If your home has suffered damage, you might be wondering: will homeowners insurance cover the cost of bringing your house up to current building codes? This question matters because older homes often don’t meet today’s safety and construction standards, and repairs can get expensive.

You want to protect your investment without unexpected bills, but insurance policies can be confusing when it comes to upgrades required by code. You’ll discover what homeowners insurance typically covers, where it falls short, and how you can prepare financially if code upgrades become necessary.

Keep reading to make sure you’re not caught off guard when it’s time to rebuild or repair your home.

Credit: mrelectric.com

Homeowners Insurance Basics

Homeowners insurance protects your home and personal belongings from damage or loss. It also provides liability coverage if someone is injured on your property. Understanding what your policy covers helps you prepare for unexpected events. Insurance policies vary, so knowing the basics is important before making decisions.

Insurance covers sudden events but not all types of damage. Some risks require extra coverage or separate policies. It is essential to read your policy carefully and ask questions if anything is unclear.

What Homeowners Insurance Covers

Homeowners insurance usually covers damage caused by fire, lightning, windstorms, and hail. It also protects against theft and vandalism. The policy covers your home structure and personal property inside. Liability protection helps with medical bills and legal fees if someone is hurt on your land. Some policies include additional living expenses if you cannot live in your home due to damage.

Coverage limits vary by policy and insurer. Check your policy to see what perils are included and the maximum payout amounts. Some policies automatically include coverage for certain risks, while others need endorsements for full protection.

Common Exclusions

Standard homeowners insurance usually excludes damage from floods and earthquakes. These disasters need separate policies or endorsements. Damage caused by normal wear and tear or neglect is not covered. Pest infestations, mold growth, and sewer backups also fall outside standard coverage unless you add special endorsements.

High-value items like jewelry or art may have limited coverage. You may need a rider or scheduled personal property insurance for full protection. Business activities conducted at home are often not covered under a homeowner’s policy. Always verify exclusions to avoid surprises during a claim.

Code Upgrade Costs

Bringing a house up to current building codes often means extra costs for homeowners. These costs, called code upgrade costs, cover changes needed to meet new safety and construction standards. Insurance policies may not always cover these expenses, making it important to understand what triggers these costs and why they can be high.

When Code Upgrades Are Required

Code upgrades become necessary during major repairs or rebuilding after damage. If a home suffers fire, storm, or other covered damage, local laws may require updates to electrical, plumbing, or structural systems. These updates ensure the house meets modern safety rules. Insurance may pay for damage repairs but not always for upgrades required by new codes.

Why Upgrades Can Be Expensive

Upgrades often involve replacing old materials or systems with newer, safer ones. For example, old wiring may need to be replaced with modern, safer electrical wiring. Plumbing might need new pipes that meet current health standards. These changes add labor and material costs. Also, permits and inspections required by local authorities increase expenses. These factors make code upgrade costs much higher than simple repairs.

Insurance And Code Compliance

Homeowners insurance protects your house from many risks. It covers damage from fire, theft, and storms. But what about bringing your house up to current building codes? Insurance and code compliance can be complex topics. Understanding how insurance handles code upgrades helps homeowners prepare better.

Building codes change over time. Older homes may not meet new safety or construction rules. After damage, repairs might require upgrades to comply with these codes. Insurance policies vary in how they handle these costs. Knowing the details can save money and stress.

Standard Policy Limits On Code Upgrades

Most standard homeowners insurance policies do not cover full costs to meet new building codes. They usually pay to restore your home to its previous state, not to upgrade it. This means you may pay out of pocket for code-related improvements.

Insurance often sets limits on what it will pay for code upgrades. These limits can be a small percentage of the total claim. If your home requires major changes to meet current laws, costs above the limit are your responsibility.

Role Of Ordinance Or Law Coverage

Ordinance or law coverage is an optional add-on to standard policies. It helps cover extra costs for code compliance after damage. This coverage pays for upgrades needed to meet current building codes during repairs.

This coverage can include expenses like removing outdated materials, rebuilding to new standards, and meeting safety rules. Without it, homeowners must pay these costs themselves. Ordinance or law coverage offers important financial protection for code-related repairs.

Additional Coverage Options

Standard homeowners insurance often falls short when it comes to covering the costs of bringing a house up to current building codes. Many policies have limits or exclusions for upgrades required after damage. Homeowners should explore additional coverage options to protect their investment and avoid unexpected expenses. These options help cover the extra costs needed to meet local building standards during repairs.

Endorsements For Code Upgrades

Endorsements are add-ons to your existing policy that increase coverage. They can cover the cost of bringing your home up to code after damage. For example, a building code upgrade endorsement helps pay for electrical, plumbing, or structural improvements required by law. This coverage usually has limits, so check your policy details carefully. Adding such endorsements gives extra protection against costly code-related repairs.

Separate Policies Needed

Sometimes endorsements are not enough to cover all code upgrade costs. Separate policies may be necessary for specific situations, such as flood or earthquake damage. These policies often include their own rules about code upgrades. Without the right separate policy, you might pay out of pocket for upgrades required by local codes. Discuss your needs with your insurance agent to ensure you have proper coverage.

Claims Process Tips

Filing a claim to bring your house up to code can be complex. Understanding the claims process helps you avoid delays and denials. Proper preparation and clear communication improve your chances of success.

How To Document Code-related Repairs

Start by taking clear photos of the damage and areas needing repair. Keep all receipts from contractors and materials used. Get written estimates from licensed professionals about the work required. Maintain a detailed list of all repairs and upgrades made to meet code. Submit this documentation with your insurance claim to support your case.

What To Avoid Saying To Insurers

Do not admit fault or say you neglected maintenance. Avoid guessing or providing uncertain information about the damage. Stay away from agreeing that the damage is your responsibility. Never say the repairs are optional or cosmetic. Keep your statements factual and focused on the repairs needed to meet code requirements.

Credit: uphelp.org

Real-life Scenarios

Understanding how homeowners insurance handles the costs of bringing a house up to code can be confusing. Real-life examples help clarify what situations might lead to insurance coverage or require homeowners to pay themselves. These scenarios show the fine line between insurance help and out-of-pocket expenses.

When Insurance Paid For Upgrades

In some cases, insurance covers the cost to update parts of a home to meet current building codes. This often happens after a covered event like a fire or storm. For example, if a fire damages the electrical system, insurance might pay to replace old wiring with new, code-compliant materials.

Another example involves plumbing repairs after water damage. If the pipes need full replacement, the insurer may cover upgrades to meet modern safety standards. These payments depend on the policy’s specific language and endorsements about code upgrades.

When Homeowners Paid Out Of Pocket

Many homeowners face costs to bring their homes up to code that insurance does not cover. This typically occurs during routine repairs or upgrades not linked to a covered loss. For instance, if a homeowner wants to update their outdated electrical panel voluntarily, the insurance company will not pay for it.

Also, if damage happens slowly over time, like gradual water seepage or wear and tear, insurance usually denies code upgrade claims. Homeowners must cover these expenses themselves. Knowing when insurance stops and personal responsibility starts saves money and stress.

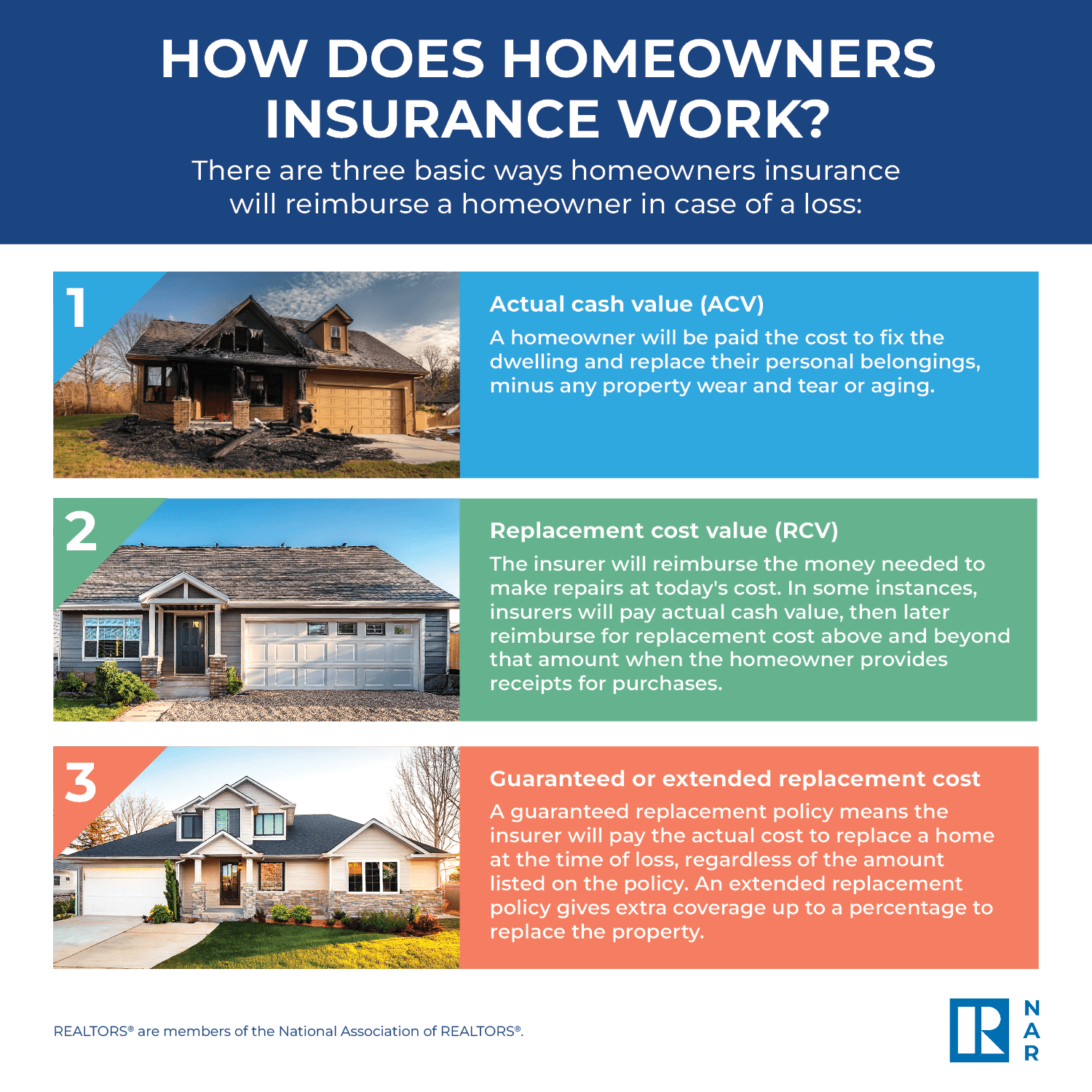

Credit: www.nar.realtor

Frequently Asked Questions

What Two Events Are Not Covered Under Homeowners Insurance?

Homeowners insurance does not cover flood damage or earthquake damage. These events require separate policies or endorsements for protection.

What Will Homeowners Insurance Pay For?

Homeowners insurance pays for damage to your home, personal belongings, liability claims, medical expenses, and additional living costs. Coverage depends on covered perils and policy limits.

What Not To Say To Homeowners Insurance?

Avoid admitting neglect, intentional damage, or false information. Don’t exaggerate claims or hide facts. Stay honest and clear for smooth processing.

What Is Code Coverage In Homeowners Insurance?

Code coverage in homeowners insurance protects against damages caused by covered risks, like fire or theft. It excludes floods, earthquakes, and wear. Coverage limits and policy terms determine payouts for repairs or replacements.

Conclusion

Homeowners insurance usually does not cover costs to bring a house up to current codes. This work often counts as an upgrade, not a repair. Some policies offer limited coverage through endorsements or riders. Separate policies may be needed for specific risks.

Homeowners should review their policy details carefully. Knowing what is covered helps avoid surprises after damage or loss. Always ask your insurance agent about code upgrade coverage options. Planning ahead protects your home and your wallet.