Table of Contents

- How to Bundle Home and Auto Insurance: What It Actually Means

- Multi-Policy Insurance Discount: How Much Can You Really Save?

- Pros and Cons of Bundling Insurance: An Honest Assessment

- Step-by-Step: How to Bundle Home and Auto the Right Way

- How to Compare Insurance Policies Before You Commit

- Using an Insurance Bundle Savings Calculator Effectively

- Coverage Options, Claims Process, and Flexible Payment Options

- Conclusion

Last Updated: June 7, 2026

Knowing how to bundle home auto insurance is one of the most straightforward ways to reduce what you pay for coverage each year, yet most policyholders never do it correctly. This guide from Covera walks you through every step: what qualifies as a bundle, how credit scores affect your premium, what the claims process looks like when policies are combined, and how to use a post-quote comparison checklist before you bind anything.

The discount you receive depends on underwriting criteria, your state’s regulatory environment, your driving record, and factors most people never think to ask about. Get those details right and the savings are real. Get them wrong and you’ll end up with coverage gaps you won’t discover until you file a claim.

How to Bundle Home and Auto Insurance: What It Actually Means

Bundling home and auto insurance means purchasing both policies from the same carrier under a single policyholder account, which typically qualifies you for a multi-policy discount applied to one or both premiums. The carrier treats you as a lower-risk, higher-value customer and passes some of that value back as reduced annual premiums.

What Qualifies as a Bundle

Not every combination of policies counts as a bundle for discount purposes. Most carriers require both policies be active simultaneously, issued under the same name, and tied to the same billing account. Renters insurance paired with auto often qualifies, as does condo insurance. A standalone umbrella policy may or may not trigger a multi-policy discount depending on the insurer. Ask the licensed insurance agent directly which combinations qualify before you request an auto insurance quote.

Insurance Literacy for First-Time Buyers: Key Terms to Know

First-time buyers often enter the bundling process without a working vocabulary, which puts them at a disadvantage. Here are the terms that matter most:

- Premium: The amount you pay for your policy, typically monthly or annually.

- Deductible: The out-of-pocket amount you pay before your insurer covers a claim.

- Coverage limits: The maximum amount your insurer will pay for a covered loss.

- Liability coverage: Pays for damage or injury you cause to others.

- Collision insurance: Covers damage to your vehicle from an accident, regardless of fault.

- Comprehensive coverage: Covers non-collision damage such as theft, weather, or fire.

- Underwriting: The process insurers use to evaluate risk and set your premium.

- Bind policy: The moment your coverage officially takes effect after you accept a quote.

When reviewing your first bundle quote, ask the agent to show you the coverage limits for both policies side by side. A low premium with inadequate coverage limits is not a deal; it’s a liability.

Multi-Policy Insurance Discount: How Much Can You Really Save?

The multi-policy insurance discount varies significantly by carrier, state, and individual risk profile. Treat advertised savings figures as directional, not guaranteed. What’s consistent: the discount is almost always a percentage reduction applied to annual premiums, and it’s typically larger on the home policy than the auto policy.

How Credit Scores Affect Your Bundled Premium

Insurers use a credit-based insurance score, similar to but distinct from your standard credit score, to predict the likelihood of a future claim. A higher score generally means lower premiums, and when you bundle, this effect compounds across both policies simultaneously.

If your credit score is lower than you’d like, spend a few months improving it before shopping. Paying down revolving debt and correcting credit report errors are the two fastest levers. According to the Consumer Financial Protection Bureau’s guidance on credit reports, consumers are entitled to a free credit report annually from each major bureau, a logical first step before any major insurance purchase.

State-Specific Regulatory Nuances That Affect Bundle Savings

Not every state allows insurers to use credit scores in pricing. California, Massachusetts, Michigan, and Hawaii prohibit or restrict the practice. In those states, zip code, claims history, and driving record carry more weight instead.

State minimum coverage requirements also affect how much room you have to customize a bundle. Before you get your first auto insurance quote, look up your state’s minimums through your state insurance commissioner’s website to evaluate whether a carrier’s bundle offer actually meets your needs.

Pros and Cons of Bundling Insurance: An Honest Assessment

The case for bundling:

- Simplified account management: one carrier, one portal, one renewal date.

- Multi-policy discount reduces annual premiums on one or both policies.

- Single claims process when one event damages both home and vehicle simultaneously.

- Some carriers offer loyalty discounts that compound over time.

The case against bundling:

- Bundling can create complacency, many policyholders stop shopping and miss better rates.

- If one policy becomes uncompetitive, exiting the carrier relationship is harder.

- A carrier that excels at auto may offer mediocre home coverage, or vice versa.

- Discount eligibility can change at renewal without warning.

The honest take: bundling makes sense for most people, most of the time, but it should not be a permanent set-it-and-forget-it decision. Revisit your coverage at every renewal.

Do not assume your bundle discount is locked in permanently. Carriers can adjust discount eligibility at renewal based on changes to your risk profile, claims history, or internal pricing models. Review both policies annually.

Step-by-Step: How to Bundle Home and Auto the Right Way

Total Time: 2-3 hours across 2-3 days

Difficulty: Beginner to Intermediate

Step 1: Gather Your Personal Information and Coverage Details

Before you request a single quote, collect the following:

- Driver’s license numbers for all drivers in your household

- Vehicle identification numbers (VINs) for all vehicles

- Current auto insurance declarations page

- Home address, year built, square footage, and construction type

- Current home insurance declarations page

- Your Social Security number (for credit-based underwriting)

- Claims history for the past three to five years

Having this information ready reduces errors and ensures the quote reflects your actual risk profile.

Step 2: Get an Auto Insurance Quote Alongside Your Home Quote

Request both quotes simultaneously from the same carrier. Getting your auto quote first and adding home coverage as an afterthought is a common mistake, carriers price bundles as a package, and getting both together ensures the multi-policy discount is applied correctly from the start. Use the carrier’s online portal for an initial estimate, then follow up with a licensed agent to confirm details, especially for add-ons like rideshare insurance or specialty coverage.

Step 3: Review Coverage Options, Limits, and Deductibles

Compare the following across every quote:

- Liability coverage limits (per person, per accident, property damage)

- Collision insurance deductible vs. premium trade-off

- Comprehensive coverage limits and exclusions

- Home dwelling coverage vs. replacement cost

- Personal property coverage limits

- Loss of use provisions

Pay particular attention to whether the home policy covers replacement cost or actual cash value. Replacement cost pays what it costs to rebuild; actual cash value subtracts depreciation.

Step 4: Confirm Discount Eligibility and Bind Your Policy

Before you bind policy, verify the following in writing:

- Multi-policy discount is applied to both policies (or confirm which one)

- Paperless billing discount has been applied if you opted in

- Payment frequency discount is reflected (annual payment often costs less than monthly)

- Discount eligibility criteria are documented

- Coverage start dates align for both policies

Once confirmed, binding is typically done through the carrier’s online portal or by phone with your agent. Keep copies of both declarations pages.

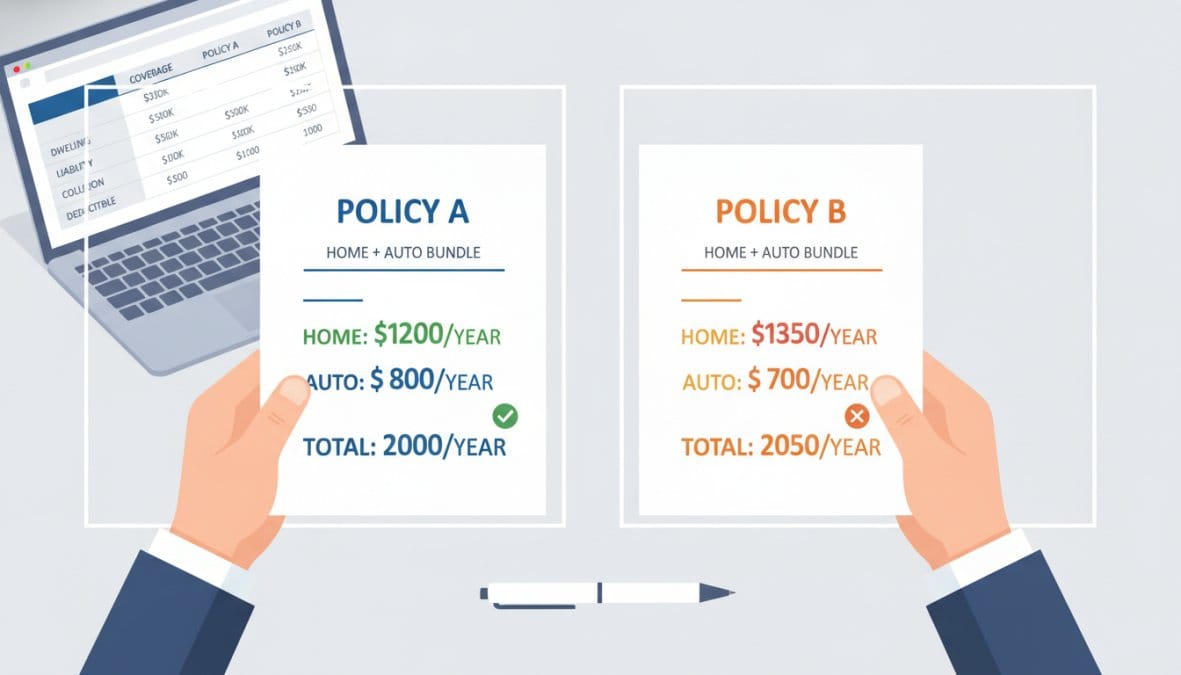

How to Compare Insurance Policies Before You Commit

The biggest mistake in insurance shopping is comparing premiums without comparing coverage. A cheaper quote may carry a higher deductible, lower liability limits, or exclusions that only surface at claim time.

Post-Quote Comparison Checklist

Use this checklist when evaluating any bundle offer before you commit:

- Are the liability coverage limits the same across all quotes being compared?

- Are the deductibles identical, or have you adjusted for the premium difference?

- Does the home policy cover replacement cost or actual cash value?

- Are there any coverage exclusions specific to your zip code or property type?

- Is rideshare insurance included or available as an add-on if needed?

- What is the carrier’s customer satisfaction rating with your state’s insurance department?

- How does the claims process work, and what is the average claim resolution time?

- Are flexible payment options available without a fee?

- Is the multi-policy discount guaranteed at renewal, or subject to change?

- What happens to the discount if you cancel one policy mid-term?

According to the National Association of Insurance Commissioners’ consumer resources, your state insurance department maintains complaint ratio data for every licensed carrier, one of the most underused tools in insurance shopping.

Using an Insurance Bundle Savings Calculator Effectively

An insurance bundle savings calculator estimates the combined premium cost of bundled policies versus separate policies, showing projected annual savings from the multi-policy discount. Most major carriers offer one on their websites, and independent comparison platforms provide carrier-agnostic versions.

The output is only as accurate as the input. Entering estimated figures rather than your actual coverage details, VIN, or claims history produces a rough estimate that may differ significantly from your actual quote. Use the calculator as a first-pass filter to identify which carriers are worth pursuing, not as a decision tool.

A more useful application: run the calculator with your current coverage limits as inputs, then compare the result to your existing premiums. This tells you whether bundling with a new carrier actually saves money, or whether it’s just cheaper because the coverage is inferior.

An insurance bundle savings calculator is a starting point, not a decision tool. Always get a full quote with your actual personal information before drawing conclusions about potential savings.

Coverage Options, Claims Process, and Flexible Payment Options

Most policyholders focus entirely on price and almost never on the claims process, the moment when your coverage actually matters. Here’s what you need to know before committing to a bundle.

Liability, Collision, and Comprehensive Coverage in a Bundle

Bundled policies don’t change the fundamental structure of your coverage, but they create an opportunity to review both policies simultaneously.

| Coverage Type | What It Covers | Applies To | Deductible? |

|---|---|---|---|

| Liability coverage | Damage/injury you cause to others | Auto | No |

| Collision insurance | Damage to your vehicle from an accident | Auto | Yes |

| Comprehensive coverage | Non-collision damage (theft, weather) | Auto | Yes |

| Dwelling coverage | Structure of your home | Home | Yes |

| Personal property | Contents of your home | Home | Yes |

| Loss of use | Temporary housing if home is uninhabitable | Home | No |

Confirm that your liability coverage limits are consistent across both policies. A mismatch, auto liability at state minimum but home liability at a higher limit, is a common coverage gap that leaves you exposed in certain scenarios.

How the Claims Process Works When Policies Are Bundled

When a single event damages both your home and vehicle, a hailstorm or a tree falling on your car in your driveway, you file one claim with one carrier. The carrier coordinates assessment across both policies, meaning one adjuster, one timeline, and one resolution process.

One nuance: even with a bundle, each policy carries its own deductible. A storm that damages your roof and your car means you pay both deductibles separately. Some carriers offer a single-deductible provision for multi-policy claims, but it’s not standard, ask about it specifically. As documented in the Insurance Information Institute’s guidance on filing claims, documenting damage thoroughly before any repairs begin is one of the most important steps in any claims process.

Flexible Payment Options and Paperless Discounts

Most carriers offer monthly, quarterly, semi-annual, or annual payment for bundled policies. Annual payment typically results in the lowest total cost, and paperless billing discounts, while small, are among the easiest discount eligibility boxes to check.

Watch for carriers that charge a fee for monthly payment plans. If you’re comparing a bundle quote assuming monthly payment against a competitor’s quote assuming annual payment, you’re not making a fair comparison. Standardize the payment frequency before drawing conclusions about which offer is better.

Insurance shopping is genuinely confusing, and the bundling process has more variables than most guides acknowledge. Covera exists to cut through that complexity, offering detailed policy breakdowns, side-by-side comparison resources, and expert guidance across auto, home, and specialty insurance. Whether you’re a first-time buyer trying to understand your coverage options or an existing policyholder wondering if your current bundle still makes sense, Covera’s comparison resources give you the information you need to make a confident decision. Get started with Covera and approach your next renewal with a clear picture of what your coverage actually covers.

Frequently Asked Questions

Is it always cheaper to bundle home and auto insurance?

Bundling home and auto insurance typically lowers your overall premium through a multi-policy insurance discount, but it is not guaranteed to be the cheapest option in every situation. In some cases, purchasing separate policies from different carriers may yield lower annual premiums. Always use a side-by-side comparison and an insurance bundle savings calculator to verify that the bundled total beats the combined cost of standalone policies before you bind your policy.

What should I look for when comparing bundled insurance quotes?

When comparing bundled quotes, review coverage limits, deductibles, and any coverage gaps rather than focusing solely on price. Check that liability coverage, collision insurance, and comprehensive coverage meet your state minimum requirements and personal needs. Confirm discount eligibility, flexible payment options, and whether the carrier offers a convenient online portal for managing both policies. Use a post-quote comparison checklist to evaluate each offer consistently across carriers.

Does bundling home and auto insurance simplify the claims process?

Yes, bundling generally simplifies the claims process because you work with a single licensed insurance agent and one insurance company for both policies. This is especially valuable when an incident affects both your home and vehicle simultaneously, for example, a severe storm that damages your roof and your car. Having one policyholder account, one point of contact, and coordinated underwriting can reduce paperwork and speed up resolution.

Can I bundle other types of insurance besides home and auto?

Most major carriers allow you to extend a multi-policy bundle beyond home and auto to include renters, life, umbrella, rideshare insurance, and even some specialty policies. Each additional policy added to a bundle may increase your discount eligibility. Ask your licensed insurance agent which combinations qualify for the deepest savings and whether adding a third policy meaningfully reduces your annual premiums compared to carrying it separately.

How does my credit score affect my bundled insurance premium?

In most U.S. states, insurers use a credit-based insurance score during underwriting to help determine your premium. A higher credit score generally signals lower risk to the carrier, which can result in more affordable rates on both your home and auto policies. Because bundling combines both premiums under one carrier, the impact of your credit score is amplified, improving your score before shopping for a bundle can meaningfully lower your total annual cost.