Table of Contents

- Best Health Insurance for Freelancers: Top Options Compared

- How to Get Affordable Health Insurance as Self-Employed

- Health Insurance Subsidies for Self-Employed Workers

- Health Insurance Tax Deduction for Freelancers: Step-by-Step

- Top Health Insurance Providers for Independent Contractors

- Plan Types and Network Options for Freelancers

- Common Mistakes Freelancers Make When Choosing Coverage

- Special Considerations: International Nomads and Coverage Gaps

Last Updated: June 27, 2026

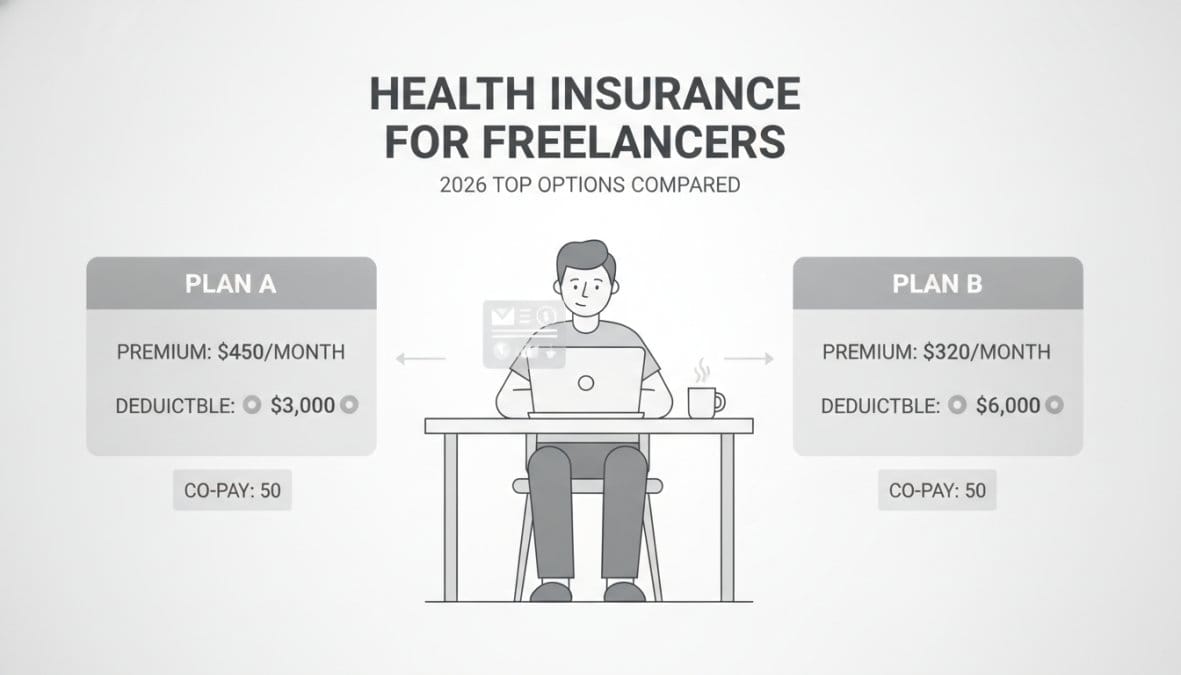

Best Health Insurance for Freelancers: Top Options Compared

Finding the best health insurance for freelancers requires balancing affordability, coverage depth, and flexibility. Self-employed workers often spend more on health coverage than traditional employees while receiving fewer plan options. The difference between a plan that works and one that drains your budget comes down to understanding subsidies, plan types, and where to find group-rate benefits most freelancers never discover.

| Insurance Option | Best For | Starting Price | Key Advantage |

|---|---|---|---|

| HealthCare.gov Marketplace | Most U.S. freelancers | Varies by income | Income-based subsidies |

| Stride Health | Marketplace navigation | Free platform | Simplified enrollment |

| Opolis | Full-time freelancers | Contact for pricing | Group-rate networks |

| Blue Cross Blue Shield | Large provider networks | Varies by state | Nationwide acceptance |

| Oscar Health | Tech-savvy freelancers | Varies by state | Mobile-first experience |

| Kaiser Permanente | Regional users | Varies by region | Integrated care model |

| Freelancers Union | Community-driven support | Free membership | Educational resources |

The single biggest mistake freelancers make is ignoring the Health Insurance Marketplace entirely. Many assume they don’t qualify for subsidies or think enrollment is too complicated. In reality, your actual income often qualifies you for substantial tax credits that reduce your monthly premium to a fraction of what you’d pay directly.

How to Get Affordable Health Insurance as Self-Employed

Affordable coverage starts with understanding your Modified Adjusted Gross Income (MAGI), not your business revenue. This number determines subsidy eligibility and amounts. Underestimating means owing back subsidies at tax time; overestimating leaves money on the table.

The Affordable Care Act created the Health Insurance Marketplace specifically for self-employed workers. Open Enrollment runs November 1 through January 15 annually, though qualifying life events trigger Special Enrollment Periods outside these dates.

Qualifying for ACA Marketplace Plans

To qualify, you must be a U.S. citizen or lawful resident with a valid Social Security number. For 2026, a single freelancer earning under approximately $54,000 qualifies for premium tax credits. The enrollment process takes 15-30 minutes on HealthCare.gov, where you enter projected income, household size, and location, then compare plans showing actual costs after subsidies.

Understanding Premium Tax Credits

Premium tax credits are direct subsidies reducing your monthly payment, calculated based on income and your region’s benchmark plan. The government determines how much you should pay as a percentage of income (roughly 0-8.5%), and any difference becomes your tax credit.

A conservative approach: if unsure whether you’ll earn $40,000 or $50,000, estimate $50,000. Lower actual income yields a larger refund; higher income avoids penalties. Tax credits apply to any plan you choose, not just Silver plans. A Bronze plan with tax credits can cost $0-50 monthly while covering catastrophic illness.

Failing to report income changes creates serious tax consequences. If your income jumps mid-year, notify the marketplace within 30 days. Failure to do so means owing back subsidies at tax time, potentially thousands of dollars.

Health Insurance Subsidies for Self-Employed Workers

Subsidies come in two forms: premium tax credits reducing monthly payments and cost-sharing reductions lowering deductibles and out-of-pocket maximums.

Eligibility Based on Income

For 2026, eligibility thresholds are:

- Below 100% of poverty line: not eligible for marketplace (likely qualify for Medicaid)

- 100-400% of poverty line: eligible for premium tax credits and cost-sharing reductions

- Above 400% of poverty line: eligible for marketplace plans but no subsidies

For a single person, 400% of the poverty line is approximately $54,000. For a family of four, roughly $111,000. Many six-figure freelancers qualify for subsidies because thresholds are calculated per household member.

How to Apply for Subsidies

Create an account on HealthCare.gov during Open Enrollment and estimate your Modified Adjusted Gross Income (MAGI) for the upcoming year. For self-employed people, MAGI is generally net business income plus other income sources. Base estimates on your previous year’s tax return, adjusting for current business trends. You can update income estimates anytime during the year if circumstances change.

Health Insurance Tax Deduction for Freelancers: Step-by-Step

The self-employed health insurance deduction allows you to deduct health insurance premiums from taxable income, reducing your federal tax bill dollar-for-dollar. Unlike traditional employees, freelancers must claim this deduction manually.

Calculating Your Deductible Premiums

Deduct premiums you personally paid, not subsidies the marketplace provided. If your monthly premium is $500 and you receive a $300 tax credit, deduct $200 monthly ($2,400 annually). The deduction appears on Form 1040, Schedule 1, reducing both income tax and self-employment tax.

Track monthly premiums in a spreadsheet. Most insurance providers send annual statements showing total premiums paid, simplifying year-end calculation.

Documentation and Record-Keeping

Keep your insurance provider’s annual statement, your tax return showing the deduction claimed, and marketplace statements showing subsidy amounts. The IRS rarely audits this deduction because documentation is straightforward. Maintain records for three years.

The self-employed health insurance deduction is the easiest way to reduce your tax bill. If you pay $500 monthly for insurance, that’s $6,000 annually in deductions. At a 24% tax rate, that’s $1,440 in federal tax savings.

Top Health Insurance Providers for Independent Contractors

The best provider depends on your priorities: lowest cost, largest network, digital experience, or group-rate access.

HealthCare.gov Marketplace: Government-Backed Coverage

The Health Insurance Marketplace is where subsidies live. It operates during Open Enrollment (November 1 – January 15) and Special Enrollment Periods triggered by qualifying life events. HealthCare.gov shows plans from all carriers in your area, filtered by metal level and sorted by monthly premium after subsidies. The “Find Care Providers” tool verifies whether your preferred doctors and hospitals are in-network before enrollment.

Stride Health: Simplified Marketplace Navigation

Stride Health removes friction from marketplace enrollment by creating personalized recommendations based on your health needs, medications, and doctors. The platform is free; Stride earns referral fees from carriers. For freelancers with specific healthcare needs, Stride calculates which plans keep you in-network for all doctors and medications, showing true costs including anticipated out-of-pocket expenses. The platform also integrates tax and expense tracking, automating your tax deduction calculation.

Opolis: Group-Rate Benefits for Freelancers

Opolis aggregates thousands of freelancers into a large group, negotiating rates with carriers like Cigna that are typically 15-30% lower than individual marketplace plans. The cooperative handles payroll, tax withholding, and quarterly estimated tax calculations. Opolis provides HSA-eligible plans, allowing pre-tax contributions that reduce taxable income further. The trade-off is complexity; setup requires more paperwork than marketplace enrollment. For full-time freelancers earning six figures, premium savings and tax deductions justify this complexity.

Major Carriers: BCBS, Kaiser, Oscar, Cigna, Aetna

Blue Cross Blue Shield operates in all 50 states with extensive provider networks, ideal if you prioritize access to the widest range of doctors and hospitals. Kaiser Permanente integrates insurance with its own hospitals and clinics, creating seamless care coordination but locking you into Kaiser’s network. Oscar Health prioritizes digital experience with an excellent mobile app and transparent claims processing, ideal for tech-savvy freelancers. Cigna offers global coverage options for freelancers who travel internationally. Aetna integrates with CVS Health’s MinuteClinic network, providing convenient urgent care access.

Freelancers Union: Community-Driven Resources

Freelancers Union is a nonprofit membership organization providing free resources, advocacy, and curated insurance recommendations. The union maintains directories of insurance brokers specializing in freelancer coverage and provides educational resources on taxes and legal issues. Local chapters host networking events, workshops, and peer support groups, offering valuable community for solo freelancers.

Plan Types and Network Options for Freelancers

Understanding plan types is essential because they dramatically affect actual costs and flexibility.

HMO vs. PPO vs. EPO Explained

Health Maintenance Organizations (HMOs) require choosing a primary care physician who coordinates care. Referrals are required for specialists, and out-of-network care is covered only in emergencies. HMOs have the lowest premiums and out-of-pocket costs.

Preferred Provider Organizations (PPOs) offer maximum flexibility. You can see any doctor without referrals, and out-of-network care is covered at higher cost. PPOs have higher premiums but lower out-of-pocket costs when you need care.

Exclusive Provider Organizations (EPOs) lock you into the network but don’t require referrals to see specialists. EPOs cost less than PPOs but more than HMOs.

For freelancers, choose based on your situation. If you’re healthy, an HMO’s low premium is attractive. If you have established doctors or anticipate significant healthcare needs, a PPO’s flexibility justifies higher cost. EPOs work well for freelancers wanting flexibility without PPO premiums.

HSA-Eligible Plans: Maximize Tax Savings

Health Savings Accounts are triple-tax-advantaged: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. To open an HSA, enroll in a High Deductible Health Plan (HDHP) with a deductible of at least $1,500 for individual coverage or $3,000 for family coverage in 2026.

Strategy: contribute the maximum ($4,150 for individual coverage in 2026) annually, pay current medical expenses out of pocket, and let the HSA grow tax-free. After age 65, withdraw HSA funds for any purpose without penalty, though non-medical withdrawals are taxed as income.

An HDHP with a $2,000 deductible might cost $150 monthly while a traditional plan costs $300 monthly. The $150 monthly savings ($1,800 annually) can be contributed to your HSA, making the higher deductible cost-neutral while building a tax-free medical fund.

If you’re healthy with emergency savings, an HDHP paired with HSA contributions is the most tax-efficient health insurance strategy available. You’re converting health insurance premiums into tax-deductible savings that compound tax-free.

Common Mistakes Freelancers Make When Choosing Coverage

The biggest mistake is choosing based on monthly premium alone without considering deductibles and out-of-pocket maximums. A $100 monthly plan with a $5,000 deductible might cost more overall than a $250 monthly plan with a $1,500 deductible if you anticipate healthcare needs.

A second error is ignoring subsidies because you assume you don’t qualify. Many freelancers earning $50,000-$80,000 qualify for substantial subsidies. Spending 15 minutes on HealthCare.gov to verify eligibility is worth thousands in potential savings.

Another mistake is re-enrolling in last year’s plan without comparing current options. Carriers adjust premiums and plan designs annually; what was optimal last year might be suboptimal now.

A final costly error is failing to report income changes. If you get a major client mid-year and your income jumps, notify the marketplace. Failing to do so creates a tax bill surprise in April.

Special Considerations: International Nomads and Coverage Gaps

Freelancers working internationally face unique challenges because standard U.S. health insurance doesn’t cover care outside the country.

Health Insurance for International Digital Nomads

U.S. marketplace plans won’t cover care received abroad. Several approaches address this: maintain U.S. marketplace coverage for catastrophic emergencies and purchase separate international health insurance for routine care through companies like Cigna Global or World Nomads. Alternatively, purchase local health insurance in countries where you spend most of your time. Mexico, for example, offers private health insurance for $50-150 monthly with excellent coverage.

Understand your actual needs. In countries with excellent healthcare infrastructure (Western Europe, Canada, Australia), local insurance is often sufficient. In developing countries with limited healthcare quality, maintaining U.S. marketplace coverage as backup is prudent.

Short-Term vs. Long-Term Plan Risks

Short-term health plans lasting 30-364 days are cheap ($50-100 monthly) because they exclude pre-existing conditions and provide minimal coverage. They’re appropriate only as true temporary bridges while arranging real coverage, not as ongoing solutions.

Long-term coverage through the marketplace or group plans like Opolis provides comprehensive protection. The higher premium reflects actual insurance value, covering pre-existing conditions, preventive care, hospitalization, and prescription drugs. Choosing short-term coverage to save money risks discovering when you need care that the plan doesn’t cover what you expected.

Navigating health insurance as a freelancer is complex, but the core strategy is simple: use the Health Insurance Marketplace to access subsidies, calculate your tax deduction accurately, and choose a plan matching your actual healthcare needs rather than just the lowest premium. Start by spending 15 minutes on HealthCare.gov to verify your subsidy eligibility; the potential savings justify the time investment.

Frequently Asked Questions

How do freelancers qualify for health insurance subsidies?

Freelancers qualify for subsidies through the Health Insurance Marketplace based on Modified Adjusted Gross Income (MAGI). If your income falls between 100% and 400% of the federal poverty line, you may be eligible for Premium Tax Credits. You must enroll during Open Enrollment or a Special Enrollment Period following a Qualifying Life Event. Income verification is required when applying through HealthCare.gov.

Is health insurance tax deductible for freelancers?

Yes. Self-employed individuals can deduct 100% of their health insurance premiums as a business expense, including medical, dental, and vision coverage. This deduction is taken on Form 1040 and doesn’t require itemizing. However, you cannot claim this deduction if you’re eligible for employer-sponsored coverage through a spouse’s job. Keep detailed records of all premium payments for documentation.

What’s the best health insurance option for freelancers on a tight budget?

The Health Insurance Marketplace (HealthCare.gov) typically offers the most affordable options for budget-conscious freelancers, especially those earning under $50,000 annually who qualify for Premium Tax Credits and subsidies. Silver-level ACA plans combined with subsidies can significantly reduce monthly costs. Alternatively, HSA-eligible Bronze plans paired with a Health Savings Account offer tax advantages and lower premiums, though they have higher deductibles.

How do international digital nomads find health insurance coverage?

International freelancers have limited options through standard U.S. marketplaces. Cigna offers global coverage plans designed for expatriates and frequent travelers. Alternatively, some digital nomads use international health insurance providers or maintain coverage in their home country. If you’re abroad long-term, you may not qualify for ACA plans. Research whether you need continuous U.S. coverage or if international insurance better suits your travel schedule.