Have you ever wondered if your car insurance will help pay for a cracked or broken windshield? Knowing whether your policy covers windshield replacement can save you time, money, and stress when unexpected damage happens.

You might think all car insurance plans handle this the same way, but that’s not true. Some cover it fully, others only partially, and some not at all. You’ll learn exactly how to check your coverage, what types of insurance apply, and when it makes sense to file a claim.

Keep reading to make sure you’re prepared before that next chip or crack appears on your windshield.

Insurance Coverage Types

Understanding the types of insurance coverage helps you know if your windshield replacement is covered. Different policies treat glass damage in various ways. Checking your coverage type saves time and confusion.

Comprehensive Coverage

Comprehensive coverage often includes windshield damage. It protects against non-collision events like theft, vandalism, or weather. This coverage usually pays for glass repair or replacement. Some policies have a separate deductible for glass claims.

Collision Coverage

Collision coverage pays for damage caused by an accident with another vehicle or object. It may cover windshield replacement if the glass breaks during a collision. This coverage often has a deductible that applies to the claim.

Glass-specific Coverage

Glass-specific coverage focuses only on glass repair or replacement. It sometimes comes as an add-on or separate policy. This type often has no deductible or a low one, making repairs easier and cheaper. Check if your insurer offers this option.

Credit: www.progressive.com

When To File A Claim

Knowing when to file a claim for windshield replacement can save you money and stress. The decision depends on several factors, including the severity of the damage, your insurance deductible, and state laws. Understanding these points helps you make a smart choice about filing a claim.

Damage Severity

Assess the damage to your windshield carefully. Small chips or cracks under a few inches might not need a full replacement. These often repair easily and cost less. Large cracks, shattered glass, or damage that affects your view need immediate replacement. Driving with severe damage is unsafe and may be illegal.

Cost Vs Deductible

Compare the repair or replacement cost to your insurance deductible. Your deductible is the amount you pay before insurance covers the rest. If repair costs are less than or close to your deductible, paying out-of-pocket may be better. For higher costs, filing a claim can save money. Check if your policy has a separate deductible for glass claims.

State Glass Laws

Some states have special rules about windshield coverage. These laws may require insurers to pay for glass repair or replacement without charging a deductible. Known as “free glass” laws, they protect drivers from extra costs. Check your state’s regulations to see if you qualify for such benefits. This can affect your decision to file a claim.

When To Pay Out-of-pocket

Deciding to pay out-of-pocket for windshield replacement depends on several factors. Sometimes handling minor damage yourself can save money and avoid insurance hassles. Understanding when to cover costs personally helps maintain your insurance benefits and rates. Below are key points to consider.

Minor Damage

Small chips or cracks often cost less than the deductible. Repairing these without insurance can be cheaper. Quick fixes prevent damage from spreading and keep your windshield safe. Many auto shops offer affordable repair services for minor issues.

Avoiding Rate Increases

Filing a claim might raise your insurance premiums. Insurance companies may view claims as risks. Paying out-of-pocket avoids this risk and keeps your rates steady. For small repairs, this approach can be more cost-effective over time.

Multiple Claims Impact

Making several claims in a short time may affect your record. Multiple claims can lead to higher premiums or policy cancellation. Handling small damages yourself reduces claim frequency. This protects your insurance standing and future costs.

Credit: aadvanceautoglass.com

Checking Your Policy

Checking your car insurance policy is the first step to know if windshield replacement is covered. Your policy details explain what damages are included. Understanding these details helps avoid surprises during a claim. Read your policy carefully to find specific information about glass coverage.

Deductible Details

The deductible is the amount you pay before insurance helps. Check if your policy has a separate deductible for glass damage. Some policies offer zero deductible for windshield repairs. Knowing this saves money and helps decide whether to file a claim.

Repair Vs Replacement Coverage

Insurance may cover repair but not full replacement. Small chips or cracks might be fixed without replacing the whole windshield. Larger damage often requires replacement and may have different coverage rules. Review your policy to see which is covered and under what conditions.

Policy Exceptions

Some policies exclude certain types of glass damage. Damage caused by accidents may be covered, but wear and tear or vandalism might not. Weather-related damage may also have special rules. Look for these exceptions in your policy to understand coverage limits.

Estimating Repair Costs

Estimating the cost of windshield repair or replacement helps you decide on insurance claims. Knowing the repair expenses upfront avoids surprises and helps you budget. This step also clarifies whether your insurance coverage makes sense for the damage.

Getting Multiple Quotes

Request price estimates from several auto glass shops. Different shops charge different rates for the same service. Getting multiple quotes gives you a clear range of costs. This helps you spot any unusually high or low prices. It also lets you compare the quality of service offered.

Repair Vs Replacement Costs

Small chips often cost less to repair than full replacements. Repairs usually take less time and use fewer materials. Large cracks or shattered windshields require complete replacement. Replacement costs include new glass and labor charges. Understanding these differences helps you know what to expect.

Comparing Insurance Payouts

Check how much your insurance will pay for glass damage. Your payout usually equals the repair or replacement cost minus your deductible. Compare this amount to the quotes you received. If the payout is less than the cost, you may pay out-of-pocket. Knowing this prevents unexpected expenses after the claim.

State-specific Rules

Car insurance coverage for windshield replacement varies widely by state. Each state has its own rules that affect whether your insurance pays for repairs or replacement. Understanding these state-specific regulations helps you know your rights and options. Some states offer more protection for drivers, while others have stricter conditions. Below are key state-level rules that impact windshield coverage.

No Deductible States

Several states require insurance companies to cover windshield repair or replacement without charging a deductible. This means you pay nothing out of pocket if your windshield is damaged. States like Florida, Texas, and California have laws that protect consumers with zero deductible glass coverage. These rules encourage timely repairs to keep drivers safe and reduce insurance claims.

Free Windshield Replacement Laws

Some states go beyond no deductible rules and mandate free windshield replacement. These laws ensure full coverage for glass damage under comprehensive insurance. Drivers in these states do not bear any cost for fixing or replacing a broken windshield. The goal is to promote safety by removing financial barriers for quick windshield service.

Local Insurance Regulations

Insurance regulations vary locally within states as well. Some states allow insurers to set their own terms for glass coverage. Others require specific disclosures about coverage details in the policy. Local rules may affect how claims are processed and what types of damage qualify for replacement. Checking your state’s insurance department website helps clarify these local rules.

Impact On Insurance Premiums

Understanding how windshield replacement affects your insurance premiums is important. Some repairs may not impact your rates much. Others could lead to higher costs. Knowing these details helps you decide whether to file a claim or pay out-of-pocket.

Insurance companies view windshield claims differently than other types of damage. The impact on premiums depends on how often you claim and your insurer’s policies. Let’s explore how claims affect your rates and what to expect over time.

Claims And Rate Changes

Filing a claim for windshield replacement might not always increase your premium. Many insurers treat glass damage separately. Small or one-time claims often cause little to no rate change. Large or repeated claims can trigger premium increases. Your insurer may also consider your overall claim history.

Frequency Of Claims

Making frequent claims for windshield damage can raise flags. Insurance companies may see you as a higher risk. This perception can lead to increased premiums or even policy non-renewal. Limiting claims to major repairs helps keep rates stable. Minor chips or cracks might be better repaired without insurance.

Long-term Effects

Repeated claims over several years may affect your insurance costs. Premiums could rise even if individual claims do not. Some insurers offer glass coverage with no deductible to avoid frequent claims. Checking your policy details can reveal long-term benefits or drawbacks. Staying informed helps you manage costs better.

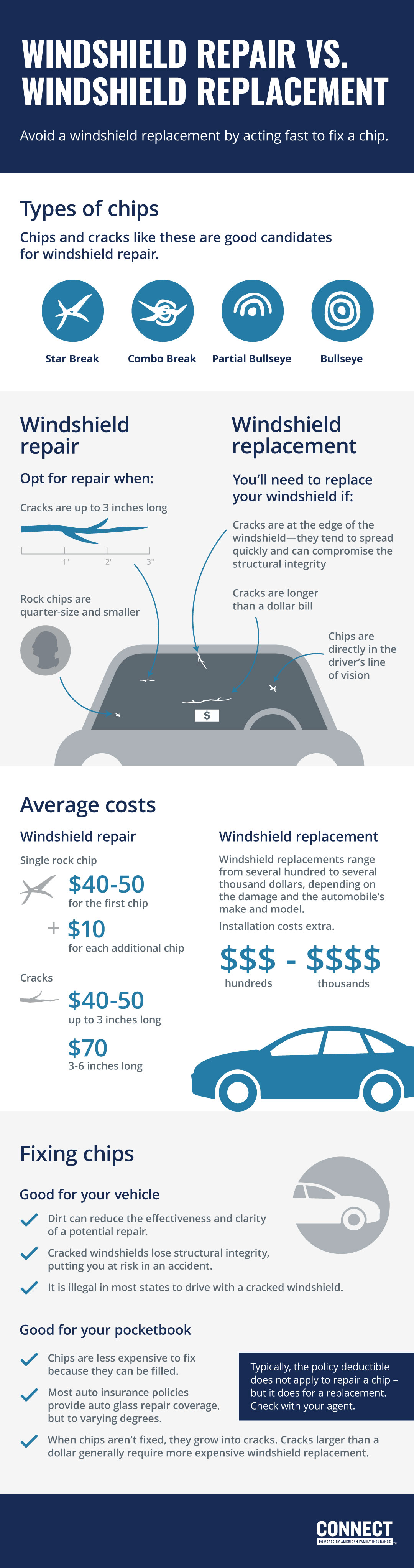

Credit: www.connectbyamfam.com

Tips For Smooth Claims

Filing a claim for windshield replacement can feel confusing. Following clear steps helps the process go smoothly. Prepare well and avoid delays. Understand what your insurer needs before you start. This lowers stress and speeds up your claim.

Documentation Needed

Keep all documents related to the damage. Take clear photos of the cracked or broken windshield. Get a written estimate from the repair shop. Keep your insurance policy and claim forms ready. These papers help prove your case quickly.

Choosing Repair Shops

Pick a repair shop approved by your insurance company. Approved shops often handle claims faster. They know the insurer’s rules and paperwork. Check shop reviews and reputation before deciding. A reliable shop ensures quality work and smooth communication.

Timing Your Claim

File your claim as soon as possible after the damage. Waiting too long may cause your claim to be denied. Early reporting shows responsibility and urgency. Schedule the repair quickly to avoid further damage. Prompt action protects your safety and wallet.

Frequently Asked Questions

How To Know If Windshield Replacement Is Covered By Insurance?

Check your insurance policy for comprehensive coverage, which usually covers windshield replacement. Contact your insurer to confirm specific terms and deductible details. Some states mandate no-deductible glass coverage. Compare repair costs with your deductible to decide on filing a claim.

Is It Worth Filing An Insurance Claim For A Cracked Windshield?

Filing a claim is worth it if repair costs exceed your deductible or damage is severe. Check your policy first.

Does Ga Have Free Windshield Replacement?

Georgia does not offer free windshield replacement universally. Coverage depends on your insurance policy and deductible. Some policies cover full replacement with comprehensive coverage, while others require payment. Check your insurance details to confirm if free windshield replacement applies in your case.

Does Car Insurance Cover Windshield Replacement For Free?

Car insurance covers windshield replacement only with comprehensive coverage. Some policies offer free replacement with zero deductible. Coverage varies by insurer and state laws. Check your policy details to confirm. Filing a claim depends on repair costs versus your deductible amount.

Conclusion

Knowing if your car insurance covers windshield replacement helps you save money. Check your policy details carefully for glass coverage and deductibles. Comprehensive coverage usually includes windshield repairs or replacements. Small chips might be fixed without filing a claim. Large cracks often require replacement and may need a claim.

Compare repair costs with your deductible before deciding. Calling local auto glass shops for quotes can guide your choice. Stay informed to protect your vehicle and avoid unexpected expenses.