Average home insurance costs in the U.S. Are roughly $1,900 a year for a $300,000 dwelling, though rates vary by state, city, and wildfire or flood risk.

In California and the West, higher rebuild costs and wildfire zones drive premiums past the national average.

Credit tier, roof age, coverage limits and deductibles shift the price.

To get down to real figures for your region, the next portions detail state ranges, risk elements, and tips to slice rates.

What Are Average Home Insurance Costs?

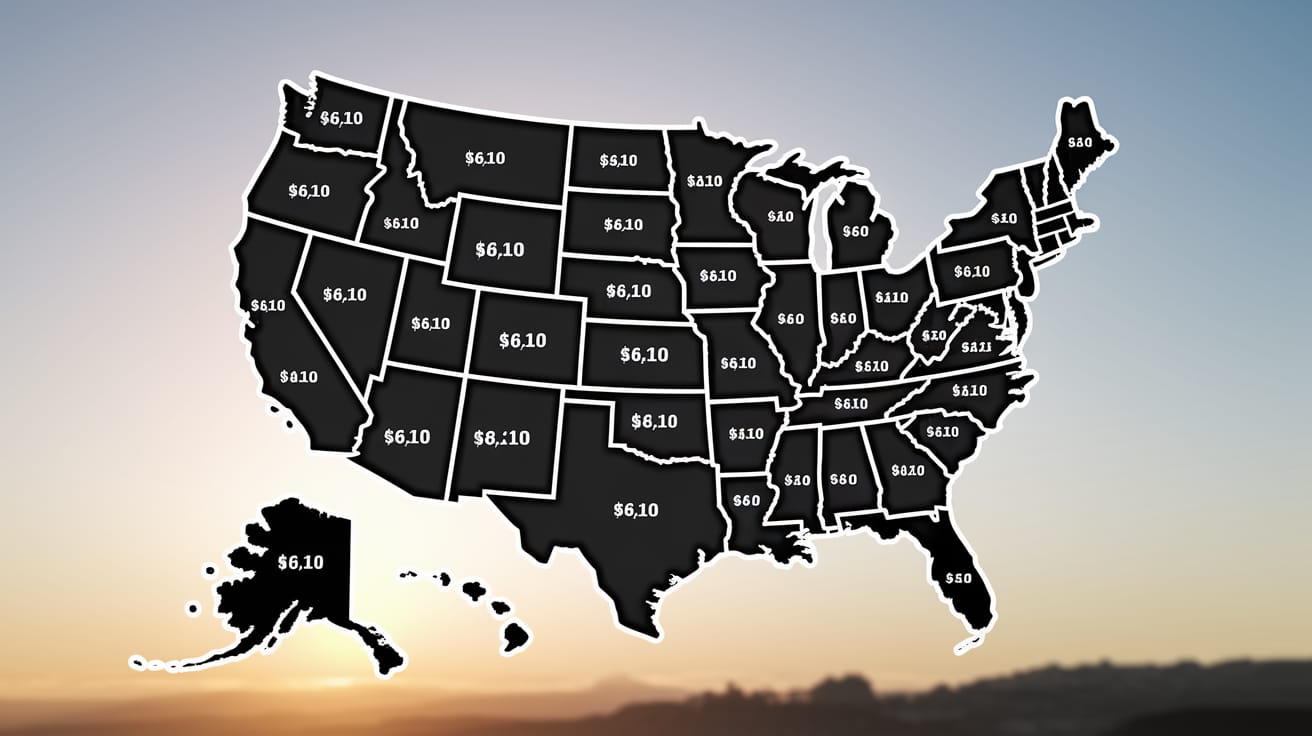

The average homeowners insurance cost is about $2,110 annually nationwide, translating to approximately $176 per month. However, certain reports indicate that the average homeowners insurance rates could be as high as $2,802. These homeowners insurance premiums vary significantly by state and dwelling coverage amount, with annual rates ranging from roughly $610 in Hawaii to nearly $6,210 in Oklahoma, reflecting local risks and market dynamics.

1. National Averages

The average U.S. Homeowners premium is $2,110 per year. That number mixes various home types, coverage amounts, and deductibles, so it’s a median, not a standard. Most owners spend $1,000 to $3,000 annually, with extreme cases on both ends.

They have gone up over the last 10 years. Inflation, more costly materials, labor shortages, and increased catastrophe losses are all driving premiums up. An average monthly cost falls somewhere around $233 to $250, combined with a $1,000 deductible, but actual bills depend on your home’s rebuild cost, location, and risk profile.

2. State-by-State Breakdown

Many of the most expensive states happen to be in severe weather corridors. Oklahoma, Texas, and Nebraska have three of the steepest averages. Nebraska is around $4,505 annually, and even particular towns such as Oklahoma City ($8,544) and New Orleans ($8,276) are on the higher end due to tornado, hail, wind, or hurricane risk.

Less expensive states are Hawaii, Vermont, and Delaware. Hawaii’s statewide average is low, around $610 per year, in part because of fewer wind and hail claims for typical HO-3 forms, and Delaware comes in around $1,025.

Regional risks—hail, tornadoes, hurricanes, wildfire—along with local construction costs, claim frequency and legal environments produce huge disparities between states. Here’s a basic table that compares annual and monthly averages to help you set your expectations.

State | Annual Avg | Monthly Avg |

|---|---|---|

Hawaii | $610 | $51 |

Delaware | $1,025 | $85 |

Vermont | $1,100 | $92 |

National Avg | $2,110 | $176 |

Nebraska | $4,505 | $375 |

Texas | $4,900 | $408 |

Oklahoma | $6,210 | $518 |

3. Monthly Premiums

I find it useful to convert annual costs to monthly for budget purposes. Hawaii’s $610 average per year works out to approximately $51 per month. Oklahoma’s $6,210 reduces to roughly $518.

Anticipate increased monthly bills in metro areas with extreme risk or aging homes. Location, home value, deductible, and coverage choices drive the outcome. Plug in the monthly amount when graphing your total housing expense. It clarifies escrow requirements and cash flow, particularly when rates reset after a claim or reappraisal.

4. Coverage Level Impact

Higher dwelling limits raise premiums since the insurer is liable for a bigger rebuild. Broader coverage, such as extended replacement cost, ordinance or law, or low sublimits, adds more.

Minimum limits tend to miss real rebuild costs, particularly with older homes that do not have modern safety features and are expensive to fix. Credit matters too; bad credit can increase premiums as much as 72 percent versus good credit.

Deductibles help control price. Moving from one thousand dollars to two thousand five hundred dollars can save about 12 percent on average, though you will pay more out of pocket when you file. Balance risk, cash reserves, and lender regulations to establish limits that align with your budget without underinsuring.

Why Your Neighbor Pays Differently

Average homeowners insurance costs can vary significantly, even among houses on the same street. Homeowners insurance rates depend on various risk factors, the design of the policy, and the quoting insurance company. No two homeowners insurance policies have the same price, as insurance carriers consider dozens of elements, including house specifications and claims history.

Your Home’s Profile

Home age, size, and construction significantly drive the homeowners insurance cost. For instance, a 2,400-stucco home with a hip roof will have a different rate compared to a 2,400 wood-frame house with a gable roof due to varying repair costs and wind resistance. Generally, brick structures tend to rate better for fire protection. Additionally, older features like knob-and-tube wiring or polybutylene pipes can lead to increased homeowners insurance premiums.

Newer homes typically enjoy lower home insurance premiums because updated electrical, roofing, and plumbing systems reduce the likelihood of loss and the variance in repair costs. Distinctive attributes, such as a pool, can elevate liability limits, while features like a board or slide may increase them even more.

A wood stove, trampoline, or koi pond changes risk and can cause endorsements or exclusions to be activated. Two identical homes can still get very different quotes from different carriers since each carrier’s rating model is unique, and included coverage—like extended dwelling replacement, ordinance or law, or water backup—changes the price.

It is crucial to detail your home’s unique features and upgrades to accurately estimate their impact on your homeowners insurance rates and to compare coverage terms effectively. Opting for a higher deductible can significantly lower your premium, potentially saving hundreds or even thousands per year. Bundling discounts with auto or umbrella policies can further enhance savings, often ranging from 5 to 25 percent depending on the insurer and state regulations.

Your Location’s Risk

Where you live significantly influences the homeowners insurance cost you can expect. Areas prone to hail, hurricanes, wildfires, or theft typically experience higher base rates, often accompanied by specific wind or wildfire deductibles. For instance, a coastal ZIP code near the Gulf or Atlantic, or in a tornado-prone Midwest corridor, generally commands higher average homeowners insurance rates compared to an inland suburb with a mild climate and low crime rates.

Factors like ZIP code, proximity to a staffed fire station, and local building codes play a crucial role in determining the homeowners insurance premiums. Stricter building codes and impact-rated roofs can lead to lower insurance costs. Additionally, creating a wildfire defensible space in certain western states can earn homeowners valuable credits on their policies.

To understand local risk factors, it’s essential to check severe weather history, crime statistics, ISO fire protection class, and any special deductibles required by insurance carriers in your area. As a result, two policies from different carriers may evaluate the same house differently based on these local signals, affecting the overall home insurance cost.

Your Personal History

Claims history is a powerful indicator. Multiple claims, particularly water or fire, are likely to increase rates. Coverage lapses can cause rates to spike on renewal or switch.

A good insurance score or good credit usually translates into lower prices. Non-smoking homes, monitored alarms, and water leak sensors can score discounts. Being a recent buyer, over 55, or bundling home and auto can move pricing even more.

Having a clean claims record, keeping detectors and alarms active, and shopping similar coverage limits and deductibles help keep your average premium low. Keep in mind that even ‘twin’ neighbors never have the same history, coverage, or discounts, so quotes will vary.

The Hidden Drivers of Rate Hikes

They’re driving average homeowners insurance costs up today and influencing tomorrow’s homeowners insurance rates. Even with no claims, many owners still face higher premiums as market forces cascade through insurance prices. Follow these indicators to predict your bill shifting.

Hidden driver | What it is | Why it raises premiums | What to watch |

|---|---|---|---|

Construction inflation | Material and labor spikes | Higher replacement costs and coverage limits | Local contractor bids, lumber, roofing, wage data |

Climate risk | More frequent, severe events | Larger losses and risk concentrations | NOAA storm data, wildfire maps, flood updates |

Reinsurance costs | Insurance for insurers | Pricier capital passed to policyholders | Global catastrophe losses, market renewals |

Legal environment | Litigation and settlements | Higher loss adjustment expenses | State lawsuit trends, assignment-of-benefits rules |

Underwriting shifts | New models and appetites | Wider premium spread for same home | Quotes across carriers, policy nonrenewals |

Household finances | Incomes vs. expense growth | Affordability strain, policy downgrades | Rate filings vs. median income trends |

Construction Costs

Escalating construction material and labor expenses directly push up home insurance pricing. When asphalt shingles, copper wiring, and drywall climb, the price to rebuild a 2,000-square-foot home climbs with them.

Tight contractor supply after big storms or regional booms lifts bids. Replacement costs that are higher necessitate insurers to increase average coverage levels and rates. If your Coverage A is old, you’re in danger of a shortfall.

Insurers need to update their own internal cost indices and pass through higher limits and premiums. Local construction cost spikes can drive above-average prices in areas experiencing labor bottlenecks, such as swiftly growing metros or post-wildfire regions.

Coastal wind codes and seismic retrofits add additional per square foot cost. Update dwelling limits to present-day rebuilding costs. Request your agent for a replacement cost review, bring a recent contractor estimate, and consider extended or guaranteed replacement endorsements.

Climate Change

Hurricanes, hailstorms and wildfires struck more often and with greater severity, driving up costs. Losses accumulate across entire neighborhoods, not just individual residences.

Insurers increase rates in high risk regions, particularly along coastal counties and the wildland-urban interface. There are some carriers that cut coverage or leave ZIP codes, so climate change impacts price and availability.

Follow local weather and hazard trends—hail swaths in the Plains, heat-driven wildfire seasons in the West, and stronger tropical systems along the Gulf and Atlantic—to see where rates might migrate next. Since 2019, rates are up some 40.4% nationally, climbing almost twice as fast as homeowner incomes.

That gap pressures budgets and can escalate owners to higher deductibles.

Reinsurance Rates

Reinsurance is insurance to insurance companies, protecting them from big, correlated losses. When global catastrophes hit, think of a rough hurricane season combined with European windstorms.

Reinsurers pass on price increases at renewal. Pushed by surging reinsurance prices, insurers must raise homeowners premiums even in lower-risk inland regions as capital costs are pooled across portfolios.

Legal costs matter too: property-related lawsuits and claim disputes add loss-adjustment expense in some states, further pressuring filings. Keep track of market news mid-year and January renewals. Shifts there tend to appear in your renewal six to nine months down the road.

Still shop widely: carriers use different underwriting formulas, so quotes for the same home can vary. Even with a spotless claims history, it might still qualify for a more favorable rate band, but capitalism sets the bottom.

Yearly non-mortgage home expenses approaching $15,979 furthermore emphasize the way repair inflation supplies future replacement values and premiums.

How to Lower Your Premium

Intelligent modifications can reduce the average homeowners insurance cost without compromising coverage. Key moves include raising deductibles, stacking discounts, improving your home’s risk profile, bundling policies, and conducting an annual review to spot waste.

- Raise your deductible. This swaps low-claim expenses for lower rates.

- Ask for discounts: multi-policy, claim-free, loyalty, senior, smart home.

- Upgrade safety: security systems, storm protections, wiring, plumbing, roof.

- Keep a clean claim record and solid credit score.

- Bundle home and auto for up to 30% savings, insurer dependent.

- Shop rates yearly; some households save $1,000 or more.

- Tell your insurer about improvements and new devices.

- Trim extras you don’t need, but keep key protections.

Increase Deductibles

Increasing the deductible typically reduces the homeowners insurance cost, as you’re taking on more of a loss. For instance, going from $1,000 to $2,500 can save you almost 12% a year; however, these savings depend on factors such as your state, insurer, and your home’s risk profile. This strategy is most effective if you can absorb the higher out-of-pocket costs on short notice.

Higher deductibles mean that if you file a claim, you will pay more out of pocket. It’s wise to avoid setting the deductible above your emergency fund. Additionally, storm or wind deductibles may be separate in some states and could be based on a percentage of your dwelling coverage amount, so be sure to check the fine print.

Choose a deductible that aligns with your cash cushion and risk tolerance. To understand the impact on your homeowners insurance premiums, compare quotes at $1,000, $2,500, and $5,000 to identify the breakpoints. Inquire how these changes affect dedicated deductibles for hail, hurricane, or wildfire claims.

Seek Discounts

- Multi‑policy (home + auto), security systems, smart‑home devices

- Claim‑free for several years, loyalty, senior, mature homebuyer

- Impact‑resistant roof, protective devices, water leak sensors

- Paperless billing, pay‑in‑full, automatic payments, new‑home credits

Home and auto bundling can save you up to 30% off, which varies by carrier. Verify that both policies are still competitive after bundling.

Inquire about claim-free discounts, as some activate after a few years. Record all possible upgrades, such as alarms, leak detectors, and roof work. Submit receipts and photos to guarantee credits.

Improve Your Home

Install storm shutters, reinforced roofing, or impact-rated materials in hail or coastal zones to reduce peril and premiums. In wildfire zones, create defensible space and install ember-resistant vents. Upgrading electrical panels and old plumbing reduces water and fire losses.

A centrally monitored security system, smart smoke detectors, and water shutoff valves can reduce rates at certain insurers. Clear gutters, repair minor leaks quickly, and trim roof trees. The fewer claims you have, the better chance you have of maintaining discounts and keeping rates stable.

Review Annually

Lower Your Premium – Check your policy annually to make sure coverage matches your needs and local risks. Update dwelling limits after remodeling or major purchases and ditch coverage you don’t need anymore.

Shop at least three quotes. Many owners save over $1,000 per year. Maintain credit; being in bad shape can cost more than 71%, so reporting mistakes is worth combating. Inform your insurer of new enhancements and inquire whether savings are in effect now or at renewal.

Understanding Your Policy’s Value

Average home insurance costs keep climbing, so the goal is simple: pay for protection you actually need, nothing you don’t. The national average is approximately $2,802 annually, but premiums differ significantly based on state, municipality, home age, credit tier and deductibles.

Understand every coverage’s value, how limits operate, and what you’re really purchasing with your premium.

Dwelling Coverage

Dwelling coverage pays to rebuild the structure of your home if a covered peril, such as fire, wind, or theft, causes damage. The limit should represent the full replacement cost, not market price, land value, or mortgage balance.

Underinsuring the dwelling shifts the gap on you. If a $500,000 rebuild follows a total loss and you’re only carrying $350,000 in coverage, you’re under by $150,000. This does not include potential code-upgrade costs.

In high-risk zones like Oklahoma City or New Orleans, where premiums are through the roof, replacement cost accuracy is even more significant. Run a home insurance calculator, then check square footage, materials, local labor, roof type, and code requirements.

Check up after significant renovations and at every renewal if building expenses in your ZIP code skyrocket.

Personal Property

Personal property coverage protects your stuff: furniture, clothes, appliances, and most electronics. Policies typically default to 50% to 70% of dwelling coverage, which might not be sufficient.

High-value items, such as jewelry, watches, art, and collectibles, frequently require a scheduled endorsement to protect their full value and risks such as mysterious disappearance. Without it, sublimits kick in and your payout can underwhelm.

Create a home inventory that includes photos, serial numbers, purchase dates, and prices. Save it to the cloud. Update it with big purchases or moves.

Liability Protection

Liability pays the legal and medical fees if someone is injured on your property or you injure someone else. Higher limits increase premiums but protect your savings, income, and home equity.

Weigh your risk: dogs with bite history, a pool, frequent guests, short-term rentals, or teenage drivers in the household. Most families opt for $300,000 to $500,000. Wealthier owners frequently prefer $1 million.

For additional peace of mind, an umbrella policy that provides coverage ranging from one million to five million dollars above your home and auto liability at a fairly modest cost.

Additional Living Expenses

ALE covers temporary housing if a covered loss makes your home unlivable. This includes hotel stays, short-term rentals, meals beyond normal, and laundry and parking as they are getting it fixed.

Limits differ and influence premium. Some impose a dollar limit, whereas others impose an elapsed time limit, such as 12 or 24 months. Even at older homes, where repairs are frequently more expensive, longer repair periods can exceed low ALE limits.

Read the fine print: covered perils only, sublimits for pets or storage, documentation rules, and any exclusions that shift costs back to you. Save receipts. Review limits if local rents spike.

Beyond the Standard Policy

Standard homeowners insurance provides coverage against fire, theft, and certain wind and hail damages, yet it leaves gaps in protection. Floods, earthquakes, and normal degradation are typically excluded. Optional coverages and endorsements can help close those gaps; however, they often lead to higher homeowners insurance costs, which vary based on local risks and your home’s construction.

Flood Insurance

Your regular home insurance doesn’t cover flooding. Water that comes from outside, such as storm surge, heavy rain, and river flooding, is flood, not homeowners.

You need a stand-alone flood policy. You can purchase via the NFIP or private providers. They both provide building and contents coverage. Nonetheless, private plans may allow for higher limits or additional benefits such as temporary living expense.

Rates differ by FEMA flood zone, elevation, foundation type and limit. A house in a high-risk zone close to a coast will pay a lot more than one on higher ground. Even beyond the mapped high-risk areas, localized street flooding can still damage basements, HVAC and flooring.

Flood-Excess Homeowners in flood-prone areas should price NFIP and private quotes side by side. If you have a mortgage in a SFHA, the lender will almost certainly need it.

Earthquake Coverage

That’s as most standard homeowners policies don’t cover quakes and shakes. Cracked foundations, fallen chimneys, or broken pipes from shaking are not found in a typical policy.

You can purchase earthquake coverage as either a separate policy or an endorsement, depending on your state. In California, many buy via the California Earthquake Authority. In other states, private options differ. Deductibles are typically high, around 10% to 25% of the dwelling limit, so claims anticipate a higher out-of-pocket portion.

Price varies based on seismic risk, soil type, home age, construction (wood-frame vs. Masonry), and deductible selection. If you live by a known fault or in soft-soil zones, evaluate your risk and retrofit status (bolting, cripple-wall bracing) and then compare premium to possible loss.

Other Endorsements

- Water backup of sewers or drains

- Extended or guaranteed replacement cost for the dwelling

- Ordinance or law coverage for code upgrades after a loss

- Scheduled personal property for jewelry, art, or collectibles

- Equipment breakdown for major systems

- Such as wildfire defense or loss prevention services in a high-risk area

- Home business property and liability

- Short-term rental or landlord coverage for rental units

- Matching siding/roof endorsement for uniform repairs

Endorsements allow you to customize a policy to actual hazards. They add premium, but they cover gaps. Maintenance issues are not covered, but water backup is. Standard theft limits for jewelry are low, but scheduling increases them.

Major renovations or an addition could go over base limits without an update. If you operate a small home business or short-term rental, standard policies may restrict or exclude those risks.

Contrast options with your insurer, map them to local threats such as hurricanes, wildfires, earthquakes, or inland floods, and adjust limits after upgrades.

Conclusion

Average home insurance rates vary a ton across the US and even across town. Risk, rebuild cost and claim trends drive the lion’s share of it. Big storms, fire zones and rising labor and lumber costs contribute to those increases. Smart tweaks can soften the blow. Increase a deductible with caution. Pair it with auto. Request wind and water enhancements. Shop quotes once a year. Maintain good credit. Reduce small claims.

Plain protection still counts above a dirt-cheap price. Look for limits on rebuild, liability, and loss of use. Then add stuff that corresponds to actual risks in your ZIP.

Need a quick reality check? Pull two to three quotes, compare rebuild limits line by line, then call your top pick to lock gaps. Need answers? Leave them, and we’ll figure it out.

Frequently Asked Questions

What are the average home insurance costs in the U.S. right now?

The average homeowners insurance cost typically ranges from $1,500 to $2,500 annually for a $300,000 home. Homeowners insurance rates vary based on factors like state, zip code, the year the home was built, and dwelling coverage amount. Areas prone to coastal and wildfire risks, such as certain parts of California, often face higher insurance costs due to increased rebuilding expenses.

Why do my home insurance rates differ from my neighbor’s?

Insurers determine homeowners insurance rates based on address, home characteristics, and individual factors. Elements like roof age, claims history, and credit in many states, along with construction type and certain fire or flood exposure, can significantly affect the average homeowners insurance cost.

What’s driving recent rate hikes?

Rebuilding costs, inflation, and supply chain delays are contributing to the rise in homeowners insurance rates, while CAT losses and claims from wildfires, windstorms, hail, and water damage further elevate the average homeowners insurance cost, reducing competition in higher risk states.

How can I lower my premium without losing protection?

To lower your homeowners insurance cost, consider raising your deductible, bundling auto and home policies, and installing monitored alarms. Additionally, harden your home against fire and wind while checking coverage selections and limits every year for potential discounts.

What coverage limits should I choose for real value?

Be certain the average homeowners insurance cost includes coverage for extended or guaranteed replacement if offered. Schedule valuables, and maintain your personal liability at a minimum of $300,000 to $500,000 to manage homeowners insurance rates.

Do I need coverage beyond a standard HO-3 policy?

Usually, yes! Consider homeowners insurance coverage like flood insurance from FEMA or private sources, earthquake coverage in California, and higher liability or an umbrella policy. These add-ons help fill typical gaps in homeowners insurance costs and safeguard savings and future earnings.

How often should I review my home insurance?

Review yearly or after significant changes like renovations, roof replacement, or major purchases. Refresh your inventory and pictures, and have your agent re-run the average homeowners insurance cost and available discounts. These regular check-ins help you avoid being underinsured and overpaying on homeowners insurance premiums.