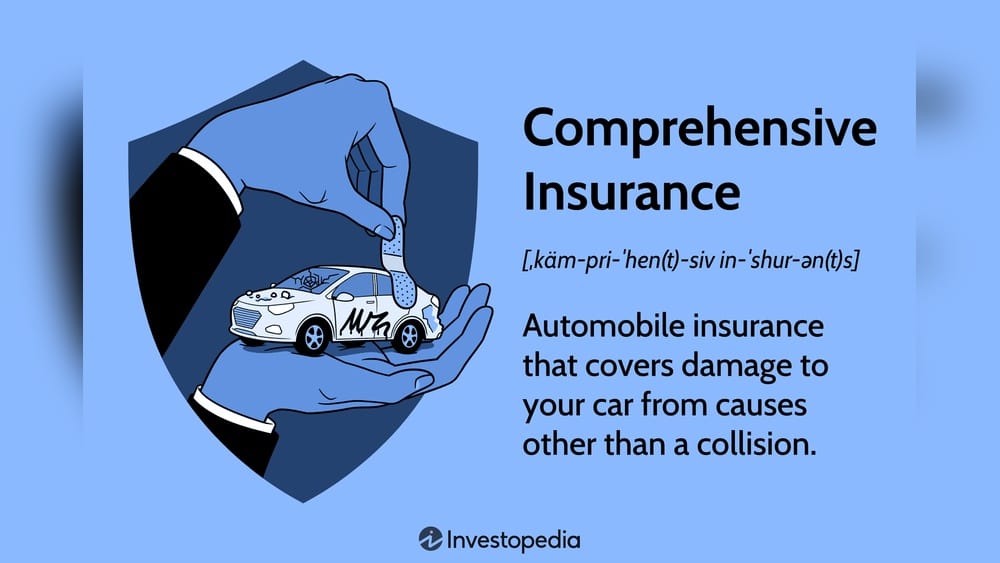

When it comes to protecting your car, understanding what comprehensive car insurance really covers can save you from unexpected costs and stress. You might already know that accidents happen, but what about those surprises like theft, vandalism, or severe weather damage?

Comprehensive car insurance is designed to cover these kinds of risks—things beyond just collisions. If you want peace of mind knowing your vehicle is protected from more than just crashes, this guide will help you see why comprehensive coverage could be exactly what you need.

Keep reading to discover what it covers, how it differs from collision insurance, and how to decide the right protection for your car and budget.

Comprehensive Coverage Basics

Comprehensive car insurance provides broad protection beyond accidents. It covers many types of damage to your vehicle that do not involve collisions. This coverage helps you repair or replace your car after unexpected events. Understanding the basics of comprehensive coverage helps you make informed choices. Here is a look at the key elements of this coverage.

Non-collision Protection

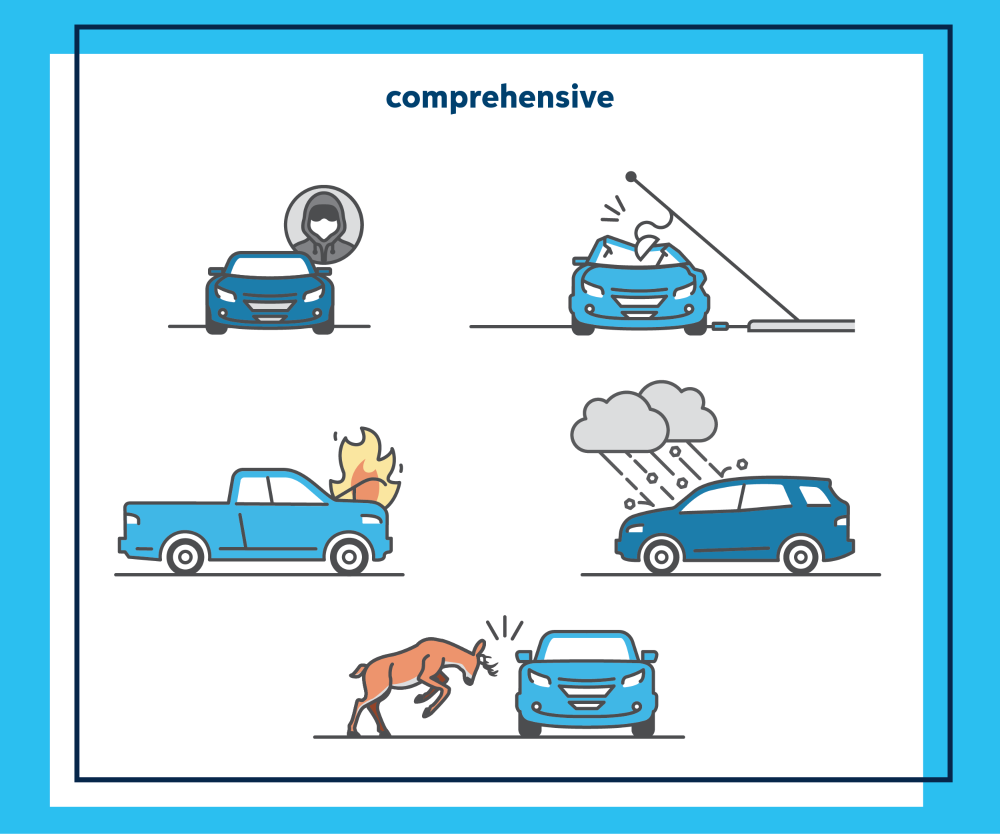

Comprehensive coverage protects your car from damage that is not caused by crashes. This includes theft, vandalism, and natural disasters. It also covers damage from hitting animals and falling objects. This protection reduces your financial risk from many common hazards on the road.

Common Covered Events

The events covered under comprehensive insurance include theft and vandalism. Weather-related damage such as hail, floods, and storms is also included. Fire, explosions, and damage caused by animals are covered as well. Even broken windows or windshields fall under this coverage. These events can cause costly repairs, and comprehensive insurance helps cover those costs.

Deductibles And Payouts

A deductible is the amount you pay before insurance pays the rest. Choosing a higher deductible lowers your premium but increases out-of-pocket costs. The payout is usually the car’s actual cash value before damage. This value accounts for depreciation and is less than the replacement cost. Understanding deductibles and payouts helps you manage your coverage effectively.

Credit: www.auto-owners.com

Damage Types Covered

Comprehensive car insurance protects your vehicle from many types of damage beyond crashes. It covers incidents that happen without a collision. Understanding what damage types are covered helps you see the value of this insurance. Below are common damage types included in comprehensive coverage.

Theft And Vandalism

Theft coverage pays if your car is stolen. It also covers damage caused during theft attempts. Vandalism includes intentional damage like scratched paint or broken windows. This protection helps you avoid high repair or replacement costs.

Weather-related Damage

Damage from weather events is covered under comprehensive insurance. Hail, floods, hurricanes, and tornadoes can harm your car’s body and engine. Lightning strikes and earthquakes may also cause damage. This coverage helps with repairs or replacement after these natural events.

Animal Collisions

Hitting an animal can cause serious damage to your car. Comprehensive insurance covers collisions with deer, dogs, or other wildlife. It pays for repairs to your vehicle’s body and mechanical parts damaged in such accidents.

Falling Objects And Fire

Falling tree branches, rocks, or debris can damage your car’s roof or windshield. Fire damage, including explosions, also falls under comprehensive coverage. This helps protect your car from unexpected events beyond your control.

Glass Repairs

Cracked or shattered glass, such as windshields and windows, is covered. Many insurers pay for glass repairs without applying your deductible. This coverage keeps your car safe and legal to drive without extra cost.

Key Features

Comprehensive car insurance offers broad protection beyond just accidents. It covers damage caused by events outside your control. Understanding its key features helps you decide if this coverage fits your needs.

This type of insurance pays for repairs or replacement after theft, fire, or natural disasters. It also covers damage from animals or vandalism. Knowing how it works can save you money and stress later.

Optional But Recommended

Comprehensive insurance is not required by law. Many drivers skip it to save money. Yet, lenders often require it for financed or leased cars. This coverage protects your vehicle from many risks that collision insurance does not.

Choosing comprehensive coverage means fewer out-of-pocket expenses after unexpected damage. It provides peace of mind for events like hailstorms or theft. Even if optional, it is worth considering.

Actual Cash Value Explained

Insurance companies usually pay the actual cash value (ACV) of your car. ACV means the car’s market value right before the damage happened. It does not cover the full cost of a new car.

The ACV amount reflects your car’s age, condition, and mileage. The insurer subtracts your deductible from this value. Understanding ACV helps set realistic expectations for any claims.

Deductible Impact

The deductible is the amount you pay before insurance covers the rest. Choosing a higher deductible lowers your premium but increases your out-of-pocket cost. A lower deductible raises your premium but reduces upfront costs after a claim.

Balancing deductible and premium depends on your budget and risk tolerance. Knowing this impact helps you pick the best plan for your situation.

Comprehensive Vs Collision

Understanding the difference between comprehensive and collision car insurance is essential. Both cover damages but apply to different situations. Choosing the right coverage protects your vehicle and wallet effectively.

Coverage Differences

Comprehensive insurance covers damage not caused by a crash. It includes theft, vandalism, fire, natural disasters, and hitting animals. Collision insurance covers damage from accidents with other vehicles or objects. For example, hitting a tree or another car falls under collision coverage.

When Each Matters

Comprehensive insurance matters if you face risks like theft or weather damage. It pays for repairs or replacement after non-collision incidents. Collision insurance matters after accidents on the road. It helps fix your car if you crash into something or someone.

Combining Both

Many drivers choose both types for full protection. Combining comprehensive and collision covers most damage scenarios. This combination is often required for financed or leased vehicles. It ensures peace of mind and financial security after damage.

Choosing Comprehensive Coverage

Choosing comprehensive coverage means protecting your car from many risks beyond collisions. It covers damages caused by theft, weather, animals, and falling objects. This type of insurance helps you avoid large repair costs. Consider your environment to decide if comprehensive coverage fits your needs.

High Theft Or Vandalism Areas

Living in an area with high theft or vandalism increases the risk to your car. Comprehensive coverage pays for damages from theft or intentional harm. It covers stolen vehicles and repairs for broken windows or scratched paint. This protection gives peace of mind in risky neighborhoods.

Severe Weather Zones

Severe weather can cause heavy damage to vehicles. Hail, floods, and storms can leave costly marks or even total loss. Comprehensive coverage helps cover repairs from these natural events. It also protects against fire damage caused by lightning or heat. This coverage is wise in weather-prone areas.

Animal And Falling Object Risks

Collisions with animals can cause serious car damage. Deer, raccoons, or stray dogs can cause accidents or dents. Falling objects like tree limbs or rocks also pose risks. Comprehensive coverage pays for these types of damage. It ensures your car is covered from many unexpected dangers.

Choosing Collision Coverage

Choosing collision coverage is an important step in securing your car insurance comprehensive policy. This coverage pays for damages if your car hits another vehicle or object. It helps you avoid high repair bills after an accident. Understanding key factors can guide you to the right choice for your situation.

Urban Traffic Risks

City driving brings many challenges. Traffic is dense and accidents happen more often. Parking lots are crowded, increasing chances of bumps and scrapes. Collision coverage protects against these frequent urban damages. It offers peace of mind in busy areas.

Financial Considerations

Collision coverage comes with a cost that varies by insurer. Deductibles affect how much you pay after a claim. Lower deductibles mean higher premiums but less out-of-pocket expense later. Consider your budget and accident risk before deciding on coverage levels.

Vehicle Value Importance

The value of your car matters greatly in choosing collision coverage. Older cars with low value may not need expensive coverage. New or high-value cars benefit more from collision insurance. It covers repair costs that could otherwise be very high.

When To Have Both

Sometimes, having just one type of car insurance coverage is not enough. Combining comprehensive and collision insurance can offer fuller protection. Knowing when to have both helps you avoid big costs after accidents or other damages. This section explains key situations where carrying both coverages benefits you the most.

Financed Or Leased Vehicles

Cars that are financed or leased usually require both collision and comprehensive insurance. Lenders want to protect their investment. If your car gets damaged or stolen, the insurance covers repairs or replacement. Without both coverages, you might face expensive out-of-pocket bills. This ensures your car’s value is safeguarded until you fully own it.

Maximum Protection Needs

Drivers who want the highest level of protection should consider both coverages. Comprehensive insurance covers events like theft, fire, or natural disasters. Collision insurance pays for damages from crashes. Using both means you get coverage for nearly all types of car damage. This combination is ideal for new or valuable cars and those in risky areas.

Credit: www.progressive.com

When To Drop Coverage

Deciding when to drop comprehensive car insurance coverage can save money without leaving you unprotected. Comprehensive insurance covers damage beyond collisions. It includes theft, vandalism, natural disasters, and animal strikes. Knowing the right time to stop this coverage depends on your vehicle and costs.

Low-value Vehicles

For older cars with low market value, comprehensive coverage may cost more than the car is worth. Repair bills after an incident might be higher than the car’s value. In such cases, dropping comprehensive coverage can make financial sense. You avoid paying premiums that are unlikely to pay off. Check your car’s current value before deciding.

Cost Vs Benefit Analysis

Weigh your premium costs against potential claims and deductible amounts. If your yearly premium plus deductible exceeds the car’s value after damage, coverage might not be worth it. Consider how often you face risks covered by comprehensive insurance. Areas with low theft or natural disasters risk might justify dropping coverage. Calculate potential savings and risks carefully before making a choice.

Full Coverage And Risk Management

Full coverage and risk management in car insurance comprehensive plans protect your vehicle from many types of damage. This coverage goes beyond accidents and covers risks like theft, fire, and natural disasters. Managing risk means understanding what protection you need without paying too much for insurance.

Choosing the right amount of coverage helps avoid large unexpected expenses. It also gives peace of mind while driving. Knowing how to balance coverage and costs is key to smart risk management.

Balancing Coverage And Costs

Finding the right insurance means weighing protection against price. Full coverage may cost more but reduces financial risks. Cheaper plans might leave you with big bills after damage. Consider your car’s value and where you live. Areas with high theft or weather risks need stronger coverage. Adjust your deductible to control premium costs. A higher deductible lowers monthly payments but increases out-of-pocket expenses after a claim.

Consulting Insurance Professionals

Insurance agents can explain coverage options clearly. They help match your needs with affordable plans. Experts understand risks in your location and vehicle type. They suggest coverage that fits your budget and risk level. Ask questions to understand terms like deductibles and exclusions. Professional advice reduces surprises during claims. Use their knowledge to create a balanced insurance plan that protects without overspending.

Credit: www.infinityauto.com

Frequently Asked Questions

What Does Comprehensive Mean On Car Insurance?

Comprehensive car insurance covers non-collision damage like theft, vandalism, fire, natural disasters, and animal impacts. It protects against risks outside of accidents. You pay a deductible, and the insurer covers repair or car value minus that deductible. It’s optional but often required by lenders.

Is It Better To Have Collision Or Comprehensive?

Choose collision to cover accident damage and comprehensive for non-collision risks like theft or weather. Both protect differently. Prioritize based on your car’s value and location. Financed cars usually need both; older cars might skip one to save costs.

What Is Included In Comprehensive Car Insurance?

Comprehensive car insurance covers theft, vandalism, fire, natural disasters, animal damage, falling objects, and glass breakage. It excludes collision accidents. It pays for repair or actual cash value minus deductible. Lenders often require it for financed or leased vehicles.

What Does Comprehensive Insurance Cover You For?

Comprehensive insurance covers non-collision damages like theft, vandalism, fire, natural disasters, animal hits, and falling objects. It also protects against windshield and glass damage. This coverage pays for repairs or actual cash value minus your deductible, offering broad protection beyond accident-related incidents.

Conclusion

Comprehensive car insurance offers broad protection beyond accidents. It covers theft, weather damage, vandalism, and animal collisions. This coverage helps reduce unexpected repair costs. Choosing comprehensive depends on your location and risks. Consider your vehicle’s value and daily driving conditions.

Combining comprehensive with collision insurance adds extra security. Protect your car wisely for peace of mind on the road.