Are you struggling to understand how the Individual Coverage Health Reimbursement Arrangement (ICHRA) fits into the confusing world of the family glitch? You’re not alone.

The family glitch has left many families stuck paying more for health insurance than they should, even when employer coverage seems “affordable. ” But ICHRA might just be the solution you didn’t know existed. You’ll discover how ICHRA works alongside—or around—the family glitch to give you more control over your healthcare costs.

Keep reading to find out how this benefit could unlock better coverage options and savings for you and your family.

Credit: www.takecommandhealth.com

Family Glitch Basics

The Family Glitch is a key issue in health coverage. It affects many families who want affordable insurance. Understanding its basics helps clarify how ICHRA fits in. This section breaks down the Family Glitch and its effects on employee health plans.

What The Family Glitch Means

The Family Glitch happens when employer coverage is affordable for the worker but not for their family. The Affordable Care Act sets rules on who can get subsidies for health plans. If the worker’s coverage is affordable, family members usually cannot get help. This leaves many families with high insurance costs.

Impact On Employee Coverage

Employees may get good health insurance offers from their job. But family members often face expensive options. This limits choices for families who need coverage. The glitch can cause some to skip insurance or pay large bills. It also affects how employers design their health benefits.

Current Limitations

The Family Glitch rule does not consider family income or size. It only looks at the worker’s coverage cost. This creates gaps for many families needing help. Changes to fix this glitch have been slow. Until then, families must navigate these limits carefully.

Ichra Fundamentals

Understanding the basics of ICHRA helps clarify its role in addressing the family glitch. ICHRA, or Individual Coverage Health Reimbursement Arrangement, allows employers to offer employees tax-free funds. Employees use these funds to buy their own health insurance plans. This flexible approach can work around some issues caused by the family glitch.

Let’s explore how ICHRA functions, how employers set allowances, and how employees get reimbursed.

How Ichra Functions

ICHRA lets employers give employees money for individual health plans. Employees choose plans that suit their needs and budgets. The employer controls the budget but not the plan choice. This setup avoids the problem of one-size-fits-all group plans. It also allows family members to get coverage that fits better.

Setting Allowances

Employers set monthly or yearly allowances for each employee. Allowances can differ by job type, age, or location. This flexibility helps employers tailor benefits to their workforce. Employees use these funds to pay insurance premiums or eligible medical expenses. Clear communication about allowances is key to avoid confusion.

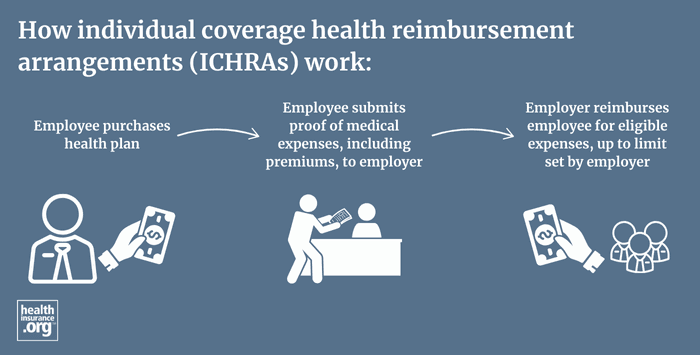

Employee Reimbursement Process

Employees buy individual insurance plans outside the employer’s group plan. Then they submit proof of coverage and expenses to the employer or plan administrator. The employer reimburses the employee up to the set allowance. This process is simple and keeps costs transparent. Employees get more control over their health benefits this way.

Ichra And The Family Glitch

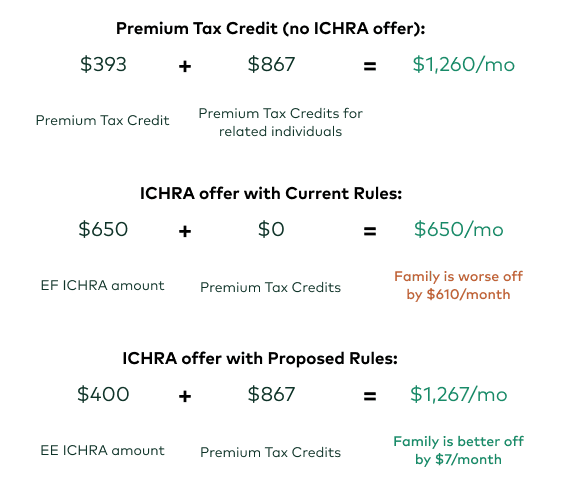

The Individual Coverage Health Reimbursement Arrangement (ICHRA) offers employers a flexible way to help employees buy health insurance. The “family glitch” affects many families trying to get affordable coverage through the health insurance marketplace. This glitch can limit access to subsidies for families who have access to employer coverage. Understanding how ICHRA interacts with the family glitch is important for families and employers alike.

Why Ichra Is Affected

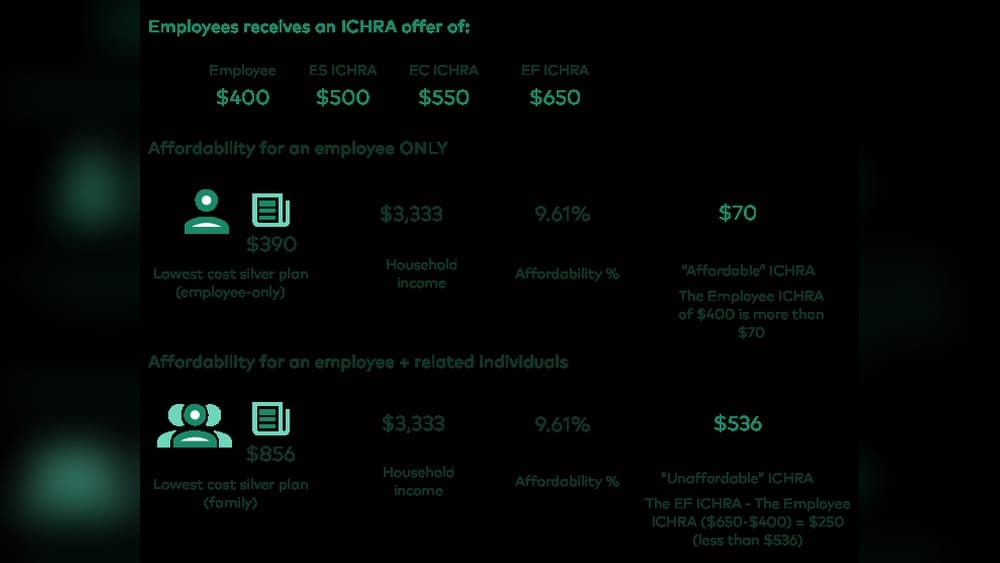

ICHRA is affected by the family glitch because it is considered an employer-sponsored plan. The Affordable Care Act (ACA) sets rules about affordability based on the employee’s cost for self-only coverage. If the employee’s share is affordable, the family cannot get subsidies for marketplace coverage. This rule ignores the cost of adding family members, which is often much higher.

Differences From Group Plans

Traditional group health plans calculate affordability differently. They look at the cost of covering the entire family. ICHRA bases affordability only on the employee’s individual coverage cost. This creates a gap where families might pay too much for coverage or lose access to marketplace help. The difference in calculation is key to understanding the family glitch with ICHRA.

Implications For Families

Families with ICHRA may face higher out-of-pocket costs. They might not qualify for premium tax credits even if family coverage is expensive. This can make health insurance less affordable for dependents. Families should carefully review their options and costs before choosing coverage through ICHRA or the marketplace.

Navigating Benefits With Ichra

Navigating benefits with an Individual Coverage Health Reimbursement Arrangement (ICHRA) offers a clear path around the family glitch. Employers provide a fixed amount of money to employees, which they can use to buy their own health insurance. This arrangement allows families to access health plans that fit their needs and budgets. Understanding how to choose plans, handle tax credits, and manage options is key.

Choosing Individual Coverage

Employees use ICHRA funds to select individual health insurance plans. These plans can be tailored to their specific health needs. Unlike traditional group plans, individuals can pick coverage that suits their family size and preferences. This freedom helps families avoid being stuck with unaffordable employer plans.

Handling Marketplace Tax Credits

ICHRA affects eligibility for marketplace tax credits. If the ICHRA offer is affordable for individual coverage, employees cannot claim these credits. Affordability is based on the employee’s share of premium costs for self-only coverage. Families may still qualify for credits if the employer’s offer is not affordable for their family size.

Managing Plan Options

Plan options vary by location and insurer availability. Employees should review available individual plans carefully. Some areas have limited choices, so understanding plan details is crucial. Managing these options allows employees to maximize the value of their ICHRA funds and get the best coverage for their family.

Employer Considerations

Employers face key considerations when offering an ICHRA amid the family glitch. Understanding how to manage these challenges helps maintain smooth benefits administration. Careful planning ensures compliance and keeps costs under control. Clear communication supports employee understanding and satisfaction. These factors work together to make ICHRA a viable option for employers.

Administration And Compliance Challenges

Managing ICHRA plans can be complex. Employers must track employee eligibility accurately. They need to verify that employees use funds for qualified coverage. Staying updated on federal rules is essential. Documentation and reporting require attention to avoid penalties. Ensuring compliance with the Affordable Care Act rules is critical. Employers may need software or expert help to handle these tasks efficiently.

Budgeting For Ichra Allowances

Setting the right ICHRA allowance is crucial. Employers should balance affordability with competitiveness. Allowances must cover expected employee health insurance costs. Budget planning should consider employee family sizes due to the family glitch. Employers might adjust budgets yearly based on plan costs and employee feedback. Clear budgets prevent overspending and help maintain financial health.

Communicating Benefits Effectively

Employees often find health benefits confusing. Employers should explain how ICHRA works simply. Highlight how ICHRA interacts with the family glitch rule. Use clear examples to show potential savings or costs. Provide regular updates during open enrollment periods. Use multiple channels like email, meetings, and printed guides. Good communication increases employee satisfaction and benefit utilization.

Credit: www.healthinsurance.org

Potential Downsides

Understanding the potential downsides of how ICHRA works with the family glitch helps set realistic expectations. ICHRA offers benefits but also brings some challenges. These issues may affect employees and employers differently. Knowing these limits can guide better decisions about health coverage options.

Limited Plan Choices In Some Areas

Not all regions have many individual health plans to choose from. ICHRA relies on the individual market for coverage. In some places, options are few and may not fit every need. This limits flexibility for employees trying to find the best plan. It can make ICHRA less attractive if good plans are scarce.

Loss Of Marketplace Subsidies

Employees using ICHRA might lose access to marketplace subsidies. If their employer offers affordable coverage, they cannot get tax credits. This means higher out-of-pocket costs for some families. The family glitch often causes this loss of financial help. Employees must weigh this loss against the benefits of ICHRA reimbursements.

Complexities In Managing Reimbursements

Handling ICHRA reimbursements can be complicated for both employers and employees. Tracking eligible expenses and submitting claims requires careful attention. Mistakes may lead to denied reimbursements or tax issues. Managing this process adds extra work and stress. Clear communication and good record-keeping are essential to avoid problems.

Strategies To Unlock Benefits

Strategies to unlock benefits with ICHRA and the family glitch focus on smart planning. Understanding the rules helps families get the most from their healthcare spending. Small changes can create big savings and better coverage choices.

Employers and employees should work together to explore flexible options and stay informed. This approach reduces gaps caused by the family glitch and improves overall health benefit value.

Maximizing Ichra Flexibility

ICHRA allows employers to set different budgets for employees. Families can use this to tailor coverage that fits their needs. Choosing plans that match individual health situations saves money. Flexible spending on premiums and out-of-pocket costs gives more control.

Employees may combine ICHRA funds with other benefits. This mix can fill coverage gaps created by the family glitch. Flexibility in plan selection also helps families avoid losing tax credits.

Supplementing Coverage Options

Adding supplemental insurance can protect against unexpected costs. Dental, vision, or critical illness plans often complement ICHRA coverage. These extras reduce financial risk and increase peace of mind.

Some families use marketplace plans alongside ICHRA to balance costs. Careful comparison of benefits and prices reveals the best mix. Supplementing coverage helps bridge gaps left by employer offers under the family glitch.

Staying Updated On Policy Changes

Health laws and rules change regularly. Keeping up with updates ensures families do not miss new opportunities. Changes in affordability tests or tax credit rules affect ICHRA use.

Employers should communicate new details clearly and promptly. Employees benefit from checking trusted sources each year. Staying informed prevents surprises and improves benefit decisions.

Credit: w3ll.com

Frequently Asked Questions

What Are The Downsides Of Ichra?

ICHRA downsides include limited plan options in some areas, potential loss of Marketplace tax credits for employees, and complex administration requirements.

What Is The Family Glitch Rule?

The family glitch rule denies financial help for family coverage if employer insurance is affordable for the employee, regardless of family cost.

How Does Ichra Reimbursement Work?

Employers set a reimbursement allowance for each employee class. Employees buy health coverage, submit proof, and get reimbursed up to their allowance.

What Happens To Unused Ichra Funds?

Unused ICHRA funds typically do not roll over and return to the employer at the plan year’s end.

Conclusion

ICHRA helps families affected by the family glitch find better options. Employers set a budget for each employee class. Employees choose and buy their own insurance plans. They submit proof to get reimbursed. This approach offers more flexibility than traditional group plans.

It can reduce coverage gaps caused by the family glitch. Still, employees should check local plan choices carefully. Understanding how ICHRA works makes health benefits clearer. It gives families more control over their healthcare spending.