Planning a pregnancy in 2026 means making some important decisions—especially when it comes to your health insurance. You might be wondering: Should you choose a PPO plan or go with a High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA)?

Each option has its strengths and challenges, and the right choice can have a big impact on your out-of-pocket costs, access to doctors, and peace of mind during this exciting time. You’ll discover the key differences between PPO and HDHP with HSA plans, and get practical advice to help you pick the best coverage for your growing family.

Keep reading to make sure your insurance supports your pregnancy journey without surprises or stress.

Ppo Basics

Choosing the right health plan is important when planning for pregnancy in 2026. PPO plans are popular for their flexibility and ease of use. Understanding the basics of PPOs helps you compare them with other options like HDHP with HSA. This section explains how PPO plans work, their costs, coverage, and provider networks.

How Ppo Plans Work

PPO stands for Preferred Provider Organization. It lets you visit any doctor or specialist without a referral. You get better coverage if you use providers within the PPO network. You can also see out-of-network doctors but pay more out of pocket. PPO plans give you freedom to choose healthcare providers easily.

Ppo Costs And Coverage

PPO plans usually have higher monthly premiums than other plans. They cover a wide range of services including prenatal care, hospital stays, and delivery. You pay copayments or coinsurance for doctor visits and prescriptions. Deductibles vary but are often lower than HDHP plans. PPOs offer balanced costs and good coverage for pregnancy needs.

Provider Networks In Ppo

PPO networks include many doctors, hospitals, and specialists. Using in-network providers keeps your costs lower. You can still visit out-of-network providers but expect higher fees. Networks are usually large, giving you more choices during pregnancy. Checking if your preferred doctors are in-network is important before enrolling.

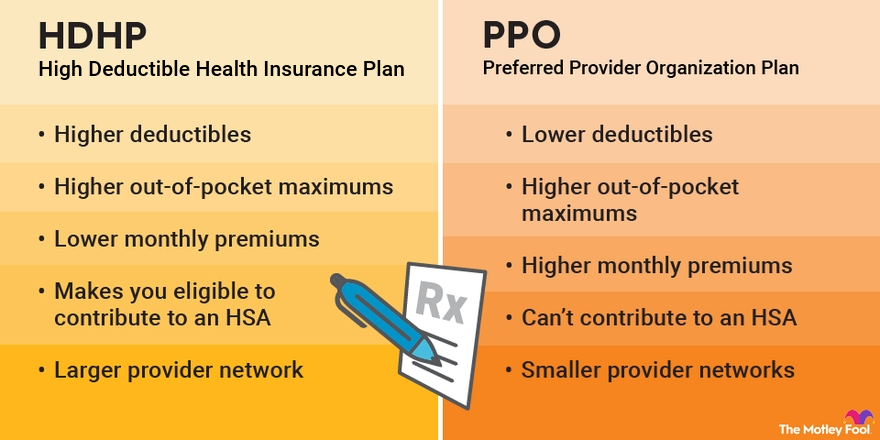

Hdhp And Hsa Basics

Choosing the right health plan is important when planning pregnancy in 2026. Understanding the basics of a High Deductible Health Plan (HDHP) and a Health Savings Account (HSA) can help. These two often come together and offer unique benefits for expectant parents. Knowing how they work will guide you toward better financial and healthcare choices.

How Hdhp Works

An HDHP has higher deductibles than traditional plans. This means you pay more out-of-pocket before insurance starts to cover costs. Monthly premiums for HDHPs tend to be lower. It covers preventive care without requiring you to meet the deductible first. You must meet the deductible before the plan pays for most services. HDHPs can be paired with an HSA for added savings. This setup is useful for families expecting medical expenses.

Benefits Of Hsas

An HSA is a savings account linked to an HDHP. You can deposit money tax-free into this account. These funds pay for qualified medical expenses like doctor visits and prescriptions. The money rolls over each year if unused. HSAs are owned by you, not your employer. This means the account stays with you even if you change jobs. Using an HSA helps manage pregnancy costs more easily. It also builds a medical savings fund for future needs.

Tax Advantages Of Hsa

HSA contributions reduce your taxable income. The money grows tax-free while in the account. Withdrawals for qualified medical expenses are also tax-free. This triple tax benefit is rare in other accounts. You can contribute up to a set limit each year. Contributions can come from you, your employer, or both. Using an HSA during pregnancy can lower overall healthcare costs. It offers a tax-efficient way to save and pay for care.

Pregnancy Costs With Ppo

Pregnancy costs with a PPO plan vary but generally offer broad coverage. PPO plans allow access to a wide network of doctors and hospitals. This flexibility suits many expecting parents. Understanding prenatal care, hospital fees, and out-of-pocket costs helps in choosing the right plan for 2026 pregnancy planning.

Prenatal Care Coverage

PPO plans usually cover prenatal visits, tests, and screenings. Regular check-ups are essential for a healthy pregnancy. Most plans include ultrasounds, blood tests, and genetic screenings. Coverage often begins as soon as pregnancy is confirmed. Choosing a PPO means you can visit specialists without referrals. This ease supports better prenatal care management.

Hospital And Delivery Costs

Delivery costs under a PPO can be high but predictable. PPO plans cover hospital stays, labor, and delivery fees. Both vaginal and C-section deliveries fall under coverage. You can choose your preferred hospital and doctor. Emergency care and newborn care also receive coverage. Some plans offer maternity bundles to reduce surprise bills.

Out-of-pocket Expenses

PPO plans have deductibles, copayments, and coinsurance. These costs vary depending on your plan details. Monthly premiums tend to be higher for PPOs. Out-of-pocket maximums cap your yearly spending. After reaching this limit, the plan pays 100% of covered services. Planning your budget with these costs in mind is wise.

Pregnancy Costs With Hdhp + Hsa

Pregnancy costs with a High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) can be complex. Expectant parents face high upfront expenses before insurance starts to pay. Understanding these costs helps in planning and managing your budget effectively. The HDHP often has lower monthly premiums but higher deductibles, which can affect maternity care costs. Using an HSA can ease the financial burden by covering some out-of-pocket expenses with tax-free funds.

Coverage Limitations For Maternity

Many HDHPs have specific rules about maternity coverage. Some exclude pregnancy-related care from the deductible. This means you might pay full price for prenatal visits and tests until you reach the deductible. Not all HDHPs cover childbirth the same way. It is important to check if labor and delivery are included in the plan. Coverage limits can lead to high costs during pregnancy.

Managing High Deductibles

High deductibles mean you pay more before insurance helps. Pregnancy can quickly hit these limits due to frequent doctor visits and hospital stays. Planning for these costs is crucial. Track your medical expenses carefully. Budget extra funds to cover prenatal care, ultrasounds, and labor. Early planning reduces stress during pregnancy and helps avoid surprises.

Using Hsa Funds Effectively

An HSA lets you save money tax-free for medical costs. You can use HSA funds to pay for doctor visits, prescriptions, and hospital bills. This helps reduce your out-of-pocket spending. Contribute to your HSA regularly, especially before pregnancy. Save as much as allowed to cover upcoming maternity expenses. Keep receipts to prove your expenses if needed. Using an HSA smartly makes HDHPs more affordable for expectant parents.

Comparing Out-of-pocket Risks

Choosing the right health plan for pregnancy means understanding out-of-pocket risks. These costs can grow fast, especially with complications. Knowing how each plan handles expenses helps avoid surprises. PPO and HDHP with HSA have different ways of managing your spending. We will explore these differences to guide your decision for 2026 pregnancy planning.

Complications And Unexpected Costs

Pregnancy can bring unexpected medical needs. A PPO plan usually has lower deductibles and copays for prenatal visits and tests. This means you pay less upfront for routine care. But if complications arise, PPO plans often cover more services without big price jumps.

HDHP with HSA plans have higher deductibles. You pay most costs yourself until you meet the deductible. This can be tough if unexpected issues happen early. However, you can use HSA funds to pay these expenses tax-free. Still, the initial cost burden may be higher than a PPO.

Maximum Out-of-pocket Considerations

Both PPO and HDHP plans cap your yearly spending. PPO plans often have moderate maximum out-of-pocket limits. This protects you from very high costs but may mean higher monthly premiums.

HDHP plans usually have higher maximum out-of-pocket limits. You might pay more before your insurance covers costs fully. The benefit is lower monthly premiums and the chance to save with an HSA. For pregnancy, reaching this limit can happen quickly.

Evaluating your financial comfort with these limits is key. Consider how much you can afford in monthly premiums versus potential out-of-pocket costs. This helps decide which plan fits your needs best.

Provider Network Access

Choosing the right health plan for pregnancy in 2026 means understanding provider network access. This factor affects which doctors and hospitals you can use. It also impacts your comfort and costs during prenatal care and delivery. Both PPO and HDHP with HSA plans offer different network options. Knowing these differences helps you pick the best plan for your needs.

Finding Preferred Obstetricians

PPO plans usually offer a wide network of obstetricians. You can visit most doctors without referrals. This flexibility helps if you want a specific OB-GYN for your pregnancy. HDHP plans often have narrower networks. You might need to check if your preferred obstetrician accepts the plan. Staying in-network lowers your out-of-pocket costs for prenatal visits and tests.

Hospital Choices And Network Restrictions

Hospitals in PPO networks are often numerous and include top maternity centers. This gives you more options for delivery locations. HDHP networks may limit hospital choices to reduce costs. Choosing an out-of-network hospital in either plan can lead to high bills. Confirming hospital network status early avoids surprises. Consider hospitals known for maternity care quality within the plan’s network.

Employer Contributions And Benefits

Employer contributions and benefits are key factors in choosing between a PPO and an HDHP with an HSA. These can lower your overall costs and provide extra support during pregnancy. Understanding what employers offer helps you pick the best plan for 2026.

Employer Hsa Contributions

Many employers add money to your Health Savings Account (HSA) if you choose an HDHP. This contribution helps cover deductibles and other medical expenses. Employer funds are tax-free and grow over time. They reduce how much you spend out of pocket during pregnancy. Not all employers offer HSA contributions, so check your plan details carefully. PPO plans rarely come with this benefit.

Additional Maternity Benefits

Some employers include extra maternity benefits in their PPO plans. These may cover prenatal visits, ultrasounds, or childbirth classes. They often offer better support for prenatal care without needing to meet a high deductible first. HDHPs might have fewer maternity perks but lower premiums. Employer benefits can also include paid leave or counseling services. These extras can ease the financial and emotional stress of pregnancy.

Credit: www.reddit.com

Eligibility And Enrollment

Choosing the right health plan for pregnancy requires understanding eligibility and enrollment rules. These rules affect your access to benefits and costs. Knowing where and how to enroll helps you find the best coverage for your needs in 2026.

Marketplace Options For Pregnancy

The Health Insurance Marketplace offers various plans, including PPOs and HDHPs with HSAs. You can enroll during the yearly Open Enrollment Period or qualify for a Special Enrollment Period. Pregnancy itself often qualifies you for a Special Enrollment Period.

Marketplace plans cover prenatal care and childbirth as essential benefits. Check each plan’s network to ensure your preferred doctors are included. HDHPs usually have lower premiums but higher deductibles, while PPOs offer more flexibility with providers.

Medicaid And Chip For Low Income

Medicaid and CHIP provide free or low-cost health coverage for pregnant women with low income. Eligibility depends on your state’s rules and household income. Many states extend coverage for pregnancy and up to one year after birth.

Enrollment in Medicaid or CHIP can happen anytime during the year. These programs cover prenatal visits, labor, delivery, and postpartum care. If you qualify, these plans offer strong support without high out-of-pocket costs.

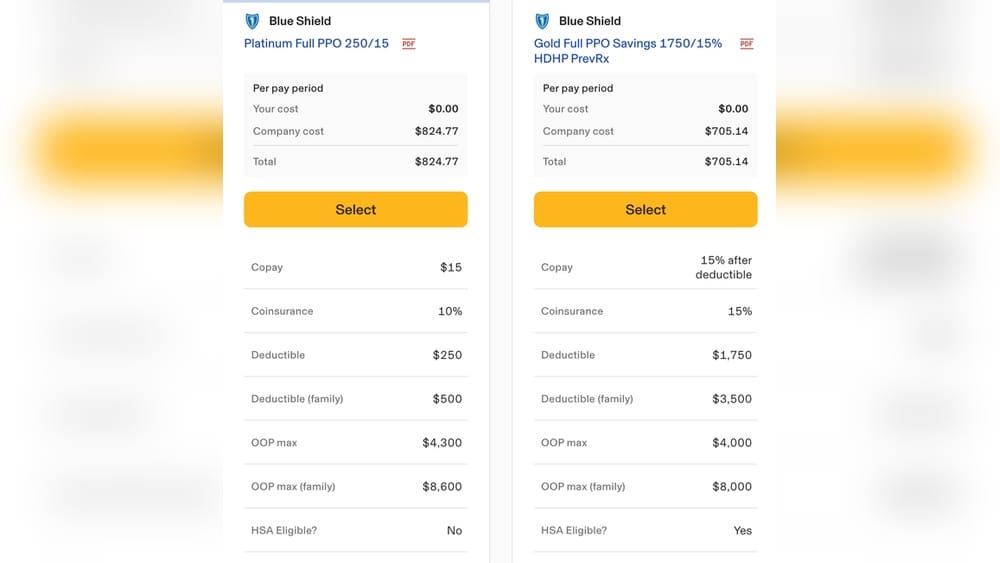

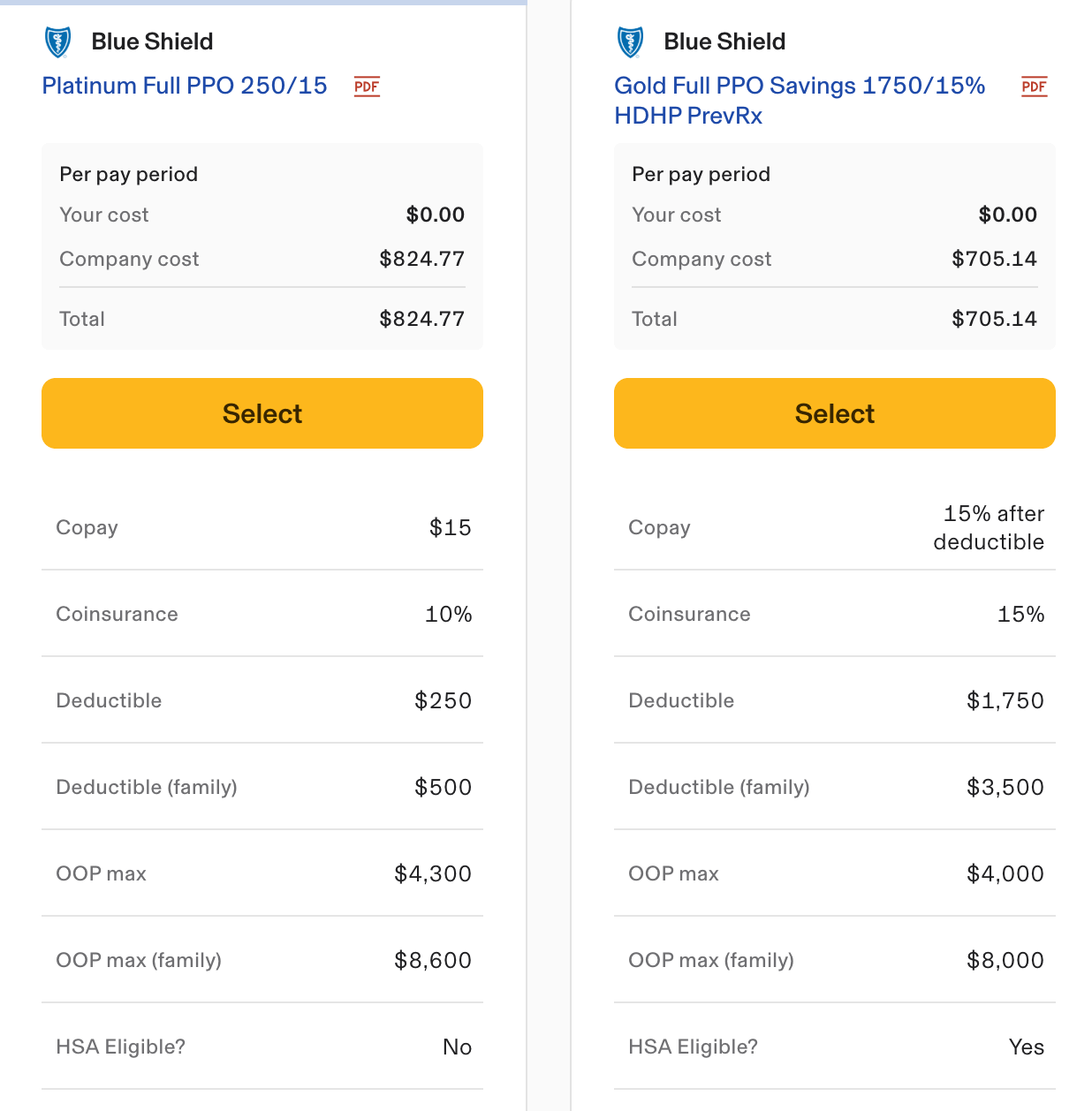

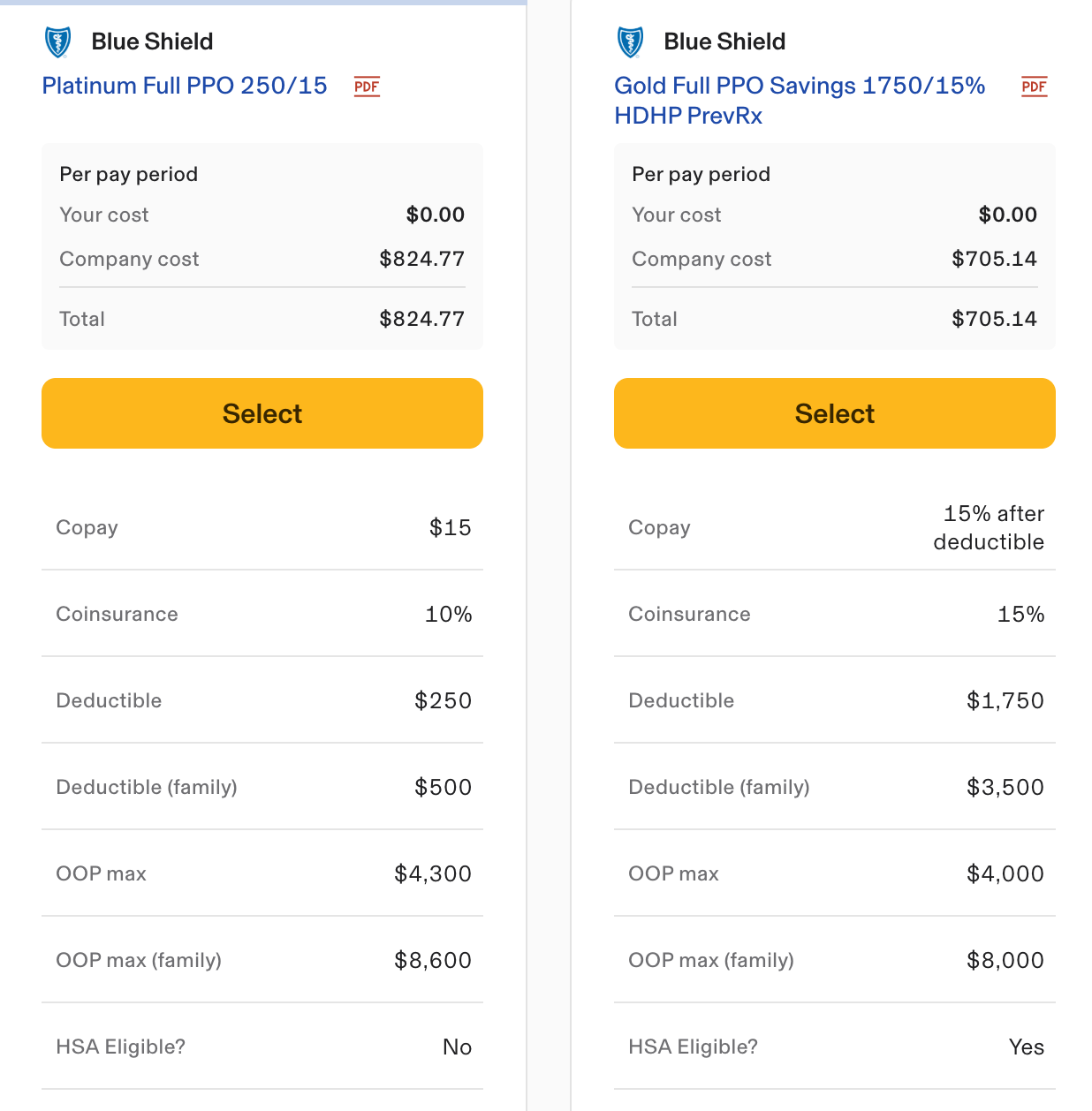

Cost Comparison Examples

Understanding the costs of PPO and HDHP with HSA plans helps expectant parents plan better. Pregnancy involves many medical visits, tests, and sometimes unexpected expenses. Comparing costs can clarify which plan fits your budget and needs for 2026.

Below are examples that show how premiums, deductibles, and total expenses might differ for each plan during pregnancy. This helps you see the financial impact clearly.

Premiums Vs Deductibles

PPO plans usually have higher monthly premiums but lower deductibles. You pay more each month but less when you use services. This can feel safer for pregnancy costs.

HDHP with HSA plans have lower premiums but higher deductibles. You pay less monthly but more out-of-pocket before insurance helps. The HSA saves money tax-free for these costs.

Example: A PPO premium might be $500 monthly with a $1,000 deductible. An HDHP premium could be $300 monthly but a $3,000 deductible. The choice depends on how much care you expect.

Estimated Total Pregnancy Expenses

Pregnancy costs vary but can be $7,000 to $10,000 for routine care and delivery. PPO plans cover most costs after the deductible and copays.

With HDHP, you pay more upfront until reaching the deductible. The HSA can cover these expenses tax-free, easing the burden.

If pregnancy goes smoothly, HDHP may save money due to lower premiums. Complications might push costs higher, making PPO safer for peace of mind.

Credit: www.fool.com

Choosing The Right Plan For 2026

Choosing the right health insurance plan for pregnancy in 2026 requires careful thought. Pregnancy brings many medical needs and costs. A plan that fits your health and budget can ease stress. Understanding your options helps you make the best choice for your growing family.

Two common plans to consider are PPO and HDHP with HSA. Each has benefits and drawbacks. Comparing them based on your needs leads to better decisions for prenatal and delivery care.

Assessing Personal Health Needs

Think about your current health and pregnancy risks. Regular doctor visits and tests are common during pregnancy. Check if your preferred doctors and hospitals accept the plan. Consider any pre-existing conditions or possible pregnancy complications. A plan with lower out-of-pocket costs for frequent care may suit you better.

Financial Planning For Pregnancy

Pregnancy can bring many medical expenses. Calculate your expected costs, including prenatal visits, ultrasounds, and delivery. PPO plans usually have higher premiums but lower copays. HDHP with HSA often has lower premiums but higher deductibles. Use your HSA funds to pay for qualified medical expenses tax-free. This can save money if you plan well.

Tips For Plan Selection

Start by listing your medical needs and budget limits. Compare plans’ coverage for maternity care and prescription drugs. Check how each plan handles emergency and hospital care. Look for plans with clear, simple rules. Read reviews or ask others about their pregnancy experiences with the plans. Choose a plan that offers peace of mind and fits your financial situation.

Credit: www.reddit.com

Frequently Asked Questions

What Type Of Insurance Should I Get If Planning To Get Pregnant?

Choose a health insurance plan that covers maternity care, like Marketplace plans or Medicaid/CHIP. Verify provider networks and benefits. Consider plans with low out-of-pocket costs and no waiting periods for pregnancy-related services.

Should I Get Hsa Or Ppo While Pregnant?

Choose PPO for predictable maternity costs and broader provider access. HSA paired with HDHP offers tax savings but risks high out-of-pocket expenses. Evaluate your budget, coverage needs, and provider network before deciding. Many hit max out-of-pocket during pregnancy regardless of plan.

Is Hdhp Better For Pregnancy?

HDHPs may lead to high out-of-pocket costs during pregnancy, especially with complications. Many exclude maternity coverage or don’t count it toward deductibles. Consider plans with full maternity benefits and lower deductibles for better financial protection during pregnancy.

What Is The Best Insurance Plan For A Pregnant Woman?

The best insurance plan for a pregnant woman covers maternity care with strong provider networks. Medicaid/CHIP suits low-income individuals. Marketplace plans like Kaiser Permanente, Blue Cross Blue Shield, Cigna, and Aetna offer good coverage. Verify provider acceptance and plan details before choosing.

Conclusion

Choosing between a PPO and an HDHP with HSA depends on your needs. PPO plans offer lower out-of-pocket costs and more provider choices. HDHPs have higher deductibles but let you save money tax-free in an HSA. Pregnancy costs can be high, so consider your budget and health risks carefully.

Check if your preferred doctors accept the plan. Think about how much you can contribute to an HSA. Evaluate both plans based on your expected care and finances. This way, you can find the best fit for your 2026 pregnancy journey.