Table of Contents

- Why Insurance Matters for Young Families

- How to Calculate Life Insurance Needs for Your Family

- Term vs Whole Life Insurance for Families: Which Is Right for You

- Essential Insurance Checklist for New Parents

- Key Insurance Tips for Young Families on a Budget

- Disability Insurance and Income Protection

- When to Review and Update Your Family Insurance Plan

- Conclusion

Insurance Tips for Young Families: Essential Coverage Guide

Last Updated: June 27, 2026

Why Insurance Matters for Young Families

One unexpected illness, accident, or tragedy can wipe out years of savings. Insurance is the safety net that keeps your family’s dreams intact when life doesn’t go as planned. A single hospitalization without adequate health insurance can cost $35,000 or more. Losing a primary earner without life insurance can force a family into decades of financial hardship.

Families who plan early pay less and sleep better at night. Below, we’ll walk you through which insurance types matter most, how to calculate what you actually need, and specific strategies to protect your family without breaking the budget.

How to Calculate Life Insurance Needs for Your Family

Getting the right life insurance amount is crucial. Two proven methods exist, and most families benefit from using both as a cross-check.

Income Replacement Method

The income replacement method starts with a simple question: how much annual income would your family lose if you died tomorrow?

Take your current annual salary and multiply it by the number of years your family would need that income. Most financial advisors suggest 10-15 years for families with young children, depending on your spouse’s earning potential and when your kids will be financially independent.

Example: If you earn $60,000 annually and want to replace 15 years of income, you’d need $900,000 in life insurance. This amount, invested conservatively, would generate roughly your current salary through investment returns, allowing your family to maintain their lifestyle while your spouse works or retrains.

Most families underestimate how long they’ll need income replacement. If your spouse doesn’t currently work, add extra years to account for the time needed to re-enter the workforce or develop new skills.

Debt and Expense Method

The debt and expense method accounts for everything your family would owe or need to cover if you died.

Start by listing:

- Mortgage balance (or rent for 5-10 years)

- Car loans

- Credit card debt

- Student loans

- Funeral expenses ($8,000-$15,000 average)

- College funding for children (if desired)

- Emergency fund (6-12 months of expenses)

Add these together. This number represents the “floor” of coverage you need. For example, a family with a $250,000 mortgage, $15,000 in car debt, $100,000 in student loans, and $50,000 in funeral and final expenses would need at least $415,000 in life insurance just to cover these obligations.

The strongest approach combines both methods. If your income replacement calculation suggests $900,000 and your debt/expense calculation suggests $615,000, you’d likely want coverage in the $750,000-$900,000 range.

Life insurance proceeds are typically tax-free to your beneficiaries, but income from investing those proceeds is taxable. A financial advisor can help you model realistic after-tax returns on your insurance payout.

Term vs Whole Life Insurance for Families: Which Is Right for You

Understanding the distinction between term and whole life is the foundation of smart insurance decisions. The wrong choice costs you thousands over your lifetime.

Term Life Insurance: Advantages and Affordability

Term life insurance covers you for a set period (typically 10, 20, or 30 years) and provides a death benefit if you die during that term.

The advantages for young families are compelling:

- Affordability: A 30-year term policy for a healthy 35-year-old might cost $40-$60 monthly for $500,000 in coverage. Whole life for the same amount costs $300-$400 monthly.

- Simplicity: You know exactly what you’re paying and what your family gets.

- Alignment with needs: A 20-year term covers your family until your kids are independent and your retirement savings have grown.

- Flexibility: If your situation changes, you’re not locked into a permanent policy.

The tradeoff is that term insurance expires. If you outlive your term, you have no coverage and no cash value. However, this is actually fine for most young families. Your goal is to protect your family during the years they depend on your income. By the time your term expires, you should have built enough savings that life insurance is less critical.

Whole Life Insurance: Permanence and Cash Value

Whole life insurance covers you for your entire life and builds cash value, a savings component that grows tax-deferred.

For young families, whole life has limited appeal:

- Cost: The monthly premium is 5-10 times higher than term insurance for equivalent death benefits.

- Complexity: You’re mixing insurance with investment, and returns are typically modest (3-5% annually).

- Inflexibility: You’re locked into expensive premiums even if your financial situation improves.

Whole life makes sense for high-net-worth families who want permanent coverage and have maxed out other retirement savings vehicles. For young families building wealth, term insurance lets you allocate that premium difference to retirement accounts, college savings, or emergency funds.

A common hybrid approach: buy a 30-year term policy for primary coverage, and if you want permanent coverage for final expenses, add a small whole life policy ($50,000-$100,000).

| Insurance Type | Monthly Cost (30-year, age 35) | Death Benefit | Cash Value | Best For |

|---|---|---|---|---|

| Term (20-year) | $40-$60 | $500,000 | None | Young families with kids |

| Term (30-year) | $60-$90 | $500,000 | None | Families wanting longer coverage |

| Whole Life | $300-$400 | $500,000 | Yes, grows slowly | High-net-worth individuals only |

Essential Insurance Checklist for New Parents

Becoming a parent changes your insurance needs overnight. You’re protecting the people who depend on you.

Life Insurance Coverage Amounts

New parents should have at least 10-15 times their annual income in term life insurance. If you earn $50,000, that’s $500,000-$750,000 minimum.

Both spouses need coverage, even if one doesn’t work outside the home. A stay-at-home parent provides childcare, household management, and education, services that would cost $15,000-$25,000 annually if outsourced. That parent should have $250,000-$500,000 in coverage.

Review your coverage annually. As your income grows, increase your death benefit. As your kids age and your savings grow, you can eventually reduce coverage.

Disability and Health Insurance Priorities

A 35-year-old worker has a 1-in-4 chance of experiencing a disability lasting 90 days or more before retirement age. Yet most young families have no disability insurance.

If you become disabled and can’t work, your family loses income immediately. Disability insurance replaces 50-70% of your income, typically for 2-5 years, giving you time to recover or retrain.

Health insurance is non-negotiable. Medical debt is the leading cause of bankruptcy in America. Ensure your health plan includes preventive care coverage, reasonable deductibles ($1,500-$3,000 for families), and out-of-pocket maximums ($7,000-$10,000).

Life insurance, disability insurance, and health insurance form the foundation of family financial protection. Without all three, you’re leaving your family exposed to catastrophic financial events.

Homeowners and Umbrella Liability Coverage

Homeowners insurance protects your home and includes liability coverage if someone is injured on your property and sues you. Standard policies include $100,000-$300,000 in liability coverage, which isn’t enough for growing families.

Umbrella liability insurance sits “on top” of your homeowners and auto insurance, providing an additional $1 million in liability coverage for about $150-$300 annually. If your home is worth $400,000 and your net worth is growing, umbrella insurance is essential.

Renters should also consider umbrella insurance if they have meaningful assets. Renters insurance itself is cheap ($10-$20 monthly) and covers your belongings plus $100,000 in liability.

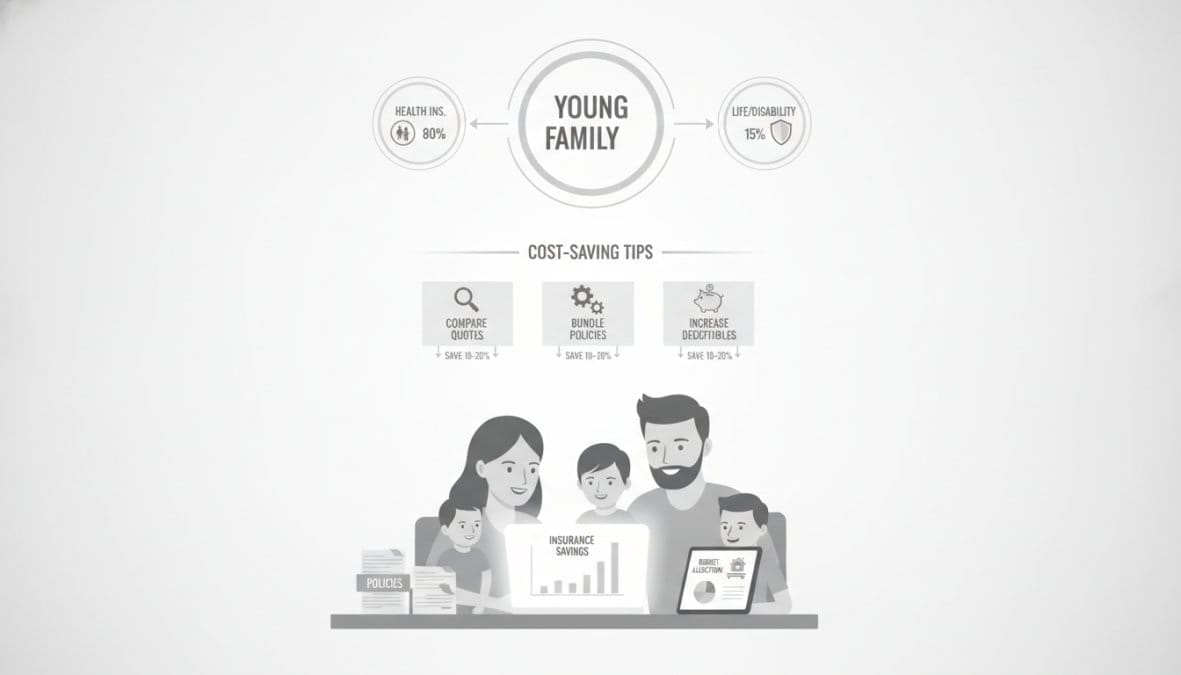

Key Insurance Tips for Young Families on a Budget

Young families need comprehensive protection on a tight budget. These strategies help you get the coverage you need without overpaying.

Strategies to Reduce Premiums Without Sacrificing Coverage

Bundle policies. Buying auto, home, and umbrella insurance from the same company typically saves 10-25% compared to separate policies.

Increase deductibles strategically. Raising your homeowners deductible from $500 to $1,000 saves about 5-10% on premiums. This works only if you have an emergency fund covering the deductible.

Shop annually. Your rate today might be 20-30% higher than competitors’ rates for identical coverage. Spending one hour annually getting quotes can save hundreds.

Improve your health profile. Quitting smoking, maintaining a healthy weight, and managing chronic conditions improve rates. Some insurers offer discounts for gym memberships or health tracking apps.

Ask about discounts. Many insurers offer discounts for defensive driving courses (3-10%), home security systems (5-15%), annual payment (2-5%), and customer loyalty (5-10%).

Buy term insurance young. Life insurance premiums are based heavily on age and health at purchase. A 30-year-old buying a 30-year term policy locks in rates for three decades. A 40-year-old buying the same policy pays significantly more.

Common Mistakes Young Families Make With Insurance

Underestimating life insurance needs. Young families often think $250,000 is “enough.” For a family with a mortgage and young children, this is dangerously low. Run both calculation methods and err on the side of more coverage.

Skipping disability insurance. Young families assume they’re healthy and won’t need it. But disability is more common than death for working-age adults. If your employer doesn’t offer it, buy individual coverage.

Keeping the same coverage as your life changes. You bought insurance when you had one child and a $200,000 mortgage. Now you have three children and a $400,000 mortgage. Your coverage hasn’t changed, but your needs have. Review annually and adjust.

Choosing coverage based only on price. The cheapest policy isn’t always the best. Check financial stability ratings (A.M. Best, Standard & Poor’s) and read reviews before choosing based on price alone.

Disability Insurance and Income Protection

Disability insurance is the forgotten pillar of family protection. If you become unable to work due to illness or injury, your family loses income immediately. Savings deplete quickly while mortgage payments and daily expenses continue.

Disability insurance replaces a portion of your income, typically 50-70%, while you recover or retrain. This bridge income allows your family to maintain stability without depleting savings.

Short-term disability typically covers 3-6 months of disability. Many employers provide this automatically. Long-term disability covers disabilities lasting longer than 6 months, up to age 65. This is where most young families have gaps.

If your employer offers long-term disability, enroll. If not, buy individual coverage. For a young, healthy professional, long-term disability insurance costs $30-$60 monthly for coverage replacing $3,000-$4,000 monthly income.

The waiting period (how long after disability starts before benefits begin) affects the premium. A 90-day waiting period is cheaper than a 30-day period, but only if you have 3 months of emergency savings.

Some professions, particularly high-income earners like doctors and lawyers, should consider “own-occupation” disability coverage, which pays benefits if you can’t perform your specific job, even if you can work in another field. Own-occupation costs more but provides crucial protection for specialized careers.

When to Review and Update Your Family Insurance Plan

Insurance isn’t a “set it and forget it” decision. Review your plan at least annually, and immediately after major life events.

After having a child: Your life insurance needs increase substantially. Increase your death benefit and add disability insurance if you don’t have it.

After a promotion or raise: Your income has increased, so your coverage should too. Update your life insurance to reflect your new earnings.

After purchasing a home: Ensure your homeowners insurance covers the full replacement cost of your home. Add umbrella liability coverage if you don’t have it.

After significant life changes: Divorce, remarriage, inheritance, or major health changes all affect your insurance needs. Run your calculations again and adjust beneficiaries on life insurance and retirement accounts.

Every 3-5 years even without major changes: Insurance rates and available products change. A policy that made sense five years ago might be outdated. Shop around and compare.

Protecting your young family doesn’t require perfect knowledge or a large budget, it requires intentional decisions made early. Start by calculating your actual insurance needs, choose appropriate coverage amounts, and review annually as your family grows. Your future self will thank you for the protection you put in place today.

Frequently Asked Questions

What types of insurance do young families need most?

Young families should prioritize life insurance, health insurance, disability insurance, and homeowners or renters insurance. Life insurance protects dependents if a breadwinner dies; disability insurance replaces income if you can’t work; health insurance covers medical costs; and property insurance protects your home and belongings. These four form the foundation of a young family’s financial protection strategy.

How much life insurance should a young family have?

Most financial experts recommend 10-12 times your annual income in life insurance coverage. For a family earning $50,000 annually, this means $500,000-$600,000 in coverage. Use the income replacement method to calculate needs: multiply your annual income by the years until retirement, then add outstanding debts and future education costs. Term life insurance is typically the most affordable option for young families.

How can young families save money on insurance premiums?

Bundle policies with one insurer for multi-policy discounts. Increase your deductible to lower monthly costs. Maintain good health and avoid risky behaviors to qualify for better rates. Shop around and compare quotes from multiple providers. Consider term life insurance over whole life for affordability. Ask about discounts for safety features, good driving records, or completing wellness programs.

Is disability insurance necessary for young parents?

Yes, disability insurance is critical for young parents. If you can’t work due to illness or injury, your family loses income when you need it most. Long-term disability insurance replaces 50-70% of your income during recovery. Many employers offer group disability coverage at low cost. If not available through work, individual disability policies are affordable for young, healthy individuals and should be part of your insurance checklist for new parents.