Personal policies often exclude work use, risking insufficient coverage and higher premiums. Always inform your insurer about work-related car use to ensure proper protection.

Do I Need Different Car Insurance To Drive For Work?

You may need different insurance if you use your car for work tasks beyond commuting. Business use often requires commercial coverage. Personal policies usually don’t cover work-related driving risks fully. Always inform your insurer to ensure proper protection and avoid claim denials.

Is It Cheaper To Insure A Vehicle For Work Or Pleasure?

Insuring a vehicle for work usually costs more than for pleasure due to higher risk and mileage. Work use may require commercial insurance.

Conclusion

Using your car for work often means more miles and higher risk. This can lead to increased insurance rates. Insurance companies may require you to switch to a commercial policy. Not telling your insurer about work use can cause denied claims.

Always be honest and update your policy to fit your needs. Staying informed helps you avoid surprises and extra costs. Driving safely and keeping good records also keeps your premiums lower. Understanding how work use affects insurance keeps you protected and stress-free.