If you’ve ever tried to navigate employer health benefits, you might have heard about the “family glitch.” It’s a confusing rule that can leave families stuck paying high health insurance costs—even when one spouse has coverage through their job. So, how does ICHRA fit into this picture?

Understanding how an Individual Coverage Health Reimbursement Arrangement (ICHRA) works with the family glitch could be the key to unlocking more affordable options for you and your loved ones. Keep reading to discover what the family glitch really means, how ICHRA can help, and what you need to know to make the best health coverage choices for your family.

Credit: www.healthinsurance.org

Family Glitch Basics

The family glitch is a rule in health insurance that can limit coverage options for families. It happens when an employee’s job offers health insurance that is affordable for just the employee. However, the cost to add family members is often high. This makes family members unable to get help to pay for coverage through the health insurance marketplace.

This section explains the basics of the family glitch. It covers how the glitch affects coverage, the rules about employer coverage affordability, and the impact on family premium tax credits.

How The Family Glitch Affects Coverage

The family glitch stops families from getting financial help for health plans. If the employee’s own coverage is affordable, the family cannot get subsidies. This happens even if the cost for family coverage is too high. Many families end up paying full price or going without insurance.

Employer Coverage Affordability Rules

The law says employer coverage is affordable if the employee’s share is under a set percentage of income. This percentage is only checked for the employee’s coverage, not the family plan. This creates a gap where family coverage can be expensive but still counted as affordable. That gap causes the family glitch.

Impact On Family Premium Tax Credits

Because of the family glitch, family members cannot get premium tax credits. These credits help lower the cost of marketplace health plans. Without them, many families face high insurance costs. The family glitch keeps some families from accessing these savings, even if they need help.

What Is An Ichra

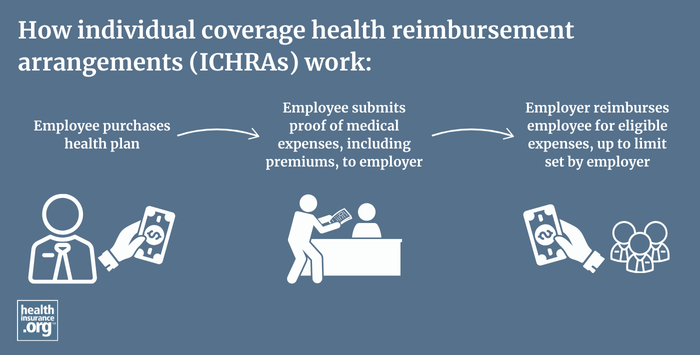

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is a type of health benefit employers offer. It lets employees buy their own health insurance. Employers then reimburse employees for part or all of the premiums. ICHRAs give workers more control over their health plans. They can choose a plan that fits their needs best.

ICHRA is flexible for both small and large companies. Employers set a monthly allowance for employees. Employees pick a health plan that works for them. Then, they send proof of payment to get reimbursed. This approach helps employers manage costs and gives employees choices.

How Ichra Reimbursement Works

Employers decide how much money to give each employee per month. Employees buy individual health insurance plans on the market. They pay for the premiums upfront. Then, employees submit receipts or proof of payment to their employer. The employer reimburses the employees up to the allowance limit. This process is simple and clear for both sides.

Setting Employee Allowances

Employers can set different allowances for different employee groups. For example, full-time workers might get higher allowances. Part-time workers could receive smaller amounts. Employers can also offer different amounts by job role or location. This customization helps control costs and meet employee needs.

Using Ichra For Individual Market Plans

Employees use ICHRA money to buy plans from the individual insurance market. These plans offer many options and different coverage levels. Employees can pick plans that cover their family or just themselves. ICHRA works well with the individual market because it supports flexible choices. This helps employees avoid the limits of traditional group plans.

Ichra And The Family Glitch

The Individual Coverage Health Reimbursement Arrangement (ICHRA) offers a new way for employers to help employees buy health insurance. It lets employees choose their own plans and get reimbursed by their employer. The Family Glitch affects how families qualify for premium tax credits under the Affordable Care Act (ACA). Understanding how ICHRA interacts with this glitch is important for employees and their families.

Why Ichra Does Not Fix The Family Glitch

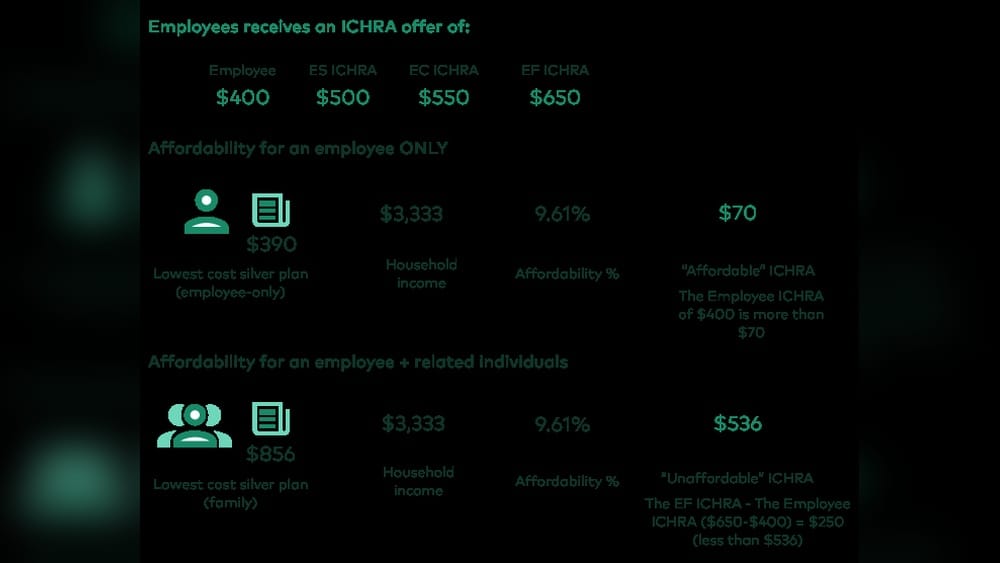

The Family Glitch happens when employer coverage is affordable only for the employee, not the whole family. The government looks at the cost of self-only coverage, not family coverage, to decide if tax credits apply. ICHRA bases affordability on the lowest-cost self-only plan offered to the employee. This means the Family Glitch still blocks families from getting premium tax credits, even with ICHRA.

Affordability Calculations With Ichra

Employers set a monthly allowance for employees through ICHRA. Employees use this allowance to buy individual health plans. Affordability is measured by the cost of the lowest-priced self-only plan minus the ICHRA allowance. If this net cost is below 9.12% of household income, coverage is affordable. But this calculation does not consider family coverage costs, keeping the Family Glitch in place.

Eligibility For Premium Tax Credits

Premium tax credits help lower insurance costs for eligible families. Eligibility depends on whether employer coverage is affordable for the family. Because ICHRA affordability is based on self-only coverage, family members may not qualify for credits. Even if family coverage is costly, they cannot get tax help if the employee’s self-only coverage is affordable. This limits tax credit access for many families with ICHRA offers.

Credit: w3ll.com

Savings Opportunities With Ichra

Individual Coverage Health Reimbursement Arrangements (ICHRA) offer unique savings opportunities. They help employees overcome the family glitch and save money on healthcare costs. ICHRA allows employers to contribute directly to employees’ health expenses. This system provides flexibility and control over health spending. Understanding how to maximize these savings is key.

Maximizing Employer Contributions

Employers set a monthly allowance for each employee class. Employees can use this money to buy individual health insurance or pay medical bills. Using the full employer contribution reduces out-of-pocket costs. Choosing plans that fit your needs helps stretch this allowance. It is important to compare options carefully and use the entire benefit.

Avoiding Premium Increases

ICHRA can protect employees from yearly premium hikes. Because employees buy insurance on the individual market, they can switch plans annually. This flexibility helps avoid sudden premium increases from employer plans. Employees can select more affordable coverage each year. This option prevents surprises and keeps healthcare affordable over time.

Handling Unused Ichra Funds

Unused ICHRA money may or may not roll over, depending on employer rules. Some employers allow funds to carry forward, increasing savings. Others require unused funds to be forfeited at year-end. Knowing your employer’s policy helps plan healthcare spending wisely. Planning expenses to use the full allowance avoids losing money.

Challenges And Downsides

Understanding the challenges and downsides of ICHRA is important. It helps employees and employers know what to expect. While ICHRA offers flexibility, some problems affect its effectiveness. These issues relate to coverage, costs, and plan options.

Here are the main challenges faced with ICHRA in the context of the family glitch.

Coverage Limitations By Employee Class

Employers set different ICHRA allowances by employee groups. Some classes get higher or lower benefits. This can cause unequal coverage among workers. Lower allowances may not cover needed health plans. Employees in smaller classes might face limited options. This setup can create confusion and dissatisfaction.

Out-of-pocket Costs And Medical Needs

Employees must pay expenses upfront and request reimbursement. High out-of-pocket costs can be a burden. Those with serious medical conditions may find the allowance too low. This forces them to spend more from their pockets. It reduces the financial protection that health coverage should provide. ICHRA does not always match individual health needs well.

Market Plan Availability Concerns

Not all health plans are available in every market. Some employees may struggle to find suitable plans. Limited choices can affect coverage quality and price. The family glitch remains because ICHRA allowances must be affordable only for self-only coverage. Family members may not qualify for subsidies outside the employer plan. This limits affordable options for entire families.

Credit: www.takecommandhealth.com

Policy Changes And Future Outlook

Policy changes around ICHRA and the family glitch affect many families and employers. Understanding these changes helps predict how health coverage options will evolve. The future outlook involves IRS rules, possible legislative fixes, and impacts on employer plans. These factors shape how affordable health insurance becomes for workers and their families.

Irs Considerations For Ichra Affordability

The IRS sets rules to determine if ICHRA coverage is affordable. These rules affect whether employees can get premium tax credits. The family glitch occurs when only employee coverage is affordable, but family coverage is not. The IRS currently bases affordability on self-only coverage costs. This limits families from accessing subsidies for their coverage.

Potential Fixes To The Family Glitch

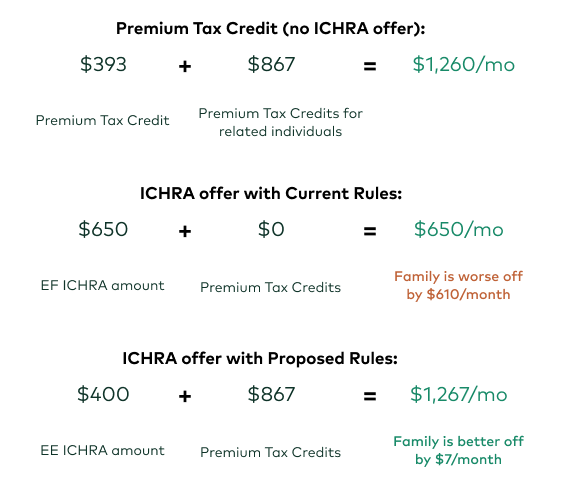

Lawmakers propose changes to fix the family glitch in health coverage. One idea is to base affordability on the cost of family coverage, not just self-only. This change would allow more families to qualify for financial help. Another proposal is to expand ICHRA rules to better address family needs. These fixes aim to reduce health insurance costs for many households.

Impact On Employer-sponsored Coverage

Employers may need to adjust their health plans due to policy changes. Changes in ICHRA rules could affect employer costs and employee choices. Some employers might increase contributions for family coverage. Others could offer different ICHRA options to meet new affordability standards. These shifts could improve access to affordable coverage for workers and their families.

Practical Tips For Families

Families affected by the family glitch face unique challenges with health coverage. Understanding how ICHRA works alongside this issue can help families make better choices. Practical tips can guide families through evaluating options, comparing plans, and understanding tax credit eligibility.

Evaluating Ichra Offers

Start by reviewing the employer’s ICHRA allowance carefully. Check how much money the employer provides for health expenses. Compare this amount with the cost of individual health plans. Consider the types of expenses ICHRA will cover. Think about your family’s health needs and budget. Make sure the ICHRA offer matches your expected health costs.

Comparing Marketplace Plans

Look at health plans available on the marketplace. Compare monthly premiums, deductibles, and out-of-pocket costs. Check if plans cover your preferred doctors and hospitals. Review benefits for family members and special health needs. Consider plans with lower costs but good coverage. This helps find the best value for your family.

Navigating Eligibility For Tax Credits

Understand how the family glitch affects tax credit eligibility. If employer coverage is affordable for the employee, family members may not get tax credits. Use online tools to check if your family qualifies for subsidies. Calculate your household income and compare it to the affordability thresholds. Knowing this helps plan your health coverage expenses better.

Frequently Asked Questions

What Are The Downsides Of Ichra?

ICHRA downsides include limited plan choices, varying employer allowances, potential higher out-of-pocket costs, and no resolution for the family glitch issue.

What Is The Family Glitch Rule?

The family glitch rule blocks families from getting ACA subsidies if an employee’s self-only coverage is affordable, even if family coverage is costly.

How Does Ichra Reimbursement Work?

Employers set a monthly allowance for employees. Employees buy health coverage, submit expenses, and get reimbursed up to the allowance.

What Happens To Unused Ichra Funds?

Unused ICHRA funds typically do not roll over and return to the employer at year-end. Employees lose unused amounts.

Conclusion

ICHRA offers a flexible way for employees to get health coverage. It lets families choose plans that fit their needs. The family glitch still limits some from getting tax help. ICHRA does not fully fix this issue yet. Employees should weigh their options carefully.

Understanding both ICHRA and the family glitch helps make better health choices. Employers and workers can both benefit by staying informed. Health coverage decisions become clearer with good knowledge.