If you work in California, you probably have questions about health insurance through your employer. Is it really the best choice for you and your family?

Understanding how employer-sponsored health plans work can save you money and protect your health. You might be surprised to learn that while employer plans often offer lower premiums and tax benefits, they aren’t always the cheapest or best fit for everyone.

You’ll discover what makes employer health insurance in California unique, when it’s a smart option, and how to compare it with other choices like Covered California or private plans. Keep reading to make the most informed decision about your health coverage—and your wallet.

Employer Health Plans In California

Employer health plans in California provide many workers with access to affordable medical coverage. These plans help employees manage health care costs while offering important benefits. California has specific rules that employers must follow when offering health insurance. Understanding these rules and common plan types helps employees make better choices about their coverage.

Legal Requirements For Employers

California law requires employers with 50 or more full-time employees to offer health insurance. The coverage must meet minimum value and affordability standards. Employers must provide written notices about health plan options to employees. They also need to comply with federal laws like the Affordable Care Act. Failure to follow these rules can lead to penalties for employers. These laws protect workers by ensuring they have access to essential health benefits.

Common Plan Types Offered

Most California employers offer group health insurance plans. Preferred Provider Organization (PPO) plans are popular for flexibility in choosing doctors. Health Maintenance Organization (HMO) plans require members to use a network of providers. High Deductible Health Plans (HDHP) paired with Health Savings Accounts (HSA) help lower premiums. Some employers also provide Exclusive Provider Organization (EPO) plans that limit out-of-network care. Each plan type has different costs and coverage options. Employees should review plan details to find the best fit for their needs.

Credit: www.coveredca.com

Cost Advantages Of Employer Coverage

Employer health insurance in California offers clear cost advantages. These plans reduce the financial burden on employees. The savings come from shared premiums, tax benefits, and risk pooling. Understanding these factors helps you see why employer coverage is often more affordable.

Shared Premiums And Employer Contributions

Employers pay a portion of your health insurance premiums. This lowers the amount you must pay each month. Sharing costs makes health coverage more accessible. It also helps employees avoid large upfront expenses. Employer contributions reduce your overall healthcare spending.

Tax Benefits Of Employer Plans

Premiums for employer health plans are deducted before taxes. This lowers your taxable income and saves money. You pay less in federal and state income taxes. Tax benefits make employer coverage more affordable than individual plans. These savings add up over the course of a year.

Risk Pooling And Lower Premiums

Employer plans cover many employees together. This spreads the health risk across a large group. Insurers charge lower premiums for groups than individuals. Risk pooling prevents high costs from falling on one person. Group plans often offer better rates and benefits.

When Employer Coverage May Not Be Best

Employer health insurance in California often seems like the easiest choice. It offers convenience and usually costs less because employers share the premium. Still, this coverage may not always meet your needs or save you money.

Some situations make employer health plans less ideal. Understanding these can help you decide if another option fits better.

High Income And Subsidy Eligibility

High earners often do not qualify for government subsidies. Subsidies lower monthly payments on Marketplace plans. If your income is above a certain level, you lose this help. Employer coverage might then be more expensive than Marketplace options. Choosing a Marketplace plan can sometimes save money for high-income workers.

Plan Design Limitations

Employer plans may have limited choices. You might face high deductibles or narrow provider networks. This means you pay more out-of-pocket or cannot see preferred doctors. Some plans exclude important benefits or have strict rules. These limits reduce the value of employer coverage.

Low Employer Contributions

Some employers pay very little toward premiums. You then pay most of the cost yourself. This can make employer insurance pricey. Marketplace plans could offer better prices or benefits. Check how much your employer contributes before deciding. Low contributions can turn a good deal into a costly one.

Comparing Employer Plans With Marketplace Options

Choosing between employer health insurance and Marketplace options in California requires careful thought. Each option has its own benefits and costs. Understanding these differences helps you decide which plan fits your needs and budget best.

Evaluating Total Costs

Employer plans often share premium costs with employees. This lowers the monthly payment you make. Marketplace plans may have subsidies based on income. These subsidies can reduce your premium significantly. Check both options for total yearly costs. Include premiums, deductibles, and other fees. This gives a clear picture of your actual spending.

Coverage And Network Differences

Employer plans usually have a fixed network of doctors and hospitals. You must use these providers to get full benefits. Marketplace plans offer more flexibility in choosing doctors. But some may have smaller networks or fewer covered services. Review the list of covered providers carefully. Confirm your preferred doctors and hospitals are included.

Out-of-pocket Expenses

Out-of-pocket costs include deductibles, copayments, and coinsurance. Employer plans often have lower deductibles because of group bargaining power. Marketplace plans may have higher out-of-pocket limits. Consider how often you visit doctors or need prescriptions. A plan with lower out-of-pocket expenses can save money if you use healthcare frequently.

Steps To Choose The Right Health Insurance

Choosing the right health insurance through your employer in California requires careful thought. Each plan has unique features that affect your costs and coverage. Follow clear steps to find a plan that fits your needs and budget. This helps avoid unexpected expenses and ensures access to needed care.

Reviewing Employer Plan Details

Start by examining the health insurance plans your employer offers. Look at the monthly premiums and how much the employer contributes. Check deductibles, copayments, and out-of-pocket limits. Review the list of covered services and network of doctors. Confirm if your preferred doctors and hospitals are included. Understanding these details helps you compare plans effectively.

Checking Marketplace Plans And Subsidies

Compare employer plans with options on Covered California, the state’s health insurance marketplace. Marketplace plans may offer subsidies based on your income. These subsidies lower monthly costs and can make plans more affordable. Review coverage benefits and costs on marketplace plans too. Sometimes a marketplace plan with subsidies costs less than employer coverage.

Assessing Personal And Family Health Needs

Think about your health and that of your family members. Consider any ongoing treatments, medications, or planned procedures. Factor in how often you visit doctors or specialists. Choose a plan that covers your needs well and offers good provider access. Match your plan choice to your typical health care usage to avoid surprise bills.

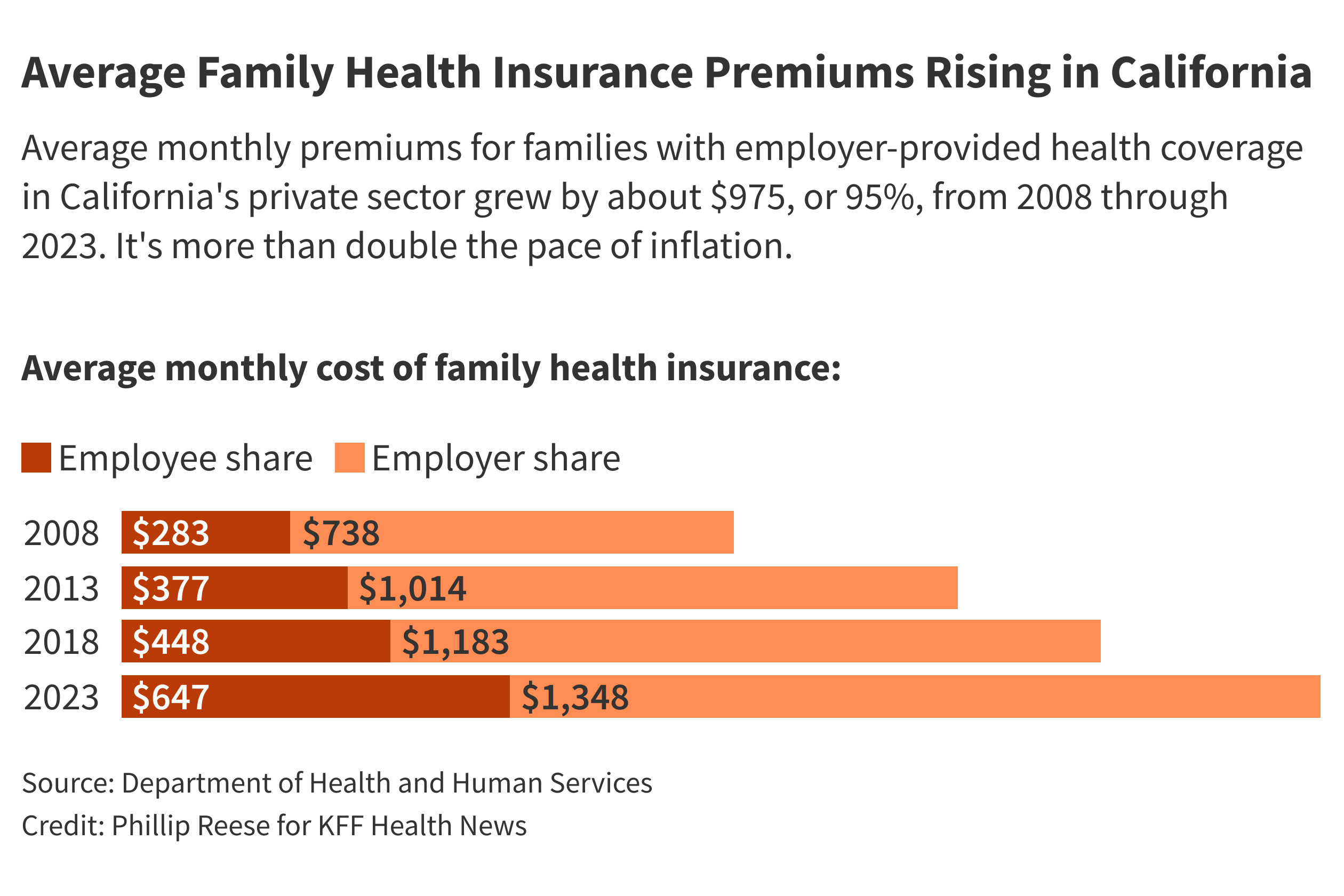

Credit: kffhealthnews.org

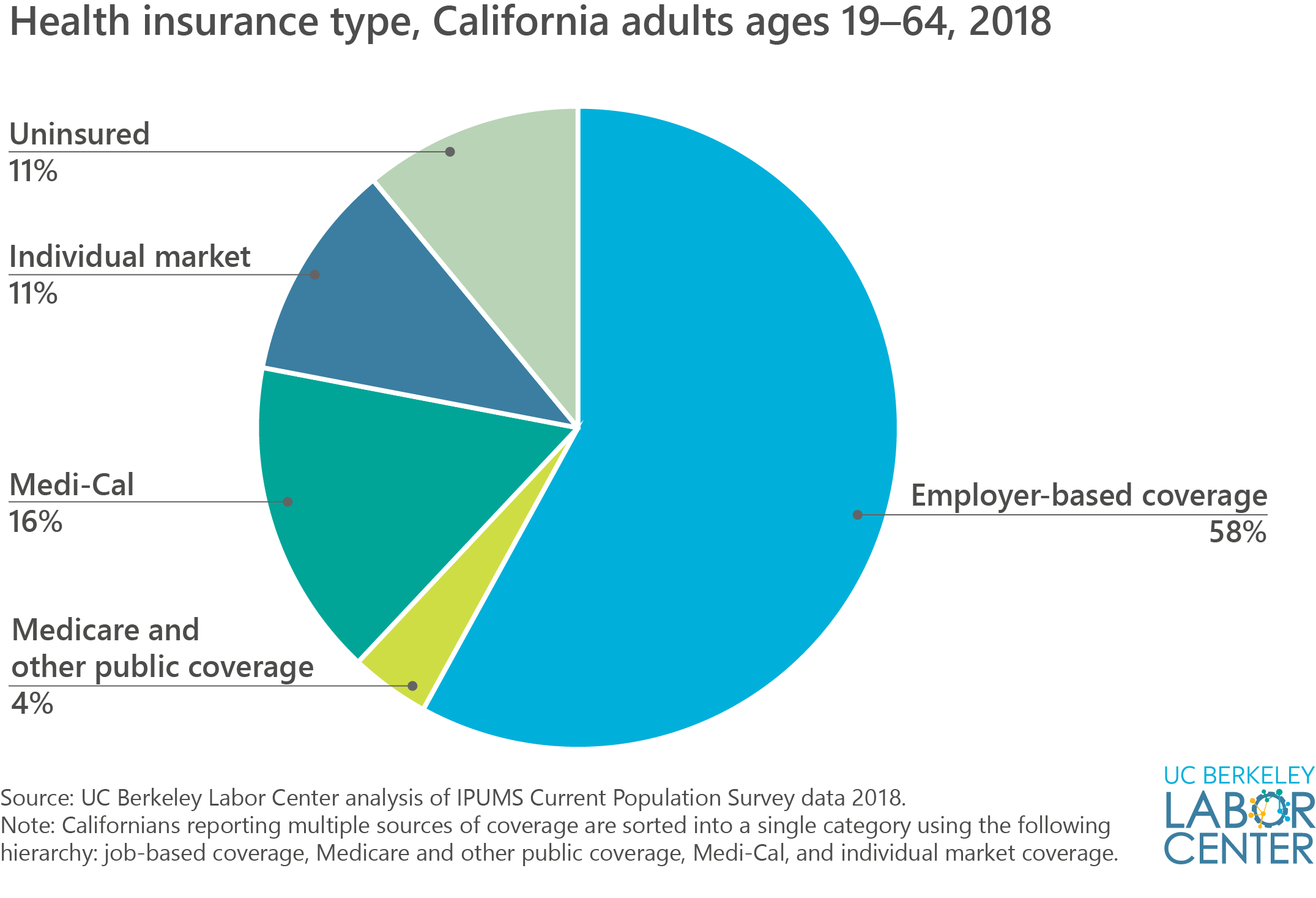

Credit: laborcenter.berkeley.edu

Frequently Asked Questions

Is It Better To Get Insurance Through Work Or Covered In California?

Getting insurance through work usually costs less due to shared premiums and tax benefits. Covered California offers subsidies and more plan choices. Compare costs, coverage, and employer contributions to decide which suits your health needs and budget best.

What Is The Law On Employers Providing Health Insurance In California?

California law requires employers with 50 or more full-time employees to offer health insurance. Plans must meet state and federal standards. Employers must provide affordable coverage or face penalties. Small employers are encouraged but not mandated to provide insurance. Employee eligibility and plan details vary by employer.

Is It Better To Get Health Insurance Through Your Employer?

Employer health insurance often costs less due to shared premiums and tax benefits. Compare plans and costs before deciding.

Is It Always Cheaper To Get Health Insurance Through An Employer?

Employer health insurance often costs less due to shared premiums and tax benefits. Costs vary by income, plan design, and employer contribution. Some individual Marketplace plans may be cheaper or offer better coverage. Always compare your employer’s offer with Marketplace options before deciding.

Conclusion

Choosing health insurance through your California employer often saves money. Employers share premium costs, lowering your monthly payments. Plans usually offer better coverage than buying alone. Still, check your employer’s plan details carefully. Sometimes, individual plans fit your needs better.

Consider your income, health, and budget before deciding. Understanding options helps you pick the best coverage. Stay informed to protect your health and finances.