If you’re a small business owner, finding the right way to offer health benefits without the hassle of group insurance can feel overwhelming. That’s where QSEHRA comes in—a smart, flexible solution designed just for employers like you.

Imagine giving your employees personalized health reimbursements while keeping your costs predictable and manageable. Curious how QSEHRA can transform your benefits plan, save you money, and simplify compliance? Keep reading, because understanding this powerful tool could be the game-changer your business needs.

Credit: ritterim.com

Qsehra Basics

Understanding QSEHRA basics helps small business owners offer health benefits. This guide breaks down key points about Qualified Small Employer Health Reimbursement Arrangements.

QSEHRA lets employers reimburse employees for medical expenses and insurance premiums. It is a simple way to provide tax-free health benefits without group health plans.

What Is Qsehra

QSEHRA stands for Qualified Small Employer Health Reimbursement Arrangement. It allows small employers to pay employees back for health costs. Employers set a monthly allowance for medical expenses or insurance premiums. Employees use this money to cover eligible health-related costs. This plan does not require a group health insurance policy.

Eligibility Requirements

Employers must have fewer than 50 full-time employees to offer QSEHRA. They cannot provide any group health insurance coverage to employees. All full-time employees must be offered the same health reimbursement amount. Employees with other health coverage, like Medicare, can still use QSEHRA. Employees must submit receipts or proof of medical spending to get reimbursed.

Annual Contribution Limits

The IRS sets yearly maximum amounts employers can reimburse through QSEHRA. For 2024, the limits are $5,850 for individuals and $11,800 for families. Employers cannot exceed these limits but may choose lower amounts. Contributions are tax-free for both employers and employees. Limits may change each year, so employers should check current IRS rules.

Credit: www.takecommandhealth.com

Qsehra Vs Other Hras

Understanding the differences between QSEHRA and other HRAs helps employers choose the right option. QSEHRA is designed for small businesses without group health plans. Other HRAs like ICHRA and Group Coverage HRA work differently. Each has unique rules about contributions, coverage, and tax effects. This section explains these differences clearly.

Differences From Ichra

QSEHRA applies only to small employers with fewer than 50 employees. ICHRA can be used by any size employer. QSEHRA has yearly contribution limits set by the IRS. ICHRA has no fixed limits on employer contributions. Employees with ICHRA can choose to use tax credits or the HRA benefit. QSEHRA reduces tax credits for employees. The plans differ in flexibility and size of the business they serve.

Comparison With Group Coverage Hra

Group Coverage HRA works only with employer-sponsored group health plans. QSEHRA works without a group health plan. Employers using Group Coverage HRA reimburse employees for out-of-pocket costs from their group plan. QSEHRA reimburses for individual health insurance and medical expenses. Group Coverage HRA suits larger companies with group plans. QSEHRA targets small businesses avoiding group plans.

Impact On Tax Credits

QSEHRA reduces Marketplace premium tax credits employees can get. This means employees may receive smaller tax credits if reimbursed through QSEHRA. ICHRA gives employees a choice to use tax credits or HRA funds, but not both. Group Coverage HRA does not affect Marketplace tax credits because it requires a group plan. Employers and employees must understand these effects for cost planning.

Benefits For Small Businesses

Small businesses face unique challenges in offering health benefits. QSEHRA provides solutions tailored for these needs. It helps small employers support their employees without the complexity of group plans.

Here are key benefits small businesses gain from using QSEHRA.

Flexibility In Health Benefits

QSEHRA lets employers set personalized reimbursement amounts. Employees choose health plans that fit their needs. This flexibility suits various family sizes and health situations. Employers avoid one-size-fits-all group plans. It makes managing benefits simpler and more employee-focused.

Cost Management Advantages

Employers control exactly how much to spend on health benefits. QSEHRA limits help avoid unexpected costs. Small businesses can budget better and reduce financial risk. No need to pay for full group coverage. This system keeps health spending predictable and fair.

Attracting And Retaining Employees

Offering QSEHRA shows care for employee health needs. It improves job satisfaction and loyalty. Health benefits attract qualified candidates to small businesses. Employees value the freedom to select their own plans. This advantage helps reduce turnover and build a stable team.

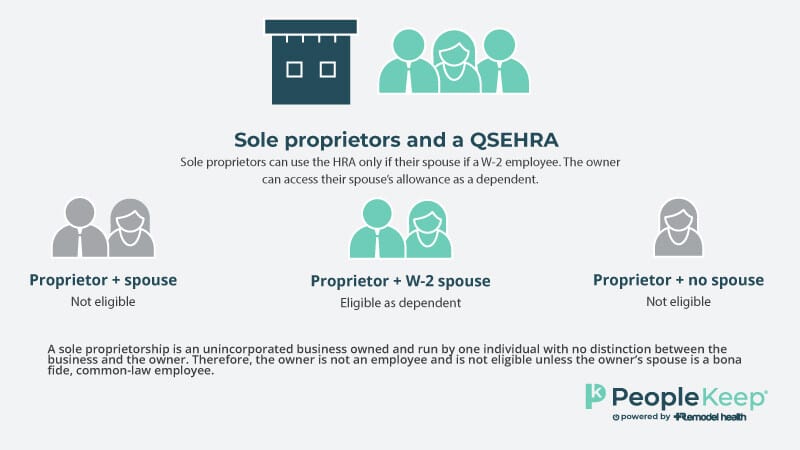

Credit: www.peoplekeep.com

Qsehra Compliance

QSEHRA compliance is essential for small employers offering health benefits. It ensures the plan meets IRS rules and protects both employers and employees. Following compliance steps helps avoid penalties and misunderstandings. Understanding key areas like reporting, coverage rules, and common errors is important.

Irs Reporting Requirements

Employers must report QSEHRA payments on employees’ W-2 forms. The amount reimbursed appears in Box 12 with code “FF”. Reporting shows transparency and follows IRS rules. Employees use this information when filing taxes. Missing or incorrect reporting can cause penalties or audits.

Affordable Coverage Considerations

QSEHRA amounts must stay within IRS limits each year. Employers should check annual contribution caps before setting reimbursements. The coverage must be affordable for employees to keep tax advantages. Affordable means employees can buy individual health plans without losing subsidies. Employers must update amounts yearly to remain compliant.

Avoiding Common Mistakes

Common errors include mixing QSEHRA with group health plans. Employers cannot offer group coverage alongside QSEHRA. Another mistake is failing to verify employee eligibility properly. Keep records of reimbursements and employee notices. Not informing employees about QSEHRA details leads to confusion. Regularly review plan rules to prevent compliance issues.

Reimbursable Expenses

Reimbursable expenses under a QSEHRA allow employees to get money back for certain health costs. Employers set a budget that employees use to pay for eligible medical expenses. Understanding which expenses qualify helps both employers and employees make the most of their QSEHRA benefits.

Eligible Medical Costs

QSEHRA covers many medical expenses approved by the IRS. These include doctor visits, prescriptions, dental care, and vision care. Expenses like copayments, deductibles, and some over-the-counter medicines are also eligible. Keeping receipts is important for reimbursement claims.

Medicare Premiums And Qsehra

Medicare premiums qualify for reimbursement under QSEHRA. This includes Part B and Part D premiums. Employees on Medicare can use QSEHRA funds to pay these costs. This helps reduce out-of-pocket expenses for retirees and those on government health plans.

Non-reimbursable Items

Not all health-related expenses can be reimbursed through QSEHRA. Cosmetic procedures, gym memberships, and vitamins usually do not qualify. Expenses that are not IRS-approved medical costs cannot be reimbursed. Employees should check the list of eligible expenses before submitting claims.

Setting Up Qsehra

Setting up a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) requires careful planning. Employers must understand key steps to ensure smooth implementation. This process helps small businesses offer health benefits without a group health plan.

Determining Allowance Amounts

Start by deciding how much to allocate for each employee. The IRS sets annual limits on QSEHRA contributions. Employers can vary amounts based on family size and age. Setting clear, fair allowance amounts helps manage costs and employee expectations.

Communication With Employees

Inform employees about QSEHRA rules and benefits clearly. Explain how reimbursements work and what expenses qualify. Provide written notices to meet legal requirements. Open communication avoids confusion and builds trust among staff.

Integration With Payroll

Coordinate QSEHRA reimbursements with your payroll system. Track employee claims and payments accurately. Ensure proper tax reporting to avoid penalties. Using payroll software or a third-party service simplifies this process.

Employee Experience

QSEHRA offers employees a simple way to manage health expenses. It allows them to receive reimbursements for medical costs. This benefit helps employees choose their own health plans. They get more control and flexibility over their healthcare.

Employees enjoy less hassle with claims and paperwork. They can use funds for various qualified expenses. This makes healthcare more affordable and less stressful. The clear structure of QSEHRA improves satisfaction and trust in the workplace.

Using Qsehra Funds

Employees use QSEHRA funds to pay for medical costs. This includes doctor visits, prescriptions, and dental care. They submit receipts to their employer for reimbursement. The process is straightforward and fast. Employees only pay for what they need.

QSEHRA funds cannot be used for non-qualified expenses. Employees must keep track of their spending. This control helps avoid overspending and confusion. It also encourages smart healthcare choices.

Tax Benefits For Employees

Money received through QSEHRA is tax-free. Employees do not pay federal income tax on these reimbursements. This increases their take-home pay. It also lowers the overall cost of healthcare for them.

Tax savings from QSEHRA make health expenses easier to handle. Employees can afford better coverage or treatments. The tax benefit is a key advantage of using QSEHRA funds.

Handling Marketplace Premium Tax Credits

QSEHRA affects eligibility for Marketplace premium tax credits. Employees must report QSEHRA reimbursements when applying for credits. These reimbursements may reduce the amount of tax credits. This could increase the employee’s health insurance cost.

It is important for employees to understand these rules. Proper reporting ensures they get the right amount of tax credits. Employees can avoid surprises during tax season by staying informed.

Qsehra Challenges

QSEHRA offers small employers a way to provide health benefits. It has many advantages but also presents challenges. Understanding these difficulties helps employers manage their plans better. The following sections explain common QSEHRA challenges.

Limitations And Restrictions

QSEHRA has strict rules about who can participate. Employers cannot offer group health plans alongside QSEHRA. The IRS sets yearly limits on how much employers can contribute. These limits can restrict how much help employees receive. Only certain medical expenses qualify for reimbursement. This limits flexibility for both employers and employees.

Managing Multiple Health Plans

Handling different health plans can be confusing. Employers must track who uses QSEHRA and who does not. Employees may have other coverage, affecting their QSEHRA benefits. Keeping records accurate is essential to avoid tax problems. Communication with employees about their benefits is very important. Mistakes in managing plans can cause compliance issues.

Navigating Regulatory Changes

Health care laws and rules change often. Employers must stay updated on QSEHRA regulations. New rules can affect contribution limits and eligibility. Missing changes can lead to penalties or lost benefits. Regularly reviewing policies and consulting experts helps. Adapting quickly keeps the plan compliant and effective.

Frequently Asked Questions

What Is The Annual Qsehra Limit?

The 2024 annual QSEHRA limit is $5,850 for individuals and $11,800 for families, set by the IRS. Employers must follow these limits.

What Is The Difference Between An Hra And A Qsehra?

An HRA is a broad employer-funded health benefit. A QSEHRA is a specific HRA for small employers without group plans, with set contribution limits.

When Can Funds From A Qsehra Be Used?

Funds from a QSEHRA can be used to reimburse employees for qualified medical expenses. Employers set the reimbursement limits annually. Employees must have individual health insurance coverage to use QSEHRA funds. Reimbursements cover premiums, deductibles, copays, and other IRS-approved medical costs.

Can Qsehra Reimburse Medicare Premiums?

QSEHRA can reimburse Medicare premiums only if the employee has individual health coverage. It cannot reimburse Medicare Advantage or supplement premiums. Employers must follow IRS rules and limits for eligible expenses.

Conclusion

QSEHRA offers small employers a simple health benefit option. It helps cover employee medical costs without group plans. Employers set limits based on IRS rules. Employees get reimbursed tax-free for eligible expenses. This plan fits businesses wanting flexible, affordable health coverage.

Understanding QSEHRA rules ensures compliance and smooth use. It stands as a clear choice for many small companies. Consider your business needs to see if QSEHRA suits you well.