Wondering if you can get premium tax credits when your wife’s health plan already offers coverage? It’s a common question that can feel confusing.

You want to save money on health insurance, but the rules around premium tax credits can be tricky—especially when a spouse’s plan is involved. You’ll discover exactly when you qualify for these credits and when you don’t. By understanding the key details, you can make smarter decisions about your health coverage and potentially keep more money in your pocket.

Keep reading to find out how your wife’s plan might affect your eligibility for premium tax credits.

Premium Tax Credits Basics

Understanding premium tax credits is important when deciding on health insurance options. These credits help lower the cost of health coverage for many people. Knowing the basics can guide you in making smart choices about your insurance.

Premium tax credits are tied to income and the type of health plan chosen. They help reduce monthly insurance payments, making coverage more affordable. Let’s explore what premium tax credits are and how they work.

What Are Premium Tax Credits

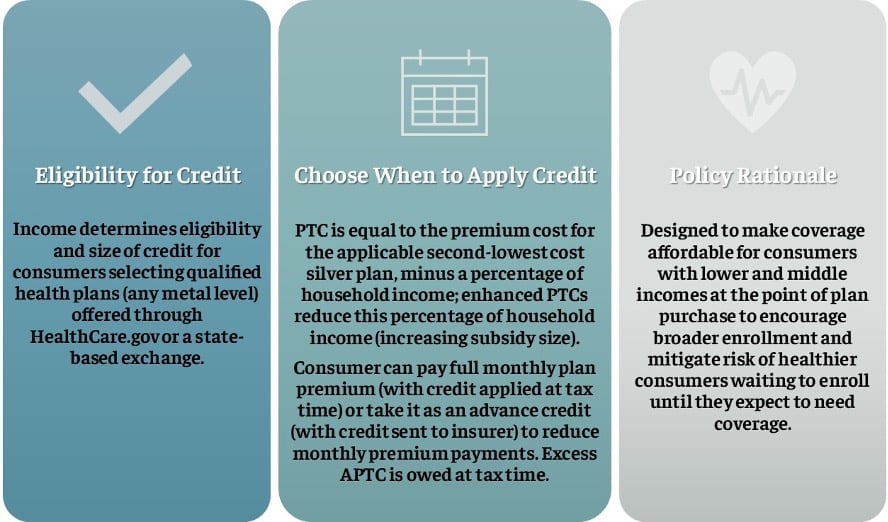

Premium tax credits are government funds to lower insurance costs. They are part of the Affordable Care Act (ACA). The credit reduces the price of monthly health insurance premiums. People with moderate incomes often qualify for these credits.

The credit applies only to plans bought through the Health Insurance Marketplace. It helps make private health insurance affordable for many families. The amount depends on your income and family size.

How Premium Tax Credits Work

Premium tax credits lower the monthly cost of Marketplace health plans. You estimate your income when you apply for coverage. The government then calculates how much help you get. This credit can be paid directly to your insurer.

If your income changes during the year, your credit amount may change too. You can get the credit in advance or claim it on your tax return. This flexibility helps you manage your insurance costs better.

Eligibility Factors

Understanding eligibility factors is key to knowing if you can get premium tax credits. These credits help lower health insurance costs. Several rules decide who qualifies for this financial help. The source of your health insurance, like your spouse’s plan, also matters.

Below are important eligibility factors to consider. They affect whether you can claim premium tax credits.

Income Requirements

Your household income must fall within certain limits. Usually, it should be between 100% and 400% of the federal poverty level. Income is based on your modified adjusted gross income (MAGI). If your income is too high, you cannot get these credits.

Filing Status Impact

How you file your taxes affects eligibility. Married couples who file jointly can qualify. Those who file separately often do not, except for special cases. Exceptions include victims of domestic abuse or certain hardships.

Citizenship And Residency

To qualify, you must be a U.S. citizen or lawfully present resident. Non-citizens without legal status cannot receive premium tax credits. This rule applies to everyone included in your tax return.

Dependents And Claiming Status

If someone else claims you as a dependent, you cannot get the credit. Dependents must meet specific IRS rules to qualify for these benefits. Your claim status directly influences your eligibility for premium tax credits.

Spouse’s Health Insurance Plan

Understanding your spouse’s health insurance plan is key when considering premium tax credits. The rules about employer-sponsored coverage, dependent coverage, and disqualifications can affect your eligibility. Knowing how these factors work helps you make informed decisions about your health coverage options.

Employer-sponsored Coverage Rules

Employer-sponsored plans must meet certain standards to impact your premium tax credit. The plan should be affordable, costing no more than a set percentage of your income. It must also provide minimum value, covering essential health benefits. If your spouse’s employer plan meets these rules, you might not qualify for the tax credit.

Spouse Plan Coverage For Dependents

Your spouse’s plan may cover dependents like children or you. If the plan covers you as a dependent, this can affect your tax credit eligibility. Coverage for dependents often counts as employer-sponsored coverage. This coverage can limit your ability to claim premium tax credits on Marketplace plans.

When Spouse Plan Disqualifies You

You cannot get premium tax credits if your spouse’s plan is affordable and meets minimum value. Also, if you have access to the plan but choose not to enroll, you may lose eligibility. The IRS checks if employer coverage is available to you through your spouse. This can disqualify you from receiving tax credits on the Marketplace.

Credit: npabenefits.com

Marketplace Vs Off-marketplace Plans

Deciding between Marketplace and off-Marketplace plans affects your eligibility for premium tax credits. The Marketplace offers plans that qualify for these credits, which lower your monthly costs. Off-Marketplace plans do not provide this benefit. Understanding the differences helps you choose the right option, especially if your spouse’s plan covers you.

Buying Through The Marketplace

Marketplace plans are sold on official government sites like HealthCare.gov. These plans meet rules for coverage and cost. You can apply for premium tax credits when buying here. The credits depend on your income and household size. Buying through the Marketplace also allows you to compare many plans side by side. It is easier to find affordable options that fit your needs.

Off-marketplace Insurance Limitations

Off-Marketplace plans come directly from insurance companies or brokers. These plans often do not meet the requirements for premium tax credits. If you buy off-Marketplace, you must pay full price without any credit help. Also, these plans may have fewer consumer protections. You might face higher costs and less coverage choice. Off-Marketplace plans can limit your ability to change coverage during open enrollment.

Exceptions And Special Cases

Premium tax credits help many people afford health insurance. Usually, having a spouse’s health plan means you cannot get these credits. Yet, some exceptions and special cases allow you to qualify despite your wife’s coverage. These exceptions address unique situations and protect those in need.

Domestic Abuse Exception

Survivors of domestic abuse can claim premium tax credits separately. The IRS allows filing as “Married Filing Separately” without losing the credit. This exception helps protect privacy and safety. You do not have to share your income or health plan details with your spouse. To qualify, you must meet certain criteria and provide proof of abuse.

No Employer Coverage Available

If your wife’s employer does not offer health insurance, you might still get tax credits. The key is that you cannot get affordable coverage through her job. The IRS looks at whether the employer’s plan meets cost and coverage rules. When no suitable plan exists, you may apply for premium tax credits on the Marketplace.

Self-employed Health Insurance Deductions

Self-employed individuals have special rules for health insurance costs. You can deduct premiums paid for yourself and family members. This deduction lowers your taxable income and affects your tax credit eligibility. If your wife’s plan is not available to you through her employer, these deductions become important. They can work alongside premium tax credits to reduce health care expenses.

Credit: penncapital-star.com

How To Claim Premium Tax Credits

Claiming premium tax credits can lower your health insurance costs. You may get these credits even if your wife’s plan offers coverage. The process involves applying and reporting correctly. Understanding how to claim these credits helps maximize your savings.

Applying Through The Marketplace

Start by visiting the Health Insurance Marketplace website. Fill out the application with your household income and details. Include information about your wife’s health insurance plan. The Marketplace calculates your eligibility based on this data. You can apply during open enrollment or a special enrollment period.

Choose a Marketplace plan to see if premium tax credits apply. The system shows how much credit you might receive. You can select a plan that fits your budget and needs. Submit your application and keep a copy for your records.

Reporting On Tax Returns

After the year ends, report your income and coverage on your tax return. Use IRS Form 8962 to claim the premium tax credit. This form reconciles the advance payments made during the year. It ensures you get the correct amount of credit or pay back any excess.

Provide accurate income and coverage information to avoid penalties. If your income changes, update your Marketplace application promptly. This helps prevent owing money when you file your taxes. Keep all documents related to your health insurance and credits.

Common Disqualifications

Understanding common disqualifications helps clarify if you can receive premium tax credits. These credits lower health insurance costs for many families. Certain conditions, however, prevent eligibility. Knowing these rules avoids surprises during tax filing and coverage enrollment.

Affordable Employer Coverage

Having access to affordable employer coverage often disqualifies you. The plan must meet specific affordability and minimum value standards. If your wife’s employer plan costs less than 9.12% of your household income, you usually cannot claim credits. This rule ensures tax credits support those without affordable options.

Public Insurance Programs

Enrollment in public insurance programs also affects eligibility. Being covered by Medicare, Medicaid, CHIP, TRICARE, or VA benefits makes you ineligible. The premium tax credit is designed for private Marketplace plans only. Public program coverage means you do not qualify for these credits.

Married Filing Separately

Filing taxes as married filing separately generally disqualifies you from premium tax credits. Exceptions exist, such as cases of domestic abuse or spousal abandonment. This filing status usually blocks eligibility to prevent misuse. Couples often file jointly to maintain access to tax credits.

Credit: bipartisanpolicy.org

Tips For Maximizing Tax Credits

Maximizing premium tax credits can reduce your health insurance costs significantly. Understanding how your spouse’s health plan affects your eligibility is key. Careful planning and coordination help you get the best financial support available.

Use these tips to make the most of your premium tax credits while managing health coverage within your household.

Coordinating Spouse Coverage

Compare both health plans carefully. See which one offers better benefits for your family’s needs. Check if your wife’s plan meets affordability and minimum value standards. If it does, you may not qualify for premium tax credits.

Consider enrolling in the plan that costs less overall. Sometimes, having one spouse on the employer plan and the other on Marketplace coverage offers savings. Coordinate open enrollment periods to avoid gaps in coverage. Keep records of all health insurance documents.

Income Planning Strategies

Your household income affects your premium tax credit amount. Plan your income to stay within eligible limits. Estimate your combined income carefully before applying. Avoid large income changes that could reduce or eliminate credits.

Use tax withholding or estimated tax payments to manage income. Adjust your earnings if possible to qualify for higher credits. Report any income changes to the Marketplace promptly. This helps prevent owing money when you file taxes.

Frequently Asked Questions

What Disqualifies You From The Premium Tax Credit?

You lose premium tax credit eligibility if you have affordable employer coverage, public insurance, or buy off-Marketplace plans. Filing status, citizenship, and dependent claims also matter.

Can I Get Marketplace Insurance If My Spouse Has Insurance?

You can buy Marketplace insurance if your spouse’s plan doesn’t cover you. Premium tax credits usually don’t apply if covered by spouse’s insurance.

Can I Deduct My Wife’s Health Insurance Premiums?

You can deduct your wife’s health insurance premiums if you pay them directly and itemize deductions or qualify for self-employed health insurance deduction. The deduction applies only to premiums you personally pay, not those paid by an employer or reimbursed.

Can I Claim A Tax Deduction On Premium For My Wife?

You can claim a tax deduction on your wife’s premium if you pay it from your pocket. The deduction applies to premiums paid for spouse coverage under Section 80D of the Income Tax Act. Ensure the payment is made by you and keep the receipts for proof.

Conclusion

Spouse’s employer health insurance usually affects your premium tax credit eligibility. If the plan covers you and meets affordability rules, tax credits likely won’t apply. Tax credits only help when no affordable coverage is available through an employer. Check your household income and plan details carefully.

Marketplace plans without employer offers might qualify for credits. Always review your options before deciding. This helps avoid unexpected costs and ensures proper coverage. Understanding these rules saves money and keeps you covered.